IWG Is A Potential Multibagger In The Making (Q1 2026 Update)

International Workplace Group (IWG / IWGFF) remains our single largest position, and for good reason.

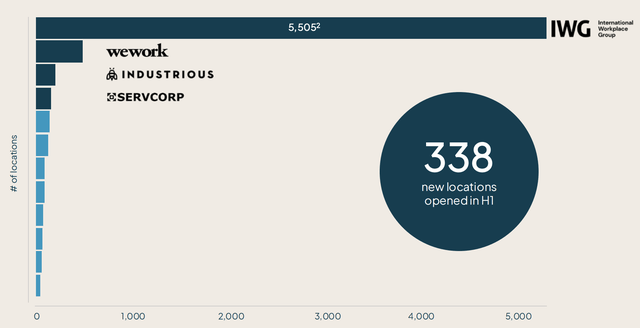

For those less familiar with the company, IWG is the global leader in flexible office space. It operates nearly 6,000 coworking and serviced office locations across more than 120 countries under brands such as Regus and Spaces. In simple terms, it provides flexible workspace solutions to businesses of all sizes, increasingly through a capital-light partnership model with landlords.

I continue to believe that it is a multibagger in the making because the company is in the middle of a major business transformation that the market still does not fully appreciate. Historically, IWG was viewed as a capex-heavy, cyclical office business.

But that is no longer the right way to think about it. It is increasingly becoming a capital-light, fast-growing, more resilient platform that helps landlords monetize vacant space and helps tenants access flexible office solutions on demand via partnership models.

That transformation is creating a much better business. It requires less capital, carries less lease liability risk, grows faster, and should ultimately deserve a much higher valuation multiple. At the same time, management is using the company’s strong cash flow and balance sheet to aggressively repurchase shares while the stock still trades at a deeply discounted valuation. That combination, improving business quality, rising cash flow, multiple expansion potential, and heavy buybacks, is what makes this such an attractive long-term opportunity.

The latest results only reinforced that thesis.