Interview With BSR REIT (Strong Buy Reaffirmed)

Important Note

Before going into today’s article, I wanted to let you know that we will soon conduct interviews with the management teams of the following REITs:

Agree Realty Corporation (ADC)

VICI Properties (VICI)

Gaming and Leisure Properties (GLPI)

NewLake Capital Partners (OTCQX:NLCP)

Gladstone Land (LAND)

Canadian Net REIT (NET.UN:CA)

Let me know if you have any questions for them, and I will make sure to ask them for you. You can put your questions in the comment section below.

Thanks!

=============================

Interview With BSR REIT (Strong Buy Reaffirmed)

BSR REIT (OTCPK:BSRTF / HOM.U:CA) is today our largest apartment REIT investment, representing 8% of our Core Portfolio. We invest so heavily in it because:

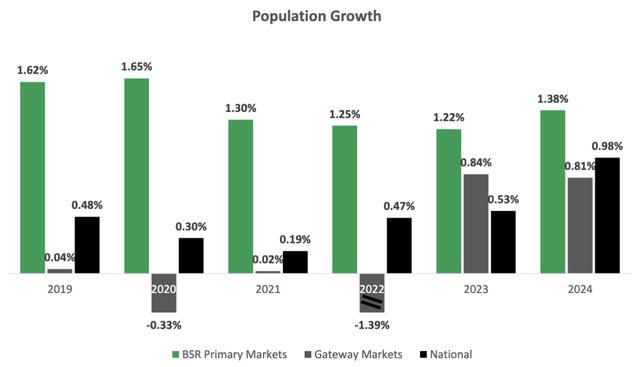

It owns affordable garden-style apartment communities in the famous Texan Triangle - Dallas, Austin, and Houston - which enjoys some of the fastest job and population growth in the nation. Over the long term, this unique focus has enabled BSR to grow its FFO and NAV per share at the fastest pace among its peer group.

Its average rent is around $1,500 per month, representing just about 20% of its residents’ income. This is nearly 2x lower than the average in gateway markets. It provides attractive long-term growth prospects and margin of safety in case of a recession.

The company has a good balance sheet with a 38% loan-to-value ratio, which we consider optimal for these assets to maximize long-term returns without compromising the company’s long-term solvency.

The management is very well aligned with shareholders, owning about 40% of the equity. They have funded significant share buybacks in recent years, and insiders have also made large personal purchases.

The shares are priced at a 30% discount to their net asset value, which is one of the lowest valuations in the apartment REIT sector. They have also recently sold a large portion of their assets, which has validated their net asset value. We believe that its stock is heavily discounted because most Texas markets are currently oversupplied, resulting in stagnant rents. But new construction activity has now dropped to a 10-year low, which should result in a strong acceleration in rent growth already in 2026. This could serve as a strong catalyst for the stock, and while we wait, we earn a 4.8% tax-advantaged dividend yield (classified as return of capital).

")

Recently, our analyst, Samuel Smith, who leads our sister service High Yield Investor, recently had the chance to talk with BSR REIT’s new CFO, Thomas Cirbus.

In the following interview, we discuss their growth outlook and how they plan to continue unlocking value for shareholders.

In short, the interview reaffirmed our investment thesis, which is that BSR REIT is likely to enjoy significant upside as rent growth accelerates in the near term.

Therefore, we maintain our Strong Buy rating on BSR. We already own a sizable position, but we will not hesitate to buy more if and when the stock dips in the future.

You can read our full investment thesis by clicking here.

Here is our interview: