20 REIT CEO Meetings: My Top Picks

Please note that this is a free article of High Yield Landlord. If you find it valuable, consider joining our service for a 2-week free trial. You'll gain immediate access to my entire REIT portfolio, real-time trade alerts, exclusive REIT CEO interviews, and much more.

20 REIT CEO Meetings: My Top Picks

Earlier this year, I attended the Citi Global Property Conference and I got to talk to a lot of REIT management teams and participated in the roundtables of the following REITs:

Tricon Residential (TCN)

American Homes 4 Rent (AMH)

Federal Realty Trust (FRT)

AvalonBay (AVB)

Independence Realty Trust (IRT)

Mid-America Communities (MAA)

Camden Property Trust (CPT)

Boardwalk REIT (BEI.UN)

Alexandria Real Estate (ARE)

Gaming and Leisure Properties (GLPI)

VICI Properties (VICI)

EastGroup Properties (EGP)

Segro (SGRO):

STAG Industrial (STAG)

Germany: Grand City Properties & AroundTown - Relevant to Vonovia (VNA) & DIC Asset (DIC)

National Storage REIT (NSR)

Hotel REITs: Apple Hospitality REIT (APLE), Hersha Hospitality (HT), Chatham Lodging (CLDT)

National Retail Properties (NNN)

Essential Properties Realty Trust (EPRT)

Spirit Realty Capital (SRC)

Realty Income (O)

W.P Carey (WPC)

Today, we want to highlight three REITs from this list that have become even better investment opportunities as a result of our new findings.

This new information is now public, but it appears to have gotten overlooked by most analysts who weren't present in person to talk with management teams and observe their body language.

We would have expected the share prices of these REITs to rise by now, but they didn't, despite revealing very positive news that should help their stock going forward.

We gained a bit more insight into topics through 1-to-1 conversations with the management and perhaps that is why the rest of the market is still missing the point.

This provides us a unique opportunity to accumulate more shares at discounted prices thanks to our access to the conference and management teams.

STAG Industrial (STAG) Has a Major Near-Term Catalyst: Large Dividend Hikes

Following STAG's roundtable presentation, I went straight to the CFO because I was interested to learn more about their thoughts on their current dividend.

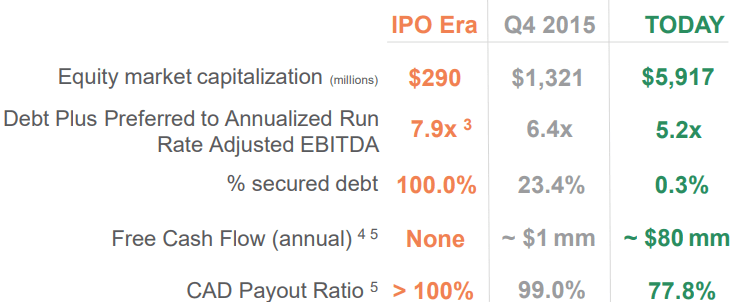

For context, STAG is an industrial REIT that has performed really well over the past years, but it has failed to grow its dividend by much because it focused on deleveraging its balance sheet, lowering its payout ratio, and increasing the quality of its portfolio.

We think that the lack of dividend growth has negatively affected its valuation. We commonly hear from investors here on Seeking Alpha that they are not investing in STAG because its dividend is growing a lot slower than its peers.

It then isn't surprising that its valuation is a lot lower than that of its peers:

STAG Industrial High-Quality Industrial REITs FFO Multiple 16x 24x

But we have been predicting that this valuation gap would close down as STAG eventually instates a new dividend growth policy. STAG is otherwise a high-quality REIT with a monthly dividend, rapid growth prospects, a strong balance sheet, and a track record of outperformance.

Well... here's the big news:

It appears that STAG will announce a big dividend hike in the near-term.

The CFO tells me that their transformation is now complete and they have the strong balance sheet and low payout ratio that they were targeting:

Therefore, their CFO told me that their dividend would rise at approximately the same rate as their cash flow going forward.

I think that as they announce a large dividend hike, this will be celebrated by the investor community and it will push the share price and valuation higher.

Today, the company is enjoying rapid organic growth as its rents are deeply below market and they are being adjusted higher as leases expire:

This should provide years of solid dividend growth and a clear path to a re-rating of the stock.

Assuming that STAG's valuation rises to 20x FFO, which is still below average for a high-quality industrial REIT, its share price would need to rise by nearly 30%. That may not sound like much when compared to some other REITs, but the interesting thing here is that the catalyst is very clear.

Besides, STAG is priced to deliver roughly double-digit total returns from its yield and growth alone, so even if the repricing fails to occur, the long-term returns should be attractive here. Its growth is also mostly organic so the thesis does not rely on the capital markets.

The dividend yield is today 4.1% and it could soon get closer to 5%. Now is still a good time to accumulate shares before the market recognizes the coming dividend growth story.

You can read our full investment thesis by clicking here.

Tricon Residential (TCN) Also Has a Major Catalyst: The Return To AUM Growth

TCN is unique in that it is not just a landlord. It is also an asset manager that earns fees for managing capital for other investors.

This used to warrant a generous valuation with the shares trading at a healthy premium to their net asset value. This was justified because it was growing at a rapid and still recently, it was targeting 15% annual FFO per share growth over the next years.

To achieve this rapid growth, it was planning to buy a large number of homes with the capital of other investors, growing its fee income in the process:

But then interest rates surged and the volume of transactions dropped significantly. This forced TCN to dial back its growth guidance because it would have been imprudent to buy so many homes in today's market.

This caused its premium valuation to quickly turn into a deeply discounted valuation. The CEO noted that they have never traded at such a low valuation with their shares trading at a 45% discount to NAV.

But here's the big news:

The CEO said that their capital partners now WANT TO return to growth. They want TCN to return to acquisitions to deploy their capital. They are happy with the unleveraged returns of single-family homes and can add debt to them later anyway. They understand the long-term opportunity in single-family rentals, they are underallocated to them, and they want the inflation-protected income that they generate.

The CEO hinted strongly that they will return to growth in the near-term with the launch of a new fund later this year and he said explicitly that he thinks that this should be a "big catalyst" for their stock.

Their capital partners are ready to go and want to invest more whenever TCN is ready to restart acquisitions and it seems like just a question of time at this point.

If TCN returned to a slight premium to its NAV, its share price could double. More realistically, TCN will likely continue to trade at a slight discount until all the uncertainty disappears, but even returning to a 20% discount to its NAV, would lead to nearly 50% upside from here.

The catalyst is the return to faster growth and this appears to be happening soon. On a side note, the CEO was very charismatic and seemed to be genuinely bullish about their growth outlook.

Alexandria Real Estate (ARE) Is Doing Better Than Ever & Has No Difficulties Accessing Capital

ARE's share price has been cut in half over the past year.

This would imply that its growth outlook and/or the value of its assets has changed materially.

But this isn't the case. The management again reiterated that even their smaller biotech tenants that rely on VC funding are doing well. They had a record raise last year and they typically put this capital to work over many years. Therefore, the recent concerns over the health of its tenants are overblown and the strong rent growth should continue, especially since its rents are today deeply below market. For context, its recent rent growth has actually accelerated and it is among the fastest in the company's history:

So the organic growth of the company should remain strong in the years ahead. Its leases are commonly 40% below market and rent growth remains strong because there is a limited amount of high-quality life science space and lots of demand for it.

But that's not the real news.

The real news is regarding the external growth of the company.

I suspect that the share price dropped a lot more than it should have because the market got worried that the company's external growth would stop as the company couldn't raise more equity at these prices.

However, the CEO noted clearly at the conference that they don't need to access equity in the public market to grow.

He explains that they have a lot of JV partners who are interested in buying equity interest in their properties and cap rates remain stubbornly low for life science buildings because there is so little supply of high-quality properties and the growth remains so compelling. Moreover, some of its tenants have approached ARE to buy the properties that they occupy because they are so mission-critical to them and want to be fully in control. In such cases, it is ARE that dictates the pricing. They have already signed some LOIs this year so this should allow them to raise equity in the private market to keep growing externally as they reinvest this cash into higher-yielding development projects.

We expect 50% upside in the coming years as the company's share price recovers to our fair value estimate.

You can read our full investment thesis by clicking here.

Bottom Line

We expect to accumulate more shares of STAG, TCN, and ARE as new capital becomes available.

We are glad that industry conferences are now back and we expect to attend many more of them in the coming quarters to share exclusive insights with our members.

Finally, please note that this is a free article from High Yield Landlord. If you found it valuable, consider joining our service for a 2-week free trial. You'll gain immediate access to my entire REIT portfolio, real-time trade alerts, exclusive REIT CEO interviews, and much more. We are the largest and highest-rated REIT investment newsletter online, with over 2,000 paid members and more than 500 five-star reviews.

We spend 1000s of hours and over $100,000 per year researching the market for the most profitable investment opportunities and share the results with you at a tiny fraction of the cost.

Get started today - the first 2 weeks are on us:

Sincerely,

Jussi Askola

Analyst's Disclosure: I/we have a beneficial long position in the shares of all companies held in the CORE PORTFOLIO, RETIREMENT PORTFOLIO, and INTERNATIONAL PORTFOLIO either through stock ownership, options, or other derivatives. High Yield Landlord® ('HYL') is managed by Leonberg Research, a subsidiary of Leonberg Capital. All rights are reserved. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The newsletter is impersonal and subscribers/readers should not make any investment decision without conducting their own due diligence, and consulting their financial advisor about their specific situation. The information is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The opinions expressed are those of the publisher and are subject to change without notice. We are a team of five analysts, each contributing distinct perspectives. Nonetheless, Jussi Askola, the leader of the service, is responsible for making the final investment decisions and overseeing the portfolio. We do not always agree with each other and an investment by Jussi should not be taken as an endorsement by other authors. Past performance is no guarantee of future results. Our portfolio performance data is provided by Interactive Brokers and believed to be accurate but its accuracy has not been audited and cannot be guaranteed. Our portfolio may not be perfectly comparable to the relevant index. It is more concentrated and may at times use margin and/or invest in companies that are not typically included in REIT indexes. Finally, High Yield Landlord is not a licensed securities dealer, broker, US investment adviser, or investment bank. We simply share research on the REIT sector.