MARKET UPDATE - Hard Asset Reckoning: The End Of The Asset-Light Era

Over the past year, we have published several articles explaining why we think AI is set to significantly disrupt the economy, financial markets, and equity valuations.

In short, I think that a large fraction of today’s businesses are likely to suffer significant AI-driven value destruction over time, just as SaaS companies already have.

This should ultimately benefit the rare assets that are immune to AI disruption.

We are already seeing this play out through what I have called the “AI Immunity Trade”. REITs are up sharply this year, even as interest rates have surged, because more capital is starting to rotate away from AI-disrupted businesses and into AI-resilient real assets.

I recently came across the following piece from Groundbreaker, an independent analyst focused on real assets, and I thought it made some very interesting points.

The core idea is that the asset-light era may be coming to an end, and that this could greatly benefit hard asset businesses like REITs.

It is a long essay, about 6,000 words, but it is very comprehensive and well worth the read. I received authorization from the author to repost it here.

I agree with his take, and it is one of the main reasons why I am so bullish on REITs and maintain such large exposure to them.

If you find his analysis useful, you can also follow him by clicking here.

— Electric Choice")

Hard Asset Reckoning: The End Of The Asset-Light Era

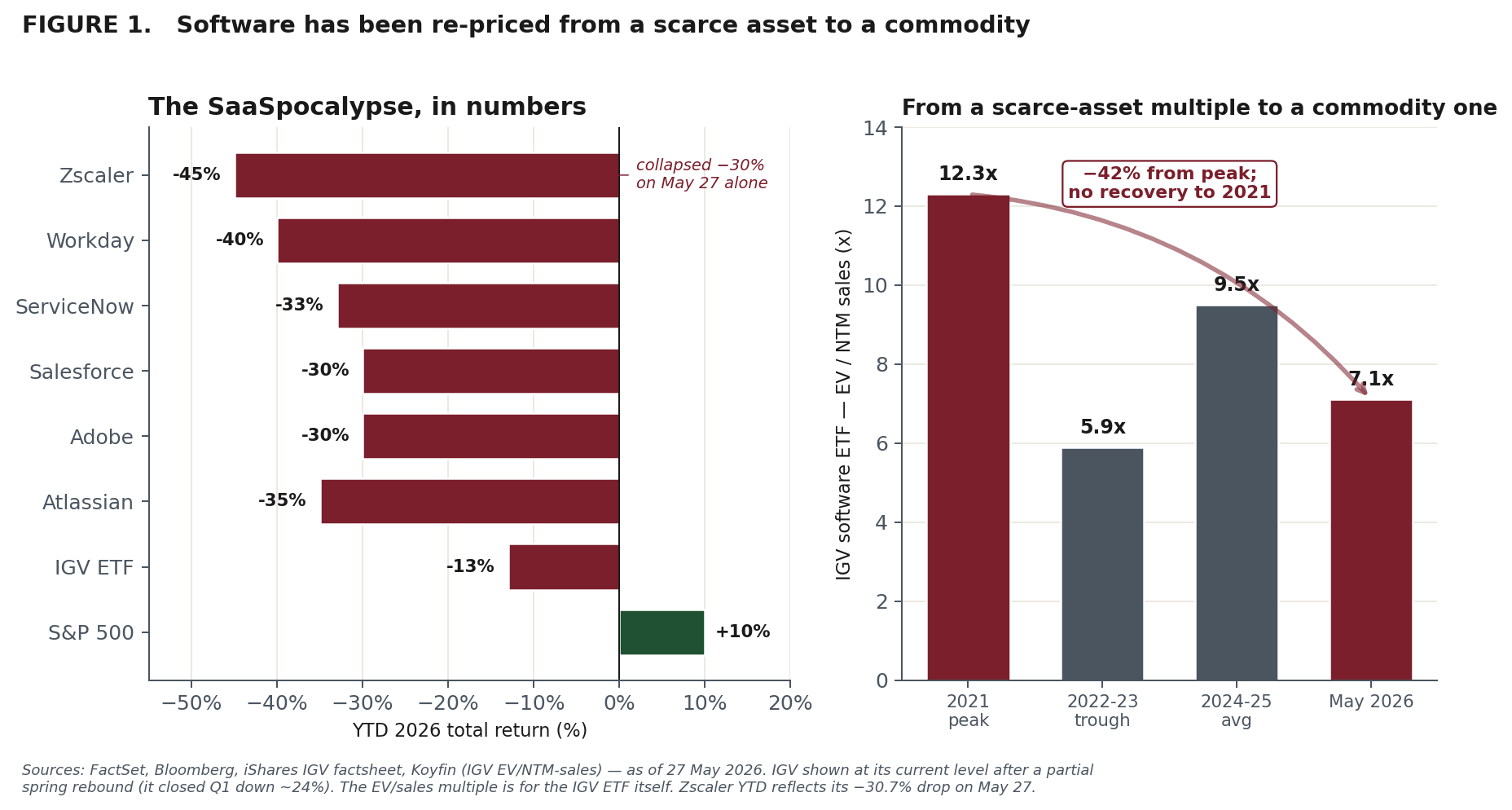

On February 3, 2026, roughly $285 billion in market capitalization evaporated from the software sector in a single trading session. Salesforce was down 30% on the year. Workday had dropped more than 40% from its twelve-month high. Atlassian had lost 35%. The iShares Expanded Tech-Software ETF (IGV) entered a technical bear market, off more than 20% for the year - in five weeks. Analysts coined a term for it: the SaaSpocalypse.

The catalyst was not a recession, a credit event, or a geopolitical shock. It was the proliferation AI. Two assumptions the entire software industry had been priced on broke at once: that producing useful software was hard, and that the number of humans using it would only grow. AI broke both.

For thirty years, building enterprise software at scale required engineering teams, multi-year roadmaps, and tens of millions of dollars of capital. AI-assisted code generation has collapsed that cost curve. A motivated team can now ship a credible internal tool or feature that a $20B SaaS incumbent charges handsomely for - in weeks, not years. When the production function for software is commoditized, the premium collapses with it - most steeply for the companies whose moat was the software itself rather than the system of record beneath it.

And as recently as yesterday - Zscaler stock collapsed roughly 30% in a single session after beating Q3 on both lines but guiding softer for the next quarter. Wall Street treated a single soft guide as confirmation that demand itself, not just multiples, is now the story. Even strong cybersecurity names are no longer being granted the benefit of the doubt.

The clearest single statistic: the IGV software index now trades at roughly 7x forward EV/sales, down from a 2021 peak above 12x. The premium the market once paid for software being scarce and defensible has been structurally re-rated away.

On the same days software cratered, Caterpillar, Deere, Southern Copper, and Constellation Energy traded at or near record highs. The market was not panicking. It was reallocating - away from business models built on the assumption that code is scarce and atoms are cheap, toward business models built on the recognition that code is becoming free and atoms are becoming priceless.

This article is about that reallocation: why the thirty-year dominance of asset-light business models is ending, why the next ten to twenty years will belong to owners of hard, physical, scarce assets, and why the investors who understand this shift earliest will capture some of the most asymmetric returns of their careers.

I. The Asset-Light Orthodoxy: How We Got Here

The intellectual origin

The preference for asset-light business models did not emerge from nowhere. It was a coherent response to conditions that prevailed from roughly 1995 to 2020. The internet made distribution free. Cloud computing made infrastructure rentable by the hour. Software-as-a-service made enterprise tools accessible without capital expenditure. The rational strategy was obvious: own the code, rent the atoms. Build the platform, let someone else build the data center. Design the marketplace, let someone else own the inventory.

The financial logic was seductive. Asset-light companies posted higher returns on invested capital because there was less capital to invest. They carried wider margins because they had fewer physical costs. They scaled faster because scaling code costs nothing at the margin, and they were more resilient in downturns because variable costs could be cut instantly while asset-heavy competitors were stuck paying for fixed infrastructure. During the 2020 shock, asset-light companies recovered roughly 2.5x faster than asset-heavy peers.

The market rewarded the strategy lavishly. At the 2021 peak, the median enterprise-software company traded at 12–13x revenue. The entire venture-capital industry was oriented around the model: build a SaaS product, acquire customers at a loss, demonstrate recurring revenue, point to a land-and-expand trajectory, and raise at an ever-higher multiple. By 2021 there were over 15,000 SaaS companies globally. Software had, as Marc Andreessen famously declared, eaten the world.

The hidden consequence: systematic underinvestment in physical assets

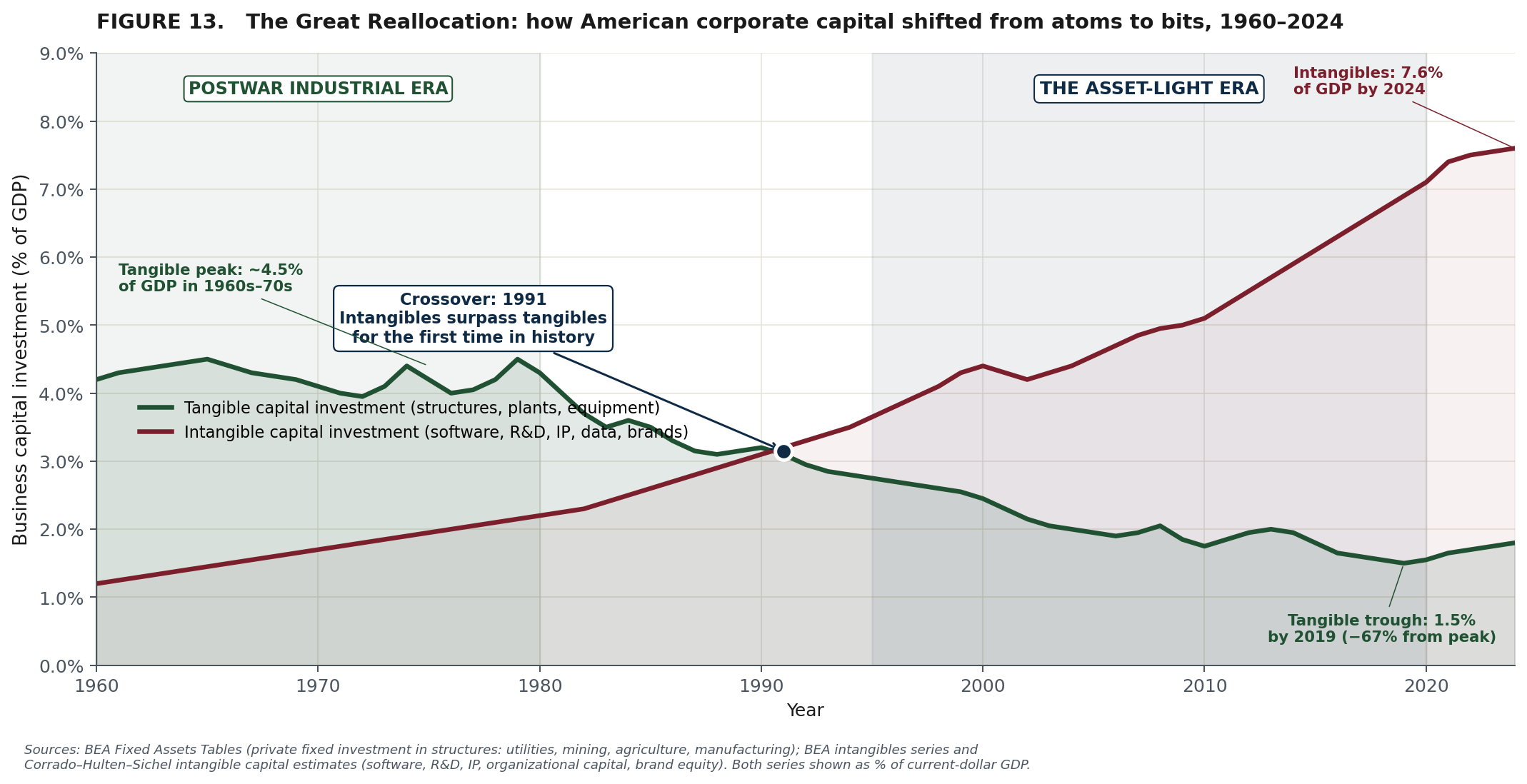

But while the smartest capital in Silicon Valley poured into code, something else was happening - or precisely, not happening - in the physical world. Capital expenditure on hard assets across the American economy was declining as a share of GDP. Infrastructure was aging. Bridges deteriorated. Power grids strained. Water systems corroded. Mines closed. Farmland was converted to suburbs. Refineries shut down. Pipelines went unbuilt.

The numbers are stark. The American Society of Civil Engineers has graded U.S. infrastructure a D+ or C− for over two decades. More than $1 trillion in water-infrastructure upgrades are needed; the power grid requires an estimated $2.5 trillion to meet projected demand. The U.S. lost an average of 4.3 acres of farmland every minute from 2000 to 2022. Domestic mining capacity for critical minerals declined for decades. Since 2020, the housing-construction shortfall has grown to an estimated 3–5 million units.

This underinvestment was not accidental. It was the logical consequence of a capital-allocation regime that systematically rewarded asset-light models and punished capital intensity. Every dollar that went into a SaaS startup was a dollar that did not go into a power plant, a water-treatment facility, a mine, a pipeline, or a farm. The market was extremely efficient at funding the highest-return, lowest-capital-intensity opportunities - and extremely inefficient at maintaining the physical substrate on which everything else depends.

The result is a paradox only now becoming visible: three decades of optimizing for asset-light models created the conditions under which hard assets are more valuable than they have been in a generation. The scarcity was manufactured by the orthodoxy itself.

II. The AI Inflection: Why Asset-Light Moats Are Dissolving

What AI can replicate - and what it cannot

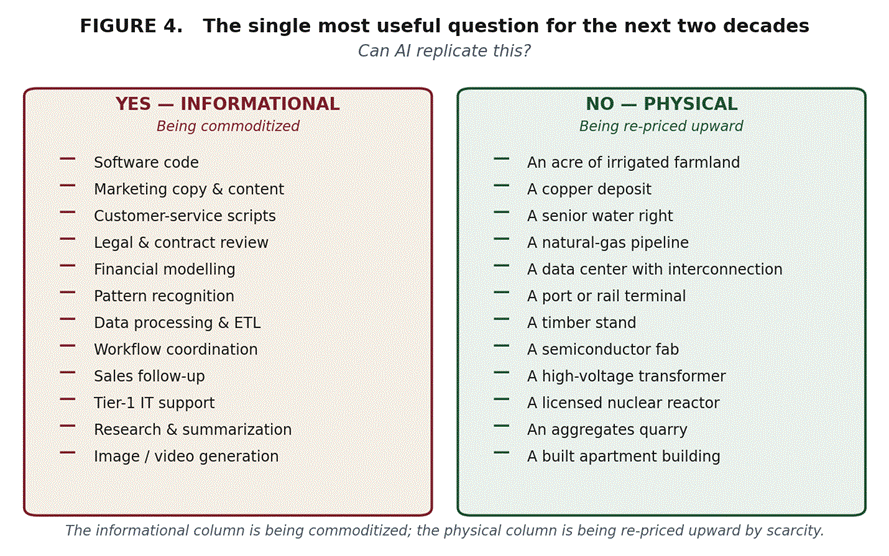

This is the critical analytical framework for the next decade. AI can replicate anything fundamentally informational: code, content, analysis, pattern recognition, workflow coordination, data processing, customer-service scripts, marketing copy, legal review, financial modeling. These are the activities asset-light businesses are built upon. When AI produces 90% of the quality at 1% of the cost, the moat of being the best software tool for a task dissolves.

What AI cannot replicate is anything fundamentally physical: an acre of irrigated farmland, a copper deposit, a water right, a natural-gas pipeline, a data center with power interconnection, a port terminal, a timber stand, a semiconductor fab, a rail network, a transmission line. These assets exist in the physical world, are constrained by geology, geography, regulation, and physics, and cannot be conjured by an algorithm regardless of how intelligent it becomes.

The market is beginning to reflect this. As of mid-2026, infrastructure-investment volumes are outpacing global GDP growth, the utilities sector has entered what analysts describe as a capital-expenditure super-cycle, and the irony is complete: AI - the most powerful informational technology ever created - is the greatest catalyst for physical-asset revaluation in modern history, because AI itself requires staggering quantities of electricity, cooling, land, water, and physical infrastructure to operate.

Big Tech is no longer buying bits - it is buying atoms

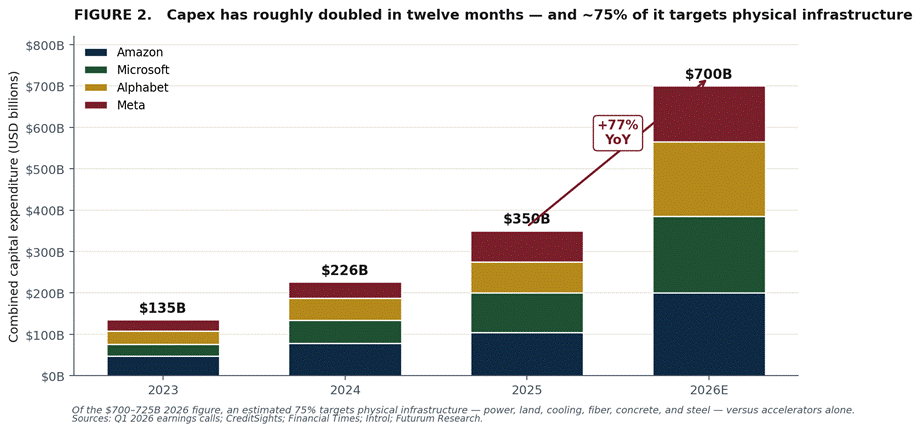

Nothing illustrates the inversion more vividly than the hyperscalers’ own balance sheets. At the beginning of 2026, the five largest cloud providers were guiding to $660–$690 billion of 2026 capital expenditure. Then first-quarter earnings landed in late April. Every major hyperscaler raised its guide. Microsoft set calendar-2026 capex near $185 billion; Alphabet raised toward $180–$185 billion; Meta lifted its range to $125–$145 billion; Amazon held at roughly $200 billion. Together, the four largest now plan to spend on the order of $700–$725 billion this year - up roughly 77% from 2025’s record $410 billion, and more than triple 2024.

Approximately 75% of that spend targets physical infrastructure rather than chips alone. Microsoft attributed about $25 billion of its 2026 figure to component-price inflation; Amazon’s free cash flow is expected to turn negative on the build-out; Alphabet’s CEO described the company as “compute-constrained.” Every dollar is demand for electrons, copper, fiber, water, and land. AI is not dematerializing the economy. It is rematerializing it at unprecedented scale.

AI is the most asset-heavy technology ever deployed

This deserves to be stated plainly, because it inverts thirty years of intuition. Every prior wave of computing was celebrated for dematerializing the economy - the PC, the internet, mobile, the cloud, and SaaS all promised to do more with fewer atoms, replacing warehouses with websites and filing cabinets with servers somewhere out of sight. AI breaks the pattern. It is the first major general-purpose technology in modern history that is more physically intensive than what it displaces, by orders of magnitude. The “cloud” was always made of concrete, copper, and water; AI simply makes that physicality impossible to ignore.

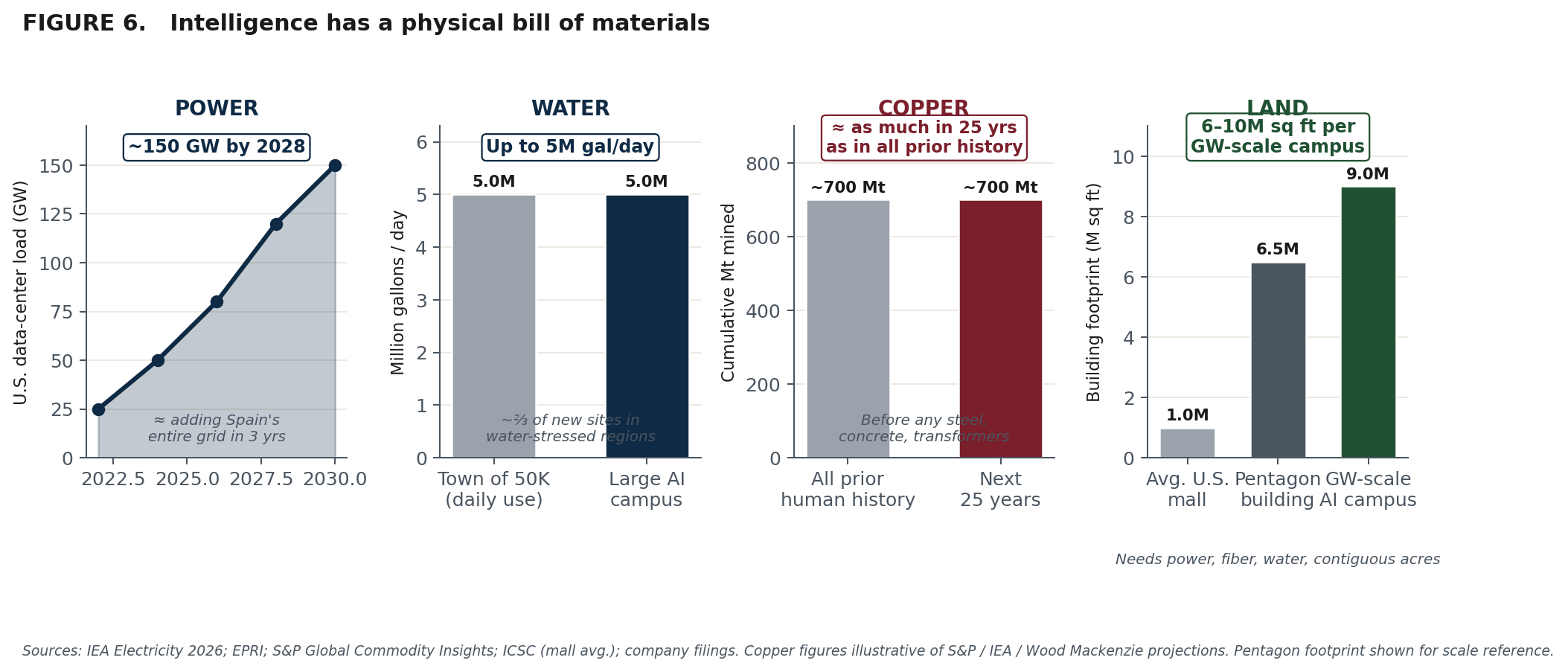

Consider the bill of materials:

On power, U.S. data-center demand is projected to climb from roughly 80 gigawatts toward 150 by 2028 - the equivalent of bolting Spain’s entire electricity system onto the grid in three years. Meta’s Louisiana campus is expected to consume more than twice the power of New Orleans.

On water, a single large campus can evaporate up to five million gallons a day - the draw of a town of fifty thousand - and roughly two-thirds of new sites are being built in already water-stressed regions.

On materials, the copper alone required to wire AI and the broader electrification it accelerates may oblige the world to mine as much copper in the next twenty-five years as has been mined in all of recorded human history - before counting the steel, concrete, fiber, transformers, and switchgear now on multi-year backorder.

On land, the campuses themselves are becoming small cities: gigawatt-scale sites now run six to ten million square feet of building footprint on thousands of acres of contiguous, fiber-connected, power-served real estate - a combination of attributes that exists in very few places in the United States and cannot be manufactured by zoning reform alone.

And this doesn’t even include the power generation. A single gigawatt of solar requires roughly five to ten thousand acres of land. A gigawatt of nuclear, can evaporate hundreds of millions of gallons of cooling water annually. Even natural gas requires upstream pipeline corridors, water for cooling, and decade-scale permitting timelines for new long-haul capacity. The implication is that AI’s physical footprint is recursive: each new gigawatt of data-center load compounds into thousands of acres of generation footprint and millions of gallons of additional water draw.

This is the deepest reason the bits-to-atoms reallocation is structural rather than cyclical. The dominant technology of the era does not merely coexist with hard assets; it is the largest new source of demand for them. The same force commoditizing the informational economy is, by physical necessity, the most powerful bid for the physical one.