Interview With Jeffrey Witherell, CEO Of Plymouth Industrial (Updated Rating And A Better Alternative)

Interview with Jeffrey Witherell, CEO of Plymouth Industrial

On January 14, we highlighted Plymouth Industrial REIT (PLYM) as the “Best Speculative Pick for 2019” and shared an exclusive interview with the CEO.

PLYM is a micro-cap industrial REIT that yielded over 10% back then and had enormous near-term growth potential. Later in July, we sold our position because the risk-to-reward had materially deteriorated:

We locked a nice gain and concluded that there wasn’t much meat on the bone left. Ever since, we have continued to follow the story from the sidelines because we remain interested in getting back on board sometime in the future.

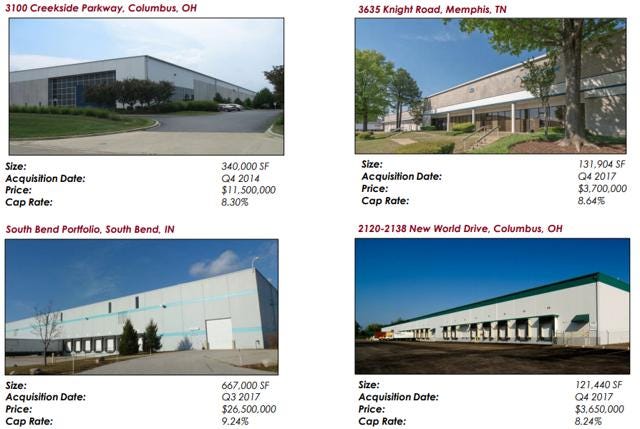

PLYM follows a unique approach that we believe to be set for long term outperformance (bearing they can handle their high leverage and meet guidance). Rather than target richly priced Class A assets at 4-5.5% cap rates – PLYM targets smaller Class B and C properties in secondary markets. These assets are riskier, but they also come with near double-digit cap rates and releasing spreads have been fairly comparable to Class A peers. Here are a few examples of the type of properties that they like to target:

We know that many of our members have kept holding on to their PLYM position. Therefore, we reached out to the CEO, Jeffrey Witherell, to have another talk about their future prospects. Below, we share the transcribed phone conversation and present our main take-aways:

JA: Jussi Askola

JW: Jeffrey Witherell

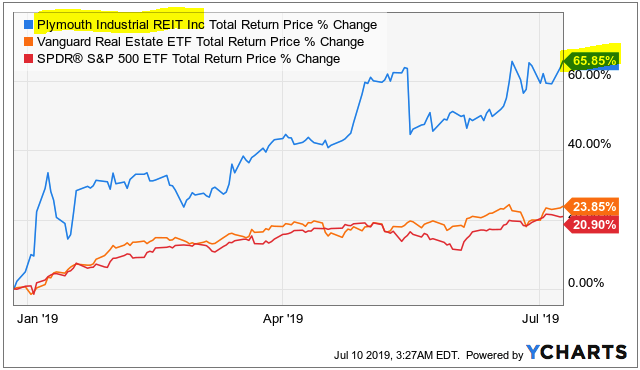

JA: Since our last interview in late December 2018, your share price has appreciated by roughly 50%. Do you think that your current share price remains undervalued given all the progress that you have made since then?

JW: I think that it is still discounted. Not deeply discounted, but we think that our NAV is closer to $21 per share.

(Note: current share price is at $18.75)

JA: Follow up: would you rather then buy back or issue shares right now?

JW: No, we won’t buy back shares. Issuing equity at this price is still accretive. We just issued a lot of it in May. I cannot talk about future offering but note that it is still accretive.

When you are a small cap like us as long as it is accretive, you keep issuing equity to reach scale. You need to get to over $300 million market cap to allow large institutions to invest in your company.

JA: Second Follow up: Would you rather issue common shares or go to alternative routes (Madison)

JW: Yes, that was a special situation with the right partner at the right time. It validated our investment thesis and we think that a lot of institutions saw that transactions and allowed us to gain their interest for our stock.

JA: With interest rates dropping significantly since December, how do you expect that to affect your balance sheet?

JW: Rates are very low and many people would now think that it is time to lever up, but we are in this for the long haul. We have long term vision so we want to deleverage slowly over time but at the same time we want to take advantage of the low rates on the debt that we do have.

JA: With increased investor appetite for Class B industrial properties, do you expect cap rate compression in the coming years?

JW: We don’t see a lot of it. It is deal specific. A lot of larger portfolios have traded at lower cap rates, but it is a bit all over the place.

Some investors are willing to overpay because they have access to very cheap capital and can make it work, but we have not seen anything drastic yet.

JA: How would you compare your approach of also buying multi-tenant industrial properties relative to only focusing on single tenant properties like STAG does?

JW: Our portfolio is roughly balanced between single tenant and multi tenant.

Multi tenant takes away that binary risk of the property going dark. You have income or don’t have income in single tenant. We like multi tenant because of that.

Let’s say you have a 100,000 square foot property and it is set up for single tenant. Now you are very limited for what you can find for replacement tenant. And in order to redevelop it for multi tenant, it is going to cost you significant capital to do that.

So if we have a property that is already set up for multi tenant, we may even be able to lease it to one tenant, but have lower risk. You don’t have the cost of having to redevelop it later on. You have more flexibility with the physical characteristics of the property.

I would say that it is less risky, but the other part of that is credit quality. Many REITs who buy single tenant 10 year leases – they are really underwriting the credit quality. When you play the net single single tenant, you are almost playing for renewals. You bet that your particular tenant will renew – whereas in multi tenant, often you may even wish that your tenant does not renew so that you can move the rent up significantly.

So we like all the physical characteristics of multi-tenant and the benefits that it affords.

JA: Finally, what impact do you expect to FFO per share if and when Madison decides to convert its preferred equity to common equity in January of 2022?

JW: We feel great about it. We want them to convert to common equity and they want to convert to common. It won’t result in much dilution and will improve the balance sheet.

The Main Take-Aways for Members of High Yield Landlord

The share price is currently at $18.75 – representing a ~15% discount to their estimate of NAV. Yet, they explain that they have no interest in buying back shares and would rather issue more of them – which they have done very aggressively. We think that this is a highly risky approach, which may work out well if they can find the right properties at high cap rates… but if they don’t, this expected accretion may quickly turn into dilution. We would prefer to see them take a more conservative approach.

Until now, the plan was always to deleverage because we are possibly approaching the end of the bull cycle and they are the most heavily leveraged industrial REIT – which puts them at high risk of losses when the cycle finally turns. Based on the most recent comments of the CEO, we believe that we won’t see much deleveraging for quite some time. They want to achieve scale as fast as possible and take advantage of the dropping rates. Again, this may work out well, but it is also very risky.

The management feels confident that they can keep buying at similar cap rates. We think that they genuinely believe so and are not just trying to sell us the bull story. PLYM is special in that it targets multi-tenant properties, which often come with higher cap rates due to the increased management intensity. They expect to keep targeting similar assets and won’t refocus exclusively on single tenant (as many of its peers have done). We see this as a positive. Single tenant properties take less efforts to manage but their cap rates have also compressed considerably as yield-starved investors replaced bonds with single tenant net lease properties with long leases.

The CEO was very reluctant to discussing the potential dilution from the Madison preferred converting to the common down the line. The best we could get from him is that “there won’t be much dilution”. We don’t like that. There was recently a short thesis published by a high-caliber REIT investor on this exact issue and yet, they fail to address it when confronted on the phone.

Bottom Line

We continue to see PLYM as a high risk / high reward play. The main difference is that the share price is now much greater than when we initially invested in the company. The yield is also lower and the upside potential has diminished. Yet, the risks have risen and the thesis has deteriorated in our opinion. The deleveraging plan appears to have been delayed, massive share issuances at discounts to NAV continue, and the anticipated dilution from the Madison preferred equity conversion will continue to weight on the shares.

PLYM is one of those REITs that will either deliver very big if they can meet their optimistic guidance, but there is a fairly high chance of a miss – which would lead to material downside due to the highly leverage balance sheet and dilution from share issuance.

Moreover, if and when the cycle finally turns, PLYM could be hit with a perfect storm: excessive leverage, short leases, old poorly located assets, missed guidance, and dilution. The anticipated reward from them achieving all their promises is not sufficient to justify the risk at the current share price.

We rather invest in Monmouth Real Estate (MNR) – a higher-quality peer that owns Class A e-commerce oriented industrial assets, has a conservative balance sheet, and backed by a management team that keeps buying shares.

Fedex Ground, Mesquite – Typical property owned by MNR:

MNR is currently our Top Pick among industrial REITs and we own an outsized position at 7.5% of our Core Portfolio:

We rate PLYM a Hold for high-risk tolerant investors with a long investment horizon. We rate it a Sell for other investors.

We rate MNR a Strong Buy.

===

Heads Up!

I will be flying to Singapore on Sunday. I will be staying there for a full month to meet with REIT management teams and tour property investments. We expect to launch a new series entitled "Asian REIT Opportunities" in which we will highlight our Top 5 Picks of Asia. The first article should be up this week end. Stay tuned!

Good investing from your HYL Research Team,

Jussi Askola