MARKET UPDATE - The Bear Thesis For REITs (Debunked)

MARKET UPDATE - The Bear Thesis For REITs (Debunked)

REITs are down 33% year-to-date and they appear to be only going lower day after day. In fact, if you read comments on REIT-related articles on Seeking Alpha, you will find that a lot of people appear convinced that REITs will suffer much larger losses in the coming quarters.

What's their bear thesis?

I have seen many theories, but it really boils down to two main things:

Bear thesis #1: rising interest rates will hurt REIT's profitability.

Bear thesis #2: rising interest rates will cause property values to decline.

Let's review both theses one by one:

Bear thesis #1: rising interest rates will hurt REIT's profitability.

Yes, in theory, if all else is held equal, then higher interest rates would result in lower profits and slower growth for a leveraged company.

But in real life, all else is never held equal, and there is a reason why interest rates are rising. Today, interest rates are rising because of high inflation, which results in growing rents.

Therefore, you cannot ignore other important factors like inflation as you attempt to determine the impact on profitability.

The question to ask yourself is which has a bigger impact: the rising interest rates or the high inflation?

And the answer is very clear: the high inflation has a far greater positive impact on revenue than the rising interest rates have on costs.

That's because:

Most REITs use little debt with a 35% LTV on average.

Most REIT debt is fixed rate and maturities are long.

Inflation is today at a 40-year high, reaching nearly 10%.

Even post-rate hikes, interest rates remain low relative to inflation.

REITs retain a lot of cash flow and can pay off their small debt maturities with retained cash flow and/or capital recycling.

Therefore, the positive impact of high inflation is a lot greater than the negative impact of rising interest rates. The inflation rate is far greater than the interest rates and inflation affects 100% of the assets, whereas debt affects only 35% of the assets. Besides, even that's not really true since that 35% does not need to be refinanced any time soon. The average debt maturity is 8 years in the REIT sector, which means that their rents will often have many years to grow before they even feel the impact of rising rates. This also leaves REITs the flexibility to pay off some of that debt before it matures if desired.

Debt is at an all-time low:

Maturities are the longest ever:

Rents are growing the fastest in decades:

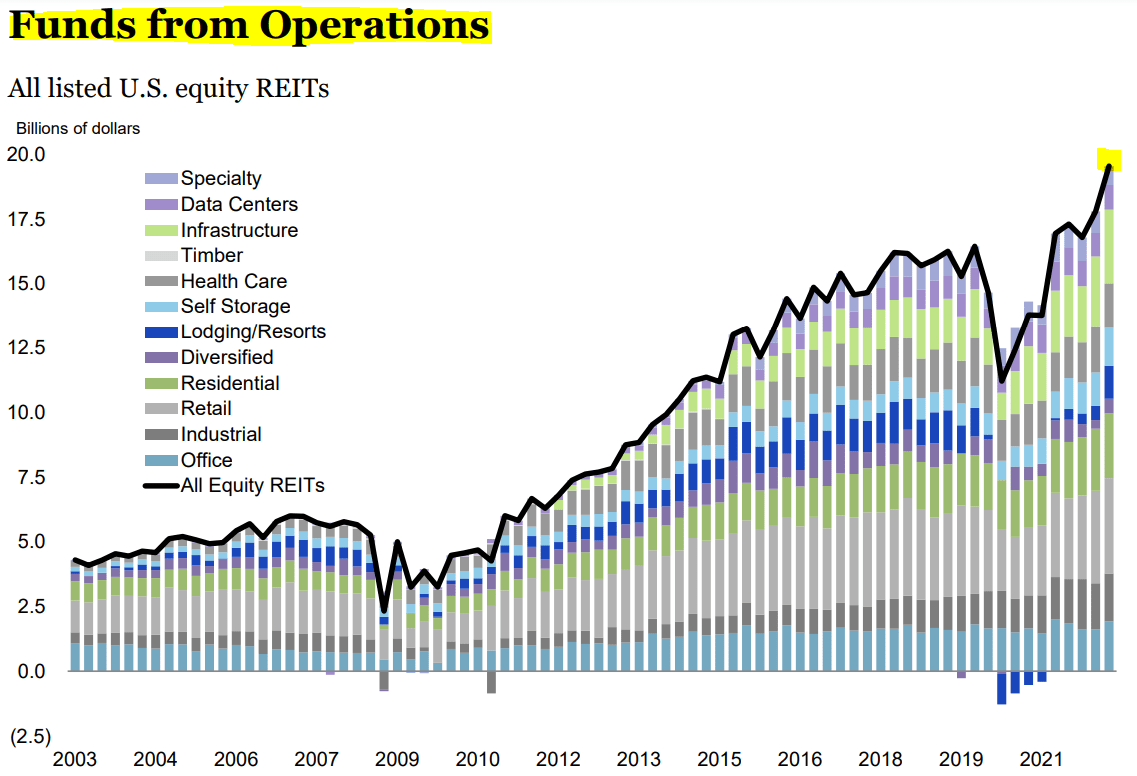

REIT cash flows are hitting new all-time highs, despite rising rates:

So the #1 bear thesis, which relates to REIT profitability, is clearly flawed. REIT cash flow has been growing far faster than its historic averages with some property sectors experiencing some of the fastest rent growth in decades. Over 100 REITs have also hiked their dividends in 2022 and only a few exceptions have cut it, which again shows you that this thesis is wrong.

Profitability is rising, not declining. But perhaps, there is more to the second thesis:

Bear thesis #2: rising interest rates will cause property values to decline.

This point is more complicated and there is more substance to this bear thesis.

Commercial real estate is valued based on two main things:

Its net operating income, or NOI in short.

Its capitalization rate, or its cap rate in short.

The higher the NOI, the higher the property value (and vis-versa):

And the lower the cap rate, the higher the property value (and vis-versa).

The cap rate is mainly a function of the risk of the property and its growth prospects, but also the risk-free rate, which has an impact on the investor demand for real estate.

Therefore, all else held equal, you would expect a higher risk-free rate to result in higher cap rates, which then result in lower property values and NAVs for REITs.

In some property sectors, cap rates had dropped to historically low levels in the past years and this was at least in part due to the low interest rate environment. Therefore, the higher interest rates certainly could cause cap rates to expand in some property sectors like apartment communities, which today still sell at exceptionally low cap rates.

But here is why this is not so clear:

Firstly, the NOI is also rising rapidly in most property sectors, which naturally, causes property values to rise. As an example, EastGroup Properties (EGP) has been hiking rents by 20%+ at its industrial properties and this rapid growth is expected to continue because its rents have not kept up with the inflation and are currently below market. So yes, cap rates could expand some, but since NOI is rising so rapidly, it does not mean that property values will decline.

Secondly, most property sectors still offer a nice spread over the risk-free rate. Today, the risk-free rate of treasuries might be 4%, but high-quality net lease properties offer a 6-7% cap rate, which represents a generous risk premium. What investors appear to forget is that when interest rates hit 0%, the spreads were temporarily abnormally high. Now, the spreads are simply normalizing in many property sectors and so it does not mean that cap rates will expand across the board. They may expand in some property sectors, but not all. Being selective is key as always.

Finally, the investor demand for real estate is not just a function of interest rates. Again, we cannot just ignore other factors which are important today. Inflation is a particularly big one. Investors fear it dearly, especially the bigger ones like pension funds, which are really driving most of the demand for commercial real estate.

Yes, the risk-free rate is now 4% and it leads many to wonder, why would someone want to buy an apartment community at a 4% cap rate. There is no spread and it is riskier they claim. But what they forget is that it is the "real" risk-free rate that really matters. Today, if you buy treasuries at a 4% interest rate, you are guaranteed to earn a negative return after taxes and inflation, and therefore, it is simply not sustainable for most investors to go all in on treasuries. The inflation is at 8% so that's a guaranteed loss.

This is very unusual:

Sure, you could say that the real returns of the apartment community likely won't be very high either and you would be correct, but at the very least, the investor is protected against the long-term impact of inflation as rents will grow and so will the replacement cost of the real estate. If the property is well-located, the long-term growth in rents and value will more than make up for the near-term lack of real returns. Here is what Blackstone (BX) recently said on this specific topic:

"My hard assets are interesting in an environment like this is because the replacement cost goes up pretty significantly. In inflationary environment, the cost to build the labor cost, which is a big component has gone up and probably the largest input cost of money goes up significantly. And the yield on cost that you need to build a new project goes up. So I was talking to a major apartment developer who builds 15,000 units he has under construction today. He said next to cut his budget to 4,000 units, a 75% decline in terms of his new construction. So what you see happen in an environment like this is you start to see a reduction in new supply, which is obviously helpful in the long-term and these hard assets are beneficial because they don't have much exposure to input costs, and there's going to be a few of them, as I said, built. So that argument for investing into hard assets... If you're in rental housing and you have pricing power or logistics, where we're still seeing in the U.S., 30% increases in rents. In Europe, nearly 20% increases in rents, the duration of [indiscernible]. Even as the cap rates go up, you can still see value appreciation, albeit at a lower rate."

They then added the following about investor demand for real estate:

"Fixed income starts to look more attractive. But if you think about our clients and their long-term obligations, the rates they want to produce are generally above investment grade fixed income. And so I don't think they can move their portfolios out of alternatives in a meaningful way. It has been their best performing sector... Recent research from Morgan Stanley estimates that private markets AUM will grow 12% annually over the next five years."

So I don't expect the demand for commercial real estate to dry up anytime soon. Blackstone (BX), Brookfield (BAM), and other major private equity firms are today sitting on more cash than ever before:

Blackstone (BX) has $182 billion of liquidity. Brookfield (BAM) has another $110 billion. These are just two of the big private equity players and they need to put this cash to work in order to earn fees.

It explains why cap rates haven't moved much or at all.

Prologis (PLD) has even able to sell industrial properties at a ~4% cap rate, despite the rising cap rates.

AvalonBay (AVB) has been recycling capital and selling properties in the high 3s or low 4s and these are some of its oldest, slower-growing apartment communities.

There are a lot of other examples, but you probably get the point here.

Cap rates and interest rates are not perfectly correlated because there are lots of other factors to take into account. Today, the high inflation is pushing a lot of investors to buy real estate, even if the spreads are now lower. They are simply accepting lower returns to protect themselves.

So to conclude here, yes, some properties may suffer some cap rate expansion, but I would not expect anything significant, and the NOI is also rising rapidly, which is another stabilizing factor.

This is exactly what Blackstone recently reported:

"Notwithstanding this impact, our real estate strategies has still seen strong appreciation year-to-date as cash flow growth and dividends have more than offset the impact of wider cap rates."

Investors should worry more about real interest rates than nominal interest rates. Inflation matters!

Bottom Line

The bottom line is that there are lots of REITs that are deeply undervalued in today's market.

REITs are down heavily due to fears that are overblown. Investors overestimate the impact of rising interest rates and underestimate the impact of inflation on the profitability of REITs and their long-term fair value.

Right now, there are some REITs that trade at just 50 cents on the dollar or even less. This essentially means that you are getting $200,000 worth of real estate for every $100,000 that you invest. Even if the real estate dropped a little in value, you would still likely come out well ahead in the long run.

Where else can you get such deals today?

Good investing from your HYL Research Team,

Jussi Askola