Our Biggest Investment Has Reached Fair Value: Buy, Hold, Or Sell?

Our Biggest Investment Has Reached Fair Value: Buy, Hold, Or Sell?

The biggest contributor to our outperformance since starting High Yield Landlord has been our heavy allocation to REITs that focus on middle-market net lease properties.

We first invested in STORE Capital (STOR) during the early days of the pandemic in 2020. We had long wanted to own a position, but it was too expensive most times so when its share price crashed from ~$40 to ~$15 per share, we loaded up on it and eventually built it as our largest holding, representing >10% of our Core Portfolio.

The pandemic was, of course, a severe crisis for STOR. Everything shut down, STOR's tenants couldn't pay rent, and the market feared that STOR would face a big wave of tenant bankruptcies since it focused on weaker middle-market tenants. We have often discussed how the "short-termism" of the market can lead to market inefficiencies, and this was the case here.

The market had priced STOR as if the only things that mattered were near-term results, but in reality, real estate should be priced based on decades of expected future cash flow.

We all knew that 2020 would be a bad year, but the impact of 1 year of weaker results does not justify a >50% crash in its share price.

STOR had a great balance sheet and plenty of liquidity to face the crisis, so it wasn't facing any major solvency issues. Moreover, its leases were a lot stronger than what the market gave it credit for. Most investors saw that STOR had small tenants and quickly concluded that they would go bankrupt and leave STOR with empty buildings that would be costly to remodel and release, but they failed to recognize that STOR followed a unique strategy of acquiring net lease properties based on their strong unit-level profitability. This meant that most of its properties were highly profitable and easily able to cover their rent payments in normal market conditions. Therefore, these tenants did whatever was necessary to avoid losing these profitable assets because of a temporary crisis. Often, STOR ended up giving them a bit of breathing room by allowing them to pay late, but it still collected most of its rent payments. This was a great solution to a temporary crisis.

Eventually, we moved past the pandemic and private equity bought out the company for ~$32 per share, which was nearly double what we had paid for it about 2 years earlier when we first initiated our position. Back then, the dividend yield was also nearly 8%, so we earned substantial income while we waited for the upside.

But our investments in middle-market net lease properties did not end there.

By then, another similar REIT had emerged and replicated STORE Capital's unique model. In fact, it was modeled after it and had even potched some of STOR's top talent.

That REIT is Essential Properties Realty Trust (EPRT).

So when we sold our stake in STORE, we immediately reallocated all of it into EPRT and have held it as our largest position ever since.

Today, it represents a huge 11.4% of our Core Portfolio and it has outperformed the REIT benchmark by a ratio of 7-to-1 since we invested in the company.

The large position size coupled with the strong outperformance really pushed us ahead.

But what now?

The shares are back at near all-time highs and they are hardly a bargain anymore. They trade at 16x FFO and offer a 3.8% dividend yield, which is quite high for a net lease REIT focusing on middle-market properties in a higher interest rate world.

This recently prompted us to downgrade it from a Strong Buy to a Buy rating. There is little upside left and it certainly isn't the most opportunistic REIT in our portfolio anymore.

But is this enough of a reason for us to sell the large position in our Core Portfolio?

No, it isn't.

I still think that EPRT's unique business model is likely to deliver above-average returns with below-average risk over the long run, and that's what alpha is all about.

It is unlikely to be our most rewarding position going forward, but we have a high degree of confidence in its ability to consistently deliver strong risk-adjusted returns, and therefore, it remains a great anchor position for our Core Portfolio.

Moreover, let's not forget that if I sold my position, I would also be hit with a large tax bill and wouldn't get to reinvest the entire proceeds into another REIT. Adjusted for that, I am even less likely to sell EPRT.

Here is why I continue to think that EPRT offers potential for above-average returns with below-average risk:

Above Average Returns

The expected returns of REITs are mainly a function of three things:

Their dividend yield.

Their FFO per share growth.

Their potential for repricing upside.

Today, EPRT's dividend yield is 3.8%. That's slightly below average for a REIT, but keep in mind that EPRT retains a substantial portion of its cash flow for growth with a ~65% payout ratio and it also uses relatively little leverage, which all else held equal, results in a lower yield.

What it lacks in its yield, it more than makes up in its growth.

The expected growth of a net lease REIT is the result of three things:

Its lease escalations.

Its retained cash flow.

Its ability to raise additional capital and reinvest it at a positive spread.

The two first components here are what we call "internal growth" and the third component is "external growth", and from both perspectives, EPRT is above average. Its leases are true-triple net, which means that EPRT has zero capex responsibilities, and its 1.7% average rent escalators fall straight to the bottom line. Moreover, it retains ~35% of its cash flow to reinvest in growth, which is very substantial. Add to that a bit of leverage, EPRT should be able to grow internally by about 4% per year.

That's great because this growth is highly consistent and predictable.

But its external growth prospects are equally attractive and this is really the main reason why EPRT's model is so powerful. The REIT is still relatively small in size and it is able to consistently access capital at a relatively low cost and reinvest it at a positive spread, resulting in rapid FFO per share growth.

This is especially true right now as its valuation has recently expanded and it gives access to cheaper equity.

At ~16x FFO, its cost of equity is right around 6%.

Interest rates are today still relatively high, but this is less relevant since EPRT doesn't use much debt anyway and has no debt maturities until 2027. Its LTV is around 30% and its borrowing cost is around 5% right now.

As a result, its weighted average cost of capital is slightly below 6% right now.

Yet, the cap rates of its latest acquisitions are 8% or more.

That's a strong 200 basis point spread.

This means that EPRT can just raise more capital and buy more properties and it will expand its FFO on a per-share basis. Rinse and repeat.

The more it does of it, and the faster it will grow.

The REIT just recently held its Q2 conference call and the management seemed confident that their growth would accelerate in the near term: [emphasis added]

"Things are firing on all cylinders. The pipeline continues to build, and we continue to deploy capital clearly, as we said in the statements...

As we said on the call, our pipeline remains full, and we continue to work hard, which may suggest a robust third quarter here, but it’s kind of too early to really tell, but we feel good about the investment market...

I clearly think as we get closer to 2025 and we get 2025 guidance out there, there's upside to our shares. So we will continue to be opportunistic on the equity side."

With a 3.8% dividend yield and ~4% internal growth, all EPRT needs to achieve is ~2% of external growth to reach double-digit total returns.

I think that this is doable for them. Historically, they have done quite a bit better, often reaching closer to 4% of annual external growth.

Therefore, the expected return calculation for EPRT would be:

3.8% dividend yield + 4% internal growth + 2-4% of external growth = 9.8% - 11.8% if you buy shares today.

That's very attractive coming from a defensive REIT.

And it does not end there.

We haven't yet discussed the potential for upside from repricing. Admittedly, I would not expect much from this. The shares already trade at 16x FFO even as interest rates are still relatively high.

But the debt market is now pricing high odds of up to 150-200 basis points lower interest rates by the end of 2025 and I think that this would likely cause EPRT's valuation to expand a bit further.

It will push a lot more capital towards REITs and EPRT being part of numerous indexes would be positively impacted by this. Moreover, it would also result in an even lower cost of capital, potentially accelerating its growth rate even further.

Repricing at 17x FFO would result in 6% upside.

Repricing t 18x FFO would result in 12% upside.

And importantly, this upside could be realized in the short run as interest rates are cut. Net lease REITs are the closest things to bonds in the equity markets and therefore, their valuations tend to react the fastest to cuts in interest rates. This explains why the shares have been surging lately and with interest rate cuts just now about to start, it seems reasonable to expect a bit more upside.

Adding that to the return equation, we get the following:

3.8% dividend yield + 4% internal growth + 2-4% of external growth + 6-12 = 15.8% - 23.8% if you buy shares today.

If that was the return prospects of speculative REIT with highly uncertain prospects, I wouldn't be interested. But EPRT is the opposite of that. It is a very defensive REIT with highly predictable prospects. We discuss that next:

Below Average Risks

EPRT is a net lease REIT that focuses on properties leased to middle-market tenants. On the surface, this may sound like a riskier strategy. Your tenants are smaller in size and their credit quality is often subpar.

But what EPRT lacks in tenant quality, it makes up in its contract quality.

These tenants have a lot less bargaining power with their landlords and this allows EPRT to structure landlord-friendly leases with:

Access to unit-level profitability

Strong rent coverage

Long lease terms

No landlord responsibilities

Master lease protection

Corporate guarantees

The access to unit-level profitability is especially important. The big-name tenants typically don't grant this to their landlords, and this then means that they are left in the dark. You never truly know how well the property is doing and you are just relying on the credit quality of your tenant.

EPRT takes the opposite approach because the unit-level profitability of the asset is what ultimately matters. Even if the tenant had poor credit and was suffering losses at other properties, it is unlikely to ever default on the lease of its profitable properties.

EPRT's performance during the pandemic is the best proof of that. This was the worst possible crisis for the company and yet, it managed to keep growing its cash flow and dividend. Some tenants had to make late rent payments because they temporarily couldn't operate their properties, but the point is that they didn't vacate their properties and they still ended up paying their rent.

Today, the average rent coverage is 3.9x so there is still significant margin of safety. If we hit a recession in the future, this ratio may come down a bit, but its tenants should still manage to remain profitable. This is especially true given that EPRT focuses more on defensive service-oriented properties such as car washes, early childhood education centers, and dental clinics:

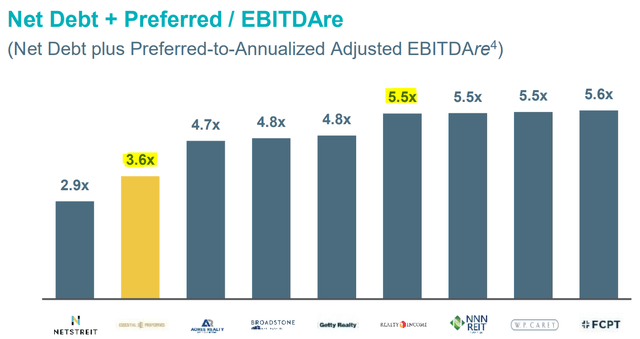

Finally, EPRT has one of the strongest balance sheets in the entire REIT sector with a low 30% LTV and a 3.6x Debt-to-EBITDA. In fact, its leverage is one of the lowest in the net lease, even lower than that of A-rated REITs like Realty Income (O):

EPRT also pairs this low leverage with a sector-low payout ratio of 65%, leaving the REIT significant financial flexibility to organically pay off debt maturities if needed.

Finally, the management has one of the best track records of the entire REIT sector and they are cycle-tested.

The combination of a defensive business model, low leverage, and an exceptional management team results in a lower risk profile.

Closing Note

I don't plan to sell my shares. At most, I would sell some of it to reinvest in other REITs if I felt like there was really no upside left, but as of right now, I am happy to keep holding to the large position in our Core Portfolio because I think that it will continue to deliver above-average returns with below-average risk.

It won't be our most rewarding REIT in the future, but it will be one of our consistent outperformers.

In hindsight, I have always almost regretted selling winners and I don't want to make this mistake again with this one, especially knowing that the thesis remains strong and I would suffer a big tax impact.

Finally, please note that this is a free article from High Yield Landlord. If you found it valuable, consider joining our service for a 2-week free trial. You'll gain immediate access to my entire REIT portfolio, real-time trade alerts, exclusive REIT CEO interviews, and much more. We are the largest and highest-rated REIT investment newsletter online, with over 2,000 paid members and more than 500 five-star reviews.

We spend 1000s of hours and over $100,000 per year researching the market for the most profitable investment opportunities and share the results with you at a tiny fraction of the cost.

Get started today - the first 2 weeks are on us:

Analyst's Disclosure: I/we have a beneficial long position in the shares of all companies held in the CORE PORTFOLIO, RETIREMENT PORTFOLIO, and INTERNATIONAL PORTFOLIO either through stock ownership, options, or other derivatives. High Yield Landlord® ('HYL') is managed by Leonberg Research, a subsidiary of Leonberg Capital. All rights are reserved. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The newsletter is impersonal and subscribers/readers should not make any investment decision without conducting their own due diligence, and consulting their financial advisor about their specific situation. The information is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The opinions expressed are those of the publisher and are subject to change without notice. We are a team of five analysts, each contributing distinct perspectives. Nonetheless, Jussi Askola, the leader of the service, is responsible for making the final investment decisions and overseeing the portfolio. We do not always agree with each other and an investment by Jussi should not be taken as an endorsement by other authors. Past performance is no guarantee of future results. Our portfolio performance data is provided by Interactive Brokers and believed to be accurate but its accuracy has not been audited and cannot be guaranteed. Our portfolio may not be perfectly comparable to the relevant index. It is more concentrated and may at times use margin and/or invest in companies that are not typically included in REIT indexes. Finally, High Yield Landlord is not a licensed securities dealer, broker, US investment adviser, or investment bank. We simply share research on the REIT sector.