Middle Eastern REIT Opportunities: Introduction - Part 1

Middle Eastern REIT Opportunities: Introduction - Part 1

Unique to High Yield Landlord is our International approach to real estate investing. Having lived and worked in many different countries (Finland, France, Germany, Wales, Estonia, and the USA), I understand that the best opportunities are not always in your home country.

To give you an example: despite currently living in Europe, I have favored US REITs over the past years. Cap rates are greater, NOI is growing faster, there is better appreciation potential and you could easily make the argument that it is also a safer market.

Greater reward potential… with lower risk… is what has driven our large allocation to US REITs so far. We have also identified opportunities in Europe and Asia, but they have been few and irregular.

A region that could present very promising investment opportunities is the Middle East. Unfortunately, because we lack “boots in the ground”, we have not been able to identify any Middle Eastern REIT opportunities so far.

In an effort to finally learn more about Middle Eastern REITs, I committed to a 1-month long field trip to the Middle East.

I am currently in Dubai to meet with REIT management teams, discuss market trends with local experts, tour properties, and ultimately, identify the Best Middle Eastern REIT opportunities for members of High Yield Landlord.

In today's article, we provide an introduction to the Middle Eastern REIT market. In future episodes of this series, we will focus on specific companies.

The Middle Eastern REIT Market

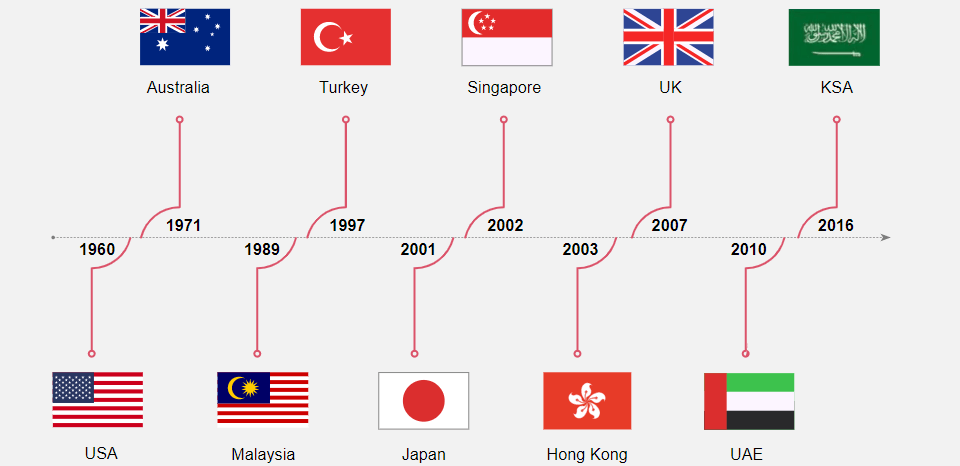

The REIT market is still very new in the Middle East. The first REIT was created in 2010 in the United Arab Emirates ("UAE"), and the second REIT was created six years later in Saudi Arabia:

Think about it: That means that most Middle Eastern REITs have existed for less than 3 years.

That's a first warning sign for investors.

New and emerging REIT markets present opportunities, but they also present much greater risks. There isn't a well-established community of REIT analysts to look over the actions of management teams, and as a result, the conflicts of interest are more significant in these markets.

Today, REITs still don't exist in all Middle Eastern countries. Rather, they are mainly concentrated in the Gulf Cooperation Council, also known as GCC, which is a regional economic union consisting of:

The United Arab Emirates

Saudi Arabia

Oman

Qatar

Bahrain

Kuwait

In case you haven't been to the region, here is a further zoomed out screenshot of the world map:

This region has some of the fastest-growing economies of the world, mostly thanks to the boom in oil and gas revenues, which has then also enabled an investment boom in other sectors to diversify the economy.

As an example, oil production once accounted for 50% of Dubai's GDP. Today, it is down to less than 1%, and the economy is heavily weighted toward tourism, banking, and real estate. Below is a picture of the Burj Khalifa, the tallest building in the world, which is located in Downtown Dubai:

.jpg")

.jpg){kind=link}

This does not mean that the region isn't reliant on oil, but it shows that these economies are today better diversified than they are perceived to be.

Today already, Dubai is one of the most popular tourist destinations for Europeans and Asians. It has some of the world's most luxurious hotels, biggest malls, and all of it was built over the past 30 years:

Abu Dhabi is also growing in prominence as a tourist destination. In fact, it is hosting a very big UFC event over the weekend, featuring Conor McGregor vs. Dustin Poirier in the main event. Bahrain now also has its own F1 Grand Prix that it organizes each year.

These events highlight the region's efforts to grow its tourism and service industries. Long-term, it is a good thing, but as we'll discuss below, the large investments in tourism are causing great overbuilding concerns in the near-term.

Getting back to REITs, the legal structure and requirements are similar to that in the US:

They are required to payout 80-90% of net profits.

They are not subject to any corporate taxes.

Most assets must be income-producing real estate.

Many of these countries do not have any corporate or income tax. As a result, they also don't charge a withholding tax to foreign REIT shareholders, which is a big advantage for us.

What are some of the differences relative to US REITs?

First of all, practically all Middle Eastern REITs are externally managed, which leads to greater conflicts of interest as discussed in Module #2 of our Course to REIT Investing. This should be your number one concern when investing in this region of the world: is the management well-aligned with shareholders?

Secondly, most Middle Eastern REITs are not specialized in one property sector. Instead, they invest in all property types and act as "jacks of all trades", which we generally do not like. We prefer REITs to specialize in one sector and develop competitive advantages.

Thirdly, many Middle Eastern REITs are structured in a way to be Shariah-compliant. These guidelines limit the REIT in a number of ways that may hurt their ability to earn returns. As an example, they may not be able to rent space to companies involved in alcoholic beverages or tobacco industries. They also may not invest in certain property types.

Finally, perhaps the biggest difference between the US and many of these Middle Eastern countries is the demand/supply dynamics.

The US real estate market occasionally suffers times of oversupply, but the private market has its way to work it out. As the market gets overbuilt, rents and values decline, forcing developers to put an end to new projects. Eventually, the demand catches up to the supply, and the market finds its balance again.

The Middle Eastern property market is not only regulated by private market forces, and as a result, these cycles of oversupply are often more severe than they would otherwise.

The government is one of the biggest property developers in these countries, and since they aren't in a need to earn an immediate profit, they may continue to build even at a loss if they think that it will yield good economic results in the long term.

Dubai is a perfect example of that.

The market has been severely overbuilt for close to a decade now, and even then, new constructions continue to pop-up all over the place. You see cranes in every street corner... meanwhile many of the properties are sitting half empty or even worse:

You will note that it is written "EMAAR" on the crane, and if you look closely at the buildings behind, it is also written EMAAR on some of them.

EMAAR is a public joint-venture company that is largely owned by the government of Dubai. I had a meeting with them a few days ago and apparently, they continue to build tower after tower with no worry for oversupply, even despite collapsing real estate prices:

And the worst part is that even if you invest in prime locations, it does not protect you from oversupply because they are also adding new prime locations by building man-made islands.

Below is a picture of the palm island - the largest man-made island in the world:

Today, many more of such islands are planned for construction...

They are also planning an even higher building than the Burj Khalifa...

And many more luxurious hotels, condominium and office buildings...

Dubai's approach is "build it and they will come". While it may benefit the tourism, service, and construction industries, it surely doesn't benefit the existing property owners who are constantly battling with a new wave of competing properties.

Not all Middle Eastern countries suffer the same supply issues, but it is something to keep a close eye on.

It feels that many of these countries are attempting to build their way out of oil dependency by forcing GDP diversification via massive investment in real estate and tourism.

Maybe it will prove successful in the long run, but in the meantime, real estate owners are suffering challenging conditions.

Covid Impact: Fundamentals & Valuation

Today, many Middle Eastern REITs are priced at exceptionally low valuations with deep discounts to NAV, low cash flow multiples, and high dividend yields.

But then again... this is well-justified when you consider that:

Most REITs are poorly managed by conflicted management teams.

They have no specialization or competitive advantage.

They need to abide by very specific rules that lower their profitability.

And finally, they are dealing with unfavorable supply/demand conditions that are only getting worse because of the covid crisis.

Countries like the UAE, Bahrain, Qatar etc... are heavily reliant on foreign expats as well as tourism. We all know that tourism has taken a big hit in 2020, but their reliance on expats is even more concerning to me.

To give you an example, expats form 90% of UAE's population, and therefore, their entire economic model relies on the presence of foreign residents.

But now expats are losing their jobs, visas expire, and they are forced to return home. Oxford Economics, a UK-based advisory firm, estimates that the UAE could "lose 900,000 jobs among a population of under 10 million, meaning some 10% of its residents could be uprooted".

Just to give you a sense of the impact on real estate, Emirates REITs, which owns 4 international schools in Dubai, has seen two of its schools go bankrupt and are now sitting empty.

The management indicated to me that before the crisis, these schools had a long waiting list to get enrolled. Now, waiting lists have disappeared and schools are fighting to stay alive.

If expats leave, they take their families with them, and it leads to declining demand for all sorts of real estate: schools, apartments, retail shops, hotels, offices, etc...

Overbuilding was a significant concern before the crisis so you can imagine that things are only getting worse.

Is this priced in the REIT market? Yes, but a low valuation is not enough to get us invested. We need good management, a strong strategy, a conservative balance sheet, and a clear path to long-term reward.

Bottom Line: Most Middle Eastern REITs Offer Poor Risk-to-Reward

If you read this far, you can probably tell that I am not particularly excited by what I have discovered so far. I have met with ~10 local real estate experts and none of them seem excited either.

Maybe it's just a sign that blood is on the streets, and now is a good time to buy at historically low prices?

If we could trust that the supply issue will get under control, then I would be on board of this idea, but right now, I am not convinced yet.

In the next episodes of this series, we will dive into individual REITs to avoid and some potential opportunities to consider for your Portfolio.

Good investing from your HYL Research Team,

Jussi Askola