Final Takeaways From REIT Week Conference

I recently attended REIT Week in NYC, which is the biggest annual REIT conference in the world.

The conference brings together the management teams of most major REITs and gives investors the opportunity to participate in roundtable discussions, ask questions, take notes, and better understand how these companies are navigating today’s market environment.

I already shared my company-specific takeaways in a separate series of articles. In this article, I want to take a step back and focus on the broader conclusions that I took away from the conference.

These broader takeaways are important because they help explain why REITs have started to recover, why sentiment is improving, and why I believe that the opportunity remains attractive.

Oversupply

The single most important takeaway from the conference was that the oversupply headwind is finally approaching an end.

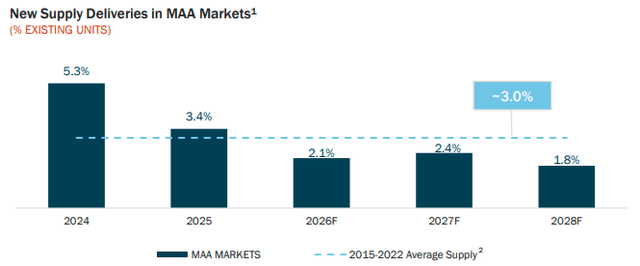

Following the pandemic, interest rates were exceptionally low, capital was abundant, and property values were high. This led to a major wave of new development across apartments, self-storage, industrial, life science, and other property sectors.

Because real estate development takes years, many projects that were started in 2021, 2022, and 2023 are only now hitting the market in 2024, 2025, and 2026. This has pressured occupancy rates, slowed rent growth, increased concessions, and hurt same-property NOI growth in several sectors.

In my opinion, this has been an even bigger headwind than interest rates for many REITs. Interest rates hurt market sentiment, but oversupply hurts property-level fundamentals.

The good news is that new construction starts have now collapsed in most sectors. Higher interest rates, higher construction costs, and lower property values mean that most new projects simply do not pencil out anymore.

Developers will not build if they cannot earn a profit.

As a result, supply should decline meaningfully in 2027 and remain low for several years thereafter. This matters because real estate supply is visible far in advance. If starts are low today, deliveries will also be low a few years from now.

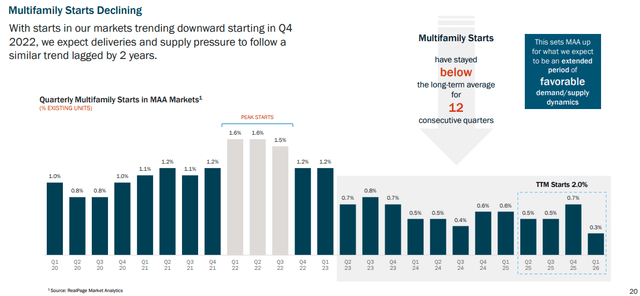

This is especially important for apartments. I heard directly from the CEO of Mid-America Apartment Communities (MAA), the largest Sunbelt apartment REIT, and the tone was bullish for the coming years. The same was true for BSR REIT and others.

The Sunbelt apartment market has been pressured by elevated supply, but that supply is now being absorbed, new starts have collapsed, and demand remains healthy. This sets the stage for a strong acceleration in rent growth as we get closer to 2027.

The key point is simple: the biggest headwind for many REITs is fading. If oversupply was the main reason why fundamentals disappointed in recent years, then the end of oversupply should be a major catalyst for stronger growth in the coming years.

Interest Rates

Interest rates were another major topic at the conference.

Right now, the market is worried that the war in Iran could lead to higher inflation and, therefore, higher interest rates. Energy prices have risen, inflation expectations have increased, and long-term interest rates have moved higher.

But the main takeaway from the macro panel at REIT Week was that this surge in rates should likely prove temporary.

This is also our view.

The recent inflationary pressure is largely tied to an external shock. War can disrupt supply chains, push energy prices higher, and create near-term inflation, but these effects are typically not permanent.

Higher energy prices eventually lead to more drilling, more supply, and changes in consumption patterns. Wars also do not last forever, and this one appears politically unpopular, increasing the odds that solutions will eventually be found.

More importantly, the broader inflation picture appears much better than the market fears. The post-pandemic inflation surge has largely normalized, the economy is relatively weak, and AI could become a powerful deflationary force over time.

AI can reduce labor costs, automate tasks, improve logistics, lower customer service costs, and increase competition across many sectors. All of this should put downward pressure on inflation.

This does not mean that rates will collapse overnight. The path will likely remain volatile. But the longer-term direction still appears to be lower, not higher, according to the macro experts.

That matters a lot for REITs. Lower rates would reduce borrowing costs, improve acquisition spreads, increase property values, and make REIT dividend yields more attractive relative to bonds.

If lower rates coincide with improving fundamentals as oversupply fades, REITs could benefit from both, much faster growth and expanding valuation multiples.

AI

AI was one of the most discussed topics at the conference, and not just because of data centers. The broader theme was the AI immunity trade.

We started discussing this over a year ago, before it became mainstream. Our thesis was that AI would disrupt many businesses by breaking down barriers to entry, increasing competition, reducing pricing power, and compressing profit margins.

As investors become more concerned about AI disruption, they will increasingly look for sectors that are more resilient. Real estate is one of the most obvious beneficiaries.

People will still need housing. Companies will still need warehouses. Consumers will still need grocery-anchored shopping centers. Society will still need healthcare facilities, cell towers, farmland, timberland, and other essential real assets.

AI can change how these assets are managed, but it is unlikely to make them obsolete. This is why REITs are increasingly being viewed as AI-resilient assets.

This is the reason why REITs have performed well this year despite higher rates. More investors appear to be rotating toward sectors that are less exposed to AI disruption.

But the AI story is not only about immunity. Several property sectors could also directly benefit from AI.

Apartments and self-storage are highly management-intensive. AI can help with leasing, virtual tours, pricing, customer service, maintenance scheduling, renovation decisions, and expense control. This could improve same-property NOI growth over time.

Industrial real estate could also benefit if AI accelerates e-commerce. Prologis (PLD) discussed this point directly. AI can make online marketing more personalized, lower customer service costs, improve logistics, and make it easier for entrepreneurs to launch e-commerce businesses. More e-commerce means more demand for industrial space.

Timberland could also benefit from better productivity tools for more efficient harvesting and land conversions to energy-related uses.

The key point is that AI is not necessarily a threat to REITs. In many cases, it may be a major tailwind. In a world where many businesses face growing disruption risk, essential real assets may become increasingly valuable.

M&A

Another major takeaway was the sharp increase in M&A activity. We have already benefited from several REIT buyouts this year, including Whitestone REIT (WSR), Sila Realty Trust (SILA), National Storage REIT (NSR), and Caesars Entertainment (CZR). Four buyouts in six months are significant, and we expect more to come.

There have also been rumors around other REITs in our portfolio, including Uniti Group (UNIT), SBA Communications (SBAC), and others.

The reason for this increased M&A activity is simple: sophisticated buyers can see that the window of opportunity may not remain open for much longer.

Many REITs still trade at steep discounts to the private market value of their assets. At the same time, the oversupply headwind is likely approaching an end, rent growth should improve, and the long-term direction of interest rates is likely lower.

That is a compelling setup for private equity firms and larger REITs.

This was also reflected in conference attendance. It was noticeably harder this year to get meetings with management teams than it was in 2024 or 2025. There were simply more investors participating.

The opportunity is no longer completely ignored, but valuations remain attractive. This is why buyers are acting now, before the recovery becomes obvious to everyone.

Data Centers

I also discussed data centers with several investors and REIT CEOs, and the tone I heard was often more cautious than expected.

This may surprise some investors because data centers are one of the hottest property sectors in the market today. Demand is strong, AI is driving growth, and tenants include some of the strongest companies in the world.

But the concern is the terminal value.

One prominent REIT CEO asked what the odds are that today’s data centers will look the same as data centers 20 years from now. His answer was essentially 0%.

That is the key risk. Huge amounts of capital are being invested in this space, and with that will likely come major innovation. Power needs, cooling systems, chip architecture, location requirements, and building designs could all change dramatically.

If that happens, some of today’s data centers may face obsolescence risk.

Developers can earn attractive yields today by signing long leases with high-credit tenants. But what is the building worth at the end of the lease? That is much harder to answer.

The market is currently focused almost entirely on near-term growth. Very few investors appear to be thinking deeply about terminal value.

This is why we have been cautious on data center REITs. We are not saying that data centers are bad investments in all cases, but we think the sector is more speculative than many investors appreciate.

That is also why we have preferred to get exposure more indirectly, through an asset manager with permanent capital that earns fees from managing these investments, rather than owning the assets directly.

Europe

The final takeaway is that Europe is becoming more interesting.

A growing number of investors and REITs appear to be looking at Europe because investment spreads are often more attractive. Interest rates are lower than in the US, yet cap rates in many sectors are not necessarily much lower. This can create better investment spreads.

European-listed real estate has also significantly lagged US REITs this year. While American REITs have rallied, many European REITs have missed out on the recovery and, in some cases, sold off further.

Part of this is tied to the war in Iran and its potential energy consequences for Europe. The market is worried that higher energy prices could lead to more inflation and delay rate cuts.

But in my opinion, the market is being too short-term oriented. European REITs often trade at much deeper discounts to NAV than their US peers. Interest rates are lower, balance sheets have improved, and new supply is more limited, resulting in more consistent rent growth.

This is creating interesting opportunities. We expect to discuss a few new European REITs in the near term, and some may eventually make their way into our portfolio.

Bottom Line

The main takeaway from REIT Week is that the setup for REITs is improving.

The oversupply headwind is fading. Interest rates remain volatile, but the longer-term direction is likely lower. AI is increasing the demand for resilient real assets. M&A activity is accelerating. Data centers may be riskier than the market appreciates. And Europe is becoming more interesting as discounts remain large.

This does not mean that every REIT is attractive. We still need to be selective and focus on balance sheet strength, management quality, asset quality, and valuation.

But the broader cycle appears to be turning in favor of REITs. The past few years were painful because REITs faced the double headwind of higher interest rates and oversupply.

Now, oversupply is fading, and we expect interest rates to eventually follow.

That creates the potential for a much better environment in the coming years. This is why we remain bullish and continue to believe that REITs offer some of the best risk-to-reward opportunities in today’s market, especially given their low valuations and the increased M&A activity.

Finally, please note that we have exceptionally posted this article without a paywall. If you found it valuable, consider joining High Yield Landlord for a 2-week free trial.

We expect to share a Trade Alert with our paid members tomorrow, and by starting your free trial today, you will also gain access to it. You will also get immediate access to my entire REIT portfolio, our exclusive REIT CEO interviews, and much more. We are the largest and highest-rated REIT investment newsletter online, with over 2,000 paid members and more than 500 five-star reviews.

We spend thousands of hours and over $100,000 per year researching the market for the most profitable investment opportunities, and we share the results with you at a tiny fraction of the cost.

Get started today - the first 2 weeks are on us:

Analyst’s Disclosure: I/we have a beneficial long position in the shares of all companies held in the CORE PORTFOLIO, RETIREMENT PORTFOLIO, and INTERNATIONAL PORTFOLIO either through stock ownership, options, or other derivatives. We also own a position in FarmTogether. High Yield Landlord® (’HYL’) is managed by Leonberg Research, a subsidiary of Leonberg Capital. All rights are reserved. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The newsletter is impersonal and subscribers/readers should not make any investment decision without conducting their own due diligence, and consulting their financial advisor about their specific situation. The information is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The opinions expressed are those of the publisher and are subject to change without notice. We are a team of five analysts, each contributing distinct perspectives. Nonetheless, Jussi Askola, the leader of the service, is responsible for making the final investment decisions and overseeing the portfolio. We do not always agree with each other, and an investment by Jussi should not be taken as an endorsement by other authors. Past performance is no guarantee of future results. Our portfolio performance data is provided by Interactive Brokers and believed to be accurate but its accuracy has not been audited and cannot be guaranteed. Our portfolio may not be perfectly comparable to the relevant index. It is more concentrated and may at times use margin and/or invest in companies that are not typically included in REIT indexes. Finally, High Yield Landlord is not a licensed securities dealer, broker, US investment adviser, or investment bank. We simply share research on the REIT sector.