Interview With The CEO Of FarmTogether On Farmland Investing

Recently, I published a public article on Seeking Alpha explaining why I think farmland could be a smarter diversifier than gold for many investors.

That article sparked a lot of interest among High Yield Landlord members, and many of you followed up with questions about farmland investing.

That did not surprise me. Farmland has many of the qualities that investors seek in gold. It is a hard asset, limited in supply, and potentially attractive in times of inflation, high deficit spending, and broader market uncertainty. But unlike gold, farmland is also productive. It generates income, and over time, that combination of yield, scarcity, and inflation protection can make it a very compelling asset class.

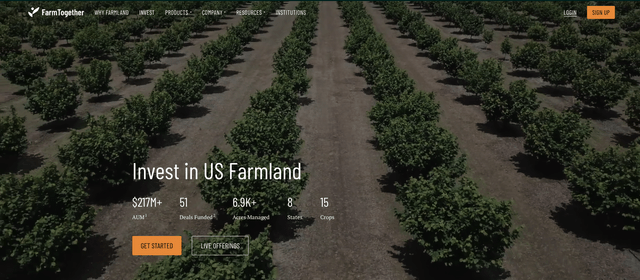

Because of your interest, I reached out to my connections at FarmTogether, one of the leading farmland crowdfunding investment firms, to set up a Q&A with their CEO, David Gould.

In the interview below, we discuss why farmland is attracting more attention today, where they are currently finding the best opportunities, what separates a great farm investment from an average one, how technology and AI are improving farm productivity, and how farmland compares with gold as a store of value and portfolio diversifier.

In the conclusion, I will also discuss how this all relates to REITs and how to best invest in this asset class.

You can learn more about FarmTogether by clicking here.

Q&A Interview With The CEO of FarmTogether

1) What makes farmland a compelling investment in 2026, in your opinion?

Farmland sits at a rare intersection of income generation and long-term capital preservation.

Productive land is a finite, essential resource — the world needs to eat, and you can’t manufacture more high-quality farmland. In an environment where investors are still navigating inflation uncertainty and equity volatility, farmland offers something genuinely different: stable cash flows from leases, real asset backing, and a return profile that isn’t correlated to the broader market.

The opportunity in the U.S. farmland market is immense — we’re talking about a $3.5 trillion asset class that has historically been accessible only to large institutions and ultra-high-net-worth families. That’s starting to change, and we’re right in the middle of that shift.

2) How is your investment strategy today, and how has it evolved in the past few years?

When FarmTogether started, the focus was primarily on opening up farmland to accredited investors through crowdfunded offerings — making the asset class more accessible. That mission hasn’t changed, but the strategy has matured significantly. We’ve built out five distinct investment vehicles: crowdfunded offerings, sole ownership bespoke offerings, tenancy-in-common structures (which can be 1031 exchange-eligible), separately managed accounts, and our Sustainable Farmland Fund. We’ve also deepened our emphasis on permanent crops — almonds, pistachios, citrus, apples, and now avocados — which are more operationally complex but offer meaningful upside when managed well.

And we’ve been building out institutional-grade capabilities: more rigorous underwriting, dedicated farm management, and a proprietary sourcing engine called Terra that helps us find high-quality off-market opportunities efficiently. The platform today serves individual accredited investors, financial advisors, and family offices — a much broader tent than where we started.

3) Where are you currently finding the best opportunities, geographically and by crop type?

Our primary focus is on high-value permanent crops in key West Coast growing regions — California’s Central Valley and San Joaquin Valley for citrus, almonds, and pistachios; the Pacific Northwest for apples; and coastal California for avocados. These regions combine favorable climates, long production histories, and established agricultural infrastructure.

One area we find particularly compelling right now are selective almond opportunities, where valuations remain depressed coming off a multi-year oversupply cycle. Acreage is contracting, export demand is recovering, and from a mean-reversion standpoint, we believe the entry point today is attractive precisely because sentiment is still cautious. Pistachios tell a different story — the industry just came off a record crop year and is entering a natural off-year cycle, but the long-term fundamentals are strong: growing global demand, constrained competition from Iran and Turkey, and a firmer price outlook as acreage growth slows.

We recently expanded into avocados for the first time with a property in Santa Barbara County, Riviera Avocado Grove, reflecting sustained consumer demand and constrained domestic supply. Geography matters enormously in all of this — water access, soil quality, and operator expertise are non-negotiable, and we won’t venture into a region unless we have the relationships and local knowledge to underwrite it properly.

4) What separates a great farmland investment from an average one in your experience?

A few things. First, the operator. Farming is a skilled business, and partnering with best-in-class operators for each specific crop type is probably the single most important variable. We maintain dedicated relationships with operators we trust, and we don’t compromise on that.

Second, water. In the West especially, water rights and irrigation infrastructure can make or break an investment — it’s something we’ve specifically added dedicated expertise for on our team.

Third, the acquisition price relative to the underlying fundamentals. We evaluate every property against a 120-point checklist covering soil health, water access, capital improvements, input costs, title, and more. It’s disciplined sourcing and disciplined underwriting — not just buying acres and hoping.

A great investment also has multiple return drivers: reliable lease income that provides downside protection, plus land appreciation potential over the hold period.

5) How do you create value beyond simply buying and holding farmland?

Active management is where we differentiate. 100% of our acreage already employs regenerative methods, such as cover cropping and reduced pesticide use, and we deploy precision agriculture tools across all of our farms — satellite imagery, soil sensors, and GPS-guided machinery to identify weak zones and adjust inputs accordingly. We also launched FarmTogether Innovation Labs, which is a formal initiative to pilot and scale promising agricultural technologies across our portfolio. The idea is to evaluate tools that can genuinely improve soil health, water conservation, and farm resilience — not for the sake of just innovation, but because improving the underlying health and productivity of the land is the most durable path to long-term investor returns. We’re also active on the operator management side, supporting property improvements and working closely with our farm management partners on cost structure and yield optimization.

6) Do you see technology, including AI, improving productivity and margins in farming?

Absolutely, and it’s already happening on our farms. We’re currently piloting precision soil analysis technology across several of our Washington apple orchards. AI-driven analytics, advanced irrigation systems, and automation are all areas we’re evaluating through Innovation Labs. The potential is real — better data on soil health means more precise fertilizer application, which reduces input costs and improves yields. Water management technology is particularly important in California and the Pacific Northwest, where water scarcity is a growing structural issue.

Our view is that technology adoption has to pass a fiduciary test: does it actually improve land performance and investor returns, not just sound impressive? But when it does, we move on it. The farms that integrate these tools thoughtfully will have a meaningful cost and productivity advantage over the next decade.

7) What is your outlook for farmland over the next 5 to 10 years? How sensitive are your returns to changes in interest rates and inflation?

The long-term structural case is strong. Global food demand is projected to rise significantly by mid-century, productive land is finite, and institutional capital is still meaningfully underallocated to the asset class. Farmland’s return profile is unusual because it combines steady cash income — through lease agreements and crop-share structures — with the potential for long-term land appreciation driven by factors like productivity improvements and scarcity of high-quality acreage.

On rate sensitivity: farmland is actually one of the more resilient real assets in a higher-rate environment. Unlike commercial real estate, farmland’s income isn’t driven by cap rate expansion — it’s driven by biological necessity. Crops get planted and harvested regardless of the Fed funds rate. That said, higher rates can pressure land values at the margin, since buyer financing costs more. On inflation, farmland is genuinely well-positioned — land values and commodity prices tend to move with inflation over time, making it a real hedge rather than a nominal one. Even in 2024 — a rare down year for the index, and the first negative annual return in the index’s history — income returns remained positive, cushioning the impact of declining land values. That dual-driver structure is what makes farmland resilient across rate and inflation cycles.

8) How would you compare farmland to gold as a store of value and portfolio diversifier?

Both are real assets that hold value over time and offer historically low correlation to equities — but farmland does something gold simply can’t: it generates income. Gold sits in a vault. A well-managed farm produces crops year after year and pays distributions to investors.

Farmland also has a productive use case that anchors its intrinsic value — people need to eat, and that demand is not going away. Gold’s value is more sentiment-driven. For investors looking to diversify and preserve capital, farmland offers what gold offers, plus an income stream and the possibility of appreciation driven by real economic activity. The tradeoff is liquidity — farmland is typically less liquid than gold, which is why we’ve built multiple product structures to give investors options that fit their liquidity needs and investment horizons.

9) How is your investment structure designed to align your interests with investors?

Our fee structure ties our compensation to performance rather than just assets under management. Our Sustainable Farmland Fund, for example, is structured as an open-ended evergreen fund with a focus on generating consistent income — it has outperformed the NCREIF Farmland Index for three consecutive years and generated cash yields in line with its 4–6% target. We also offer 1031 exchange-eligible structures for investors with specific tax needs — that kind of flexibility comes from genuinely trying to solve for what investors need, not just what’s convenient for us to offer.

Conclusion

My main takeaway from this Q&A is that farmland remains a highly attractive real asset, but successful investing in it requires far more than simply buying land and hoping for appreciation.

The interview highlights several key points. Farmland combines real asset protection, income generation, and long-term appreciation potential. The best opportunities are highly selective, with geography, crop type, water access, and operator quality driving outcomes. Active management also matters a lot, as better underwriting, technology, and strong operating partners can materially improve returns.

The discussion also reinforces why farmland can be an interesting diversifier. Like gold, it can help preserve value over time, but unlike gold, it is a productive asset that generates cash flow.

That said, accessing farmland is not straightforward.

Publicly listed options are very limited, with Farmland Partners (FPI) and Gladstone Land (LAND) being the main choices. In most cases, I strongly prefer public REITs over private investments. They offer better liquidity, transparency, and often better alignment.

However, farmland is a rare exception.

First, both of these REITs are highly leveraged, which makes them significantly riskier than the underlying asset class would suggest. Second, they have had management issues historically, particularly Gladstone Land, which is externally managed. Third, the public farmland REIT market remains immature and tends to trade in line with broader REITs and equities, meaning that you do not fully capture the diversification benefits that farmland should provide.

Because of this, I think it can make sense to look at private options in this specific case, including platforms like FarmTogether.

If you are looking for a publicly listed option, my favorite otpion is the preferred equity of Gladstone Land in our Retirement Portfolio. It offers a ~7.3% yield and trades at roughly a 20% discount to par, providing margin of safety. In my view, this is the best publicly listed way to gain exposure to farmland today.

But to build a more complete allocation, I would seriously consider complementing this with private investments.

Overall, this was a useful conversation, and it offers valuable insight into how one of the leading firms in the space is approaching the opportunity set today.

You can create an account and learn more about FarmTogether by clicking here.

Finally, please note that we have exceptionally posted this article without a paywall. If you found it valuable, consider joining High Yield Landlord for a 2-week free trial.

We expect to share a Trade Alert with our paid members tomorrow, and by starting your free trial today, you will also gain access to it. You will also get immediate access to my entire REIT portfolio, our exclusive REIT CEO interviews, and much more. We are the largest and highest-rated REIT investment newsletter online, with over 2,000 paid members and more than 500 five-star reviews.

We spend thousands of hours and over $100,000 per year researching the market for the most profitable investment opportunities, and we share the results with you at a tiny fraction of the cost.

Get started today - the first 2 weeks are on us:

Analyst’s Disclosure: I/we have a beneficial long position in the shares of all companies held in the CORE PORTFOLIO, RETIREMENT PORTFOLIO, and INTERNATIONAL PORTFOLIO either through stock ownership, options, or other derivatives. We also own a position in FarmTogether. High Yield Landlord® (’HYL’) is managed by Leonberg Research, a subsidiary of Leonberg Capital. All rights are reserved. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The newsletter is impersonal and subscribers/readers should not make any investment decision without conducting their own due diligence, and consulting their financial advisor about their specific situation. The information is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The opinions expressed are those of the publisher and are subject to change without notice. We are a team of five analysts, each contributing distinct perspectives. Nonetheless, Jussi Askola, the leader of the service, is responsible for making the final investment decisions and overseeing the portfolio. We do not always agree with each other, and an investment by Jussi should not be taken as an endorsement by other authors. Past performance is no guarantee of future results. Our portfolio performance data is provided by Interactive Brokers and believed to be accurate but its accuracy has not been audited and cannot be guaranteed. Our portfolio may not be perfectly comparable to the relevant index. It is more concentrated and may at times use margin and/or invest in companies that are not typically included in REIT indexes. Finally, High Yield Landlord is not a licensed securities dealer, broker, US investment adviser, or investment bank. We simply share research on the REIT sector.

I have been interested in investing in Farmland, but have never found any good REITs that convinced me. Perhaps BrasilAgro in Brasil.

Jussi this is a very interesting and helpful discussion. Farmland and forestry investments have not been available to retail investors at least not in my lifetime. Could you speak a little bit more or do a deeper dive into Farmland Partners FPI and other REITS that are already established that could potentially allow for easy diversification into this sector?