Top Pick #5: Vonovia

Please note that this is a free article of High Yield Landlord. If you find it valuable, consider joining our service for a 2-week free trial. You'll gain immediate access to my entire REIT portfolio, real-time trade alerts, exclusive REIT CEO interviews, and much more.

Top Pick #5: Vonovia

Vonovia (VNA / VONOY) is our largest international real estate investment and it is pretty simple to explain why:

Vonovia is a blue-chip company with solid long-term prospects... but it is priced at a 60% discount to its net asset value due to some temporary challenges.

Temporary is the keyword here.

What makes Vonovia a blue chip?

5 reasons:

Defensive portfolio: Vonovia is the largest apartment landlord in Europe. It owns over 550,000 units, mostly in Germany, which is one of Europe's safe havens. These are Class B affordable apartment communities that generate defensive cash flow, regardless of how the economy is doing. This is especially true given how rents are regulated in Germany. The regulation limits rent growth during good years but it also reduces or even eliminates the downside during tough times. To give you an example, rents did not drop even in 2008-2009. Today, rents are regulated too low and are still catching up to the recent inflation. As a result, not enough new housing is being built and vacancy rates are historically low at just 2%. Therefore, we see no threat of declining rents. On the contrary, rent growth is accelerating at the moment.

Strong balance sheet: From a first look, it may seem that Vonovia has a lot of leverage. This is especially true if you compare its balance sheet to that of comparable US REITs. But this would ignore the unique nature of German apartment communities, which generate far safer cash flow. As we noted earlier, their rents are expected to keep growing even through recessions so these assets are more comparable to Inflation-protected treasuries in a way (TIPS in short). Credit rating agencies take this into account and it explains why Vonovia has a BBB+ rated balance sheet with a positive outlook, despite having a high Debt-to-EBITDA. Its LTV is at around 43% and its maturities are also well-staggered with no more than 11% of its debt maturing annually. This should allow Vonovia to pay off maturities with retained cash flow, asset dispositions, and JV structuring, mitigating the impact of rising interest rates. The 3-4% annual rent growth rate also provides an additional buffer to the surge in interest expense.

Competitive advantages: A blue-chip needs to create value beyond what can be captured by holding the assets, and Vonovia does exactly that. Vonovia is the biggest landlord in Europe with a ~€100 billion portfolio and its size gives it many competitive advantages that allow it to create value for shareholders. Firstly, it results in huge economies of scale. The EBITDA margin of its properties is nearly 80% compared to just around 60% for peers. That's a massive difference. Secondly, Vonovia is able to consistently resell properties at large gains by dividing them into condos and reselling them one by one. The upside is typically around 40% of their current reported fair value. Thirdly, it creates value via value-add and development projects. Vonovia is so large that it can afford to have its own construction arm in-house, allowing it to do these projects in a very cost-efficient way. Finally, Vonovia is able to use its scale to offer services to other investors. This includes brokerage, property management, construction services, and asset management in exchange for fees, boosting its profits and the returns of shareholders. If you were simply buying a rental property, you would miss out on all of this.

Predictable growth prospects: Interest expense will rise and this is the main headwind of the company. But because debt maturities are well-staggered and Vonovia is able to pay off most maturities with retained cash flow and asset dispositions, the impact should be well-mitigated. Moreover, Vonovia's rents are expected to rise by 3-4% in 2023 and in the years ahead. The rent hikes apply to 100% of the assets, but the rising interest expense only applies to a limited amount of debt maturities each year.

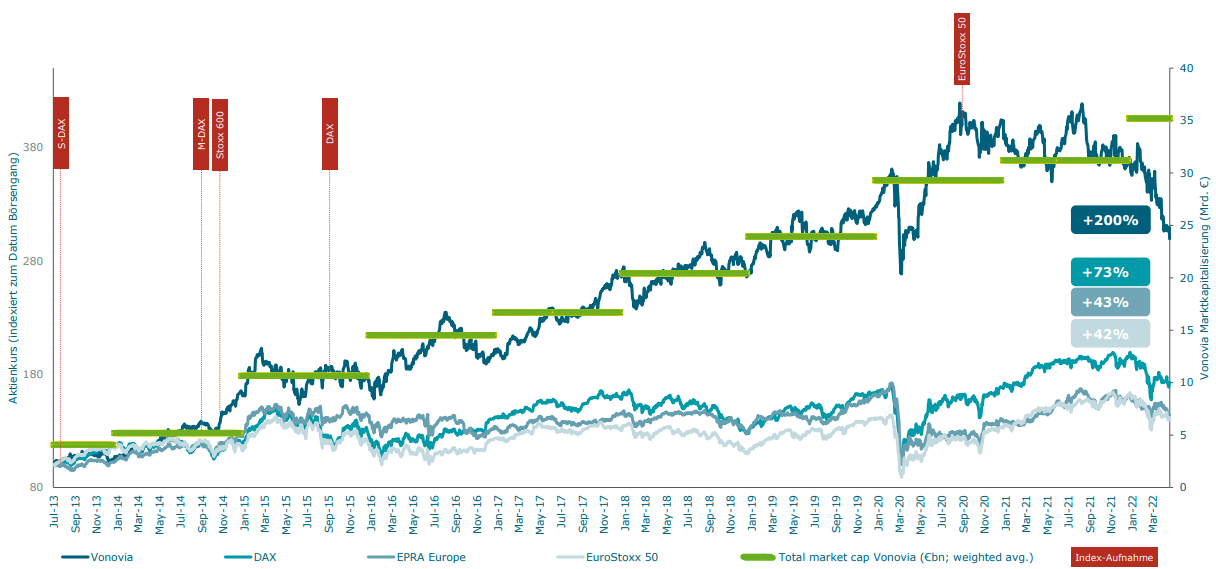

Superior management: Finally, Vonovia's management has an exceptionally strong track record of creating value for shareholders. This may not be reflected in its share price right now, but if you look back at its performance since its IPO, you will find that it has managed to grow its FFO per share by 13% annually from 2013 until 2022 and its NAV per share by even more than that. This resulted in massive market outperformance up until the recent crash:

So Vonovia has all the characteristics of a blue chip and historically, this has also been reflected in its valuation.

On average, it has historically traded at a 10% premium to its net asset value. This is well-deserved given what we explained earlier. You get the benefits of scale, professional management, diversification, liquidity, etc.

But today, the company is priced at a 60% discount to its net asset value. Put differently, you get to buy an interest in its real estate at just around 40 cents on the Euro.

This is near the lowest valuation ever for the company and it is comparable to the valuation of US apartment REITs during the great financial crisis:

Why is it so extraordinarily cheap?

The market worries that the recent surge in interest rates will cause the company's cash flow to decrease substantially and the value of its assets to collapse.

We have previously already explained why its cash flow should be quite resilient. Interest rates surged due to inflation, which leads to higher rents, and its debt maturities are well-staggered.

But will its net asset value collapse?

We think that it is likely to decline a bit, but not by nearly as much as the stock is today priced.

Here are three reasons why its net asset value should be quite resilient:

#1 - Its net asset value represents a steep discount to condo sales

Vonovia has proven time and time again that it is able to resell its apartment communities at a ~40% value uplift after converting them into condos. It does billions of such transactions every year:

Today, Vonovia's reported net asset value appears to be conservatively calculated given that even the low-quality spectrum of condos is a lot more expensive in its markets. The new constructions are commonly sold at more than double or even triple per square meter:

Vonovia is planning to do more of these transactions in the coming years to unlock value, pay off debt and potentially buy back shares.

If needed, it could materially reduce the sale prices to move more products and it still wouldn't hurt its net asset value per share.

#2 - Its net asset value also represents a steep discount to replacement cost

Its reported net asset value is also very significantly below the replacement cost of its properties.

The implied building value based on its NAV is €1,500 per square meter, which is just 40% of the estimated construction cost of its real estate:

In other words, if you had to rebuild the real estate today, you would pay more than 2x Vonovia's current implied building value (based on its net asset value of €50 per share).

Land plus building, the NAV per share of ~€50 represents about €2,400 per square meter, which is very reasonable for good real estate in major German markets. The replacement value is far higher as shown on this graph:

Today, we need a lot more apartments in Germany. Vacancy rates are at just 2% because not enough has been built in recent years.

The reason why so little has been built is that rents are too low to justify the new construction prices. Rents have not risen enough due to how they are regulated.

With that in mind, something will have to give eventually. Either rent will have to rise (and they already are) or the government will need to provide additional incentives for companies like Vonovia to build more to meet the demand.

In any case, it is hard to believe that the value of this real estate could decline a lot since it is absolutely essential, there is significant demand for it, not enough is being built, and it is already priced at a steep discount to replacement cost.

#3 - There remains demand from investors

Today, cap rates are low in Germany at 3-3.5%. This is exceptionally low when you consider that Germany's long-term interest rates have surged from negative to around 2% over the past year.

But despite that, there is still some demand for German apartment communities from major institutional investors and it is pretty simple to understand why.

Today, inflation is still nearly 5% in Germany.

It is nice to now get a 2% interest rate on long-term bonds, but that's not sustainable when inflation is so high. Your real returns are still deeply negative and this is why there is still demand for German apartment communities and other investments, despite the low cap rates.

At least here, you get to better protect your money against the threat of long-term inflation. The near-term returns will be low of course, but rents will rise over time because of how they are regulated and this essential infrastructure cannot be inflated away.

As I noted earlier, these properties are commonly seen as a hybrid between real estate and TIPs in Germany and so this also explains why investors keep buying them.

Besides, there are certain types of institutional investors in Germany that are highly regulated and have few other alternatives. Insurance companies as an example must buy real estate to earn long-term inflation-protected income and meet their long-term obligations. They use little debt anyway because of how they are regulated so the surge in interest rates is not impacting them as much.

These investors also understand that the current interest rate environment is exceptional. Interest rates surged because we had to combat inflation, but as inflation comes back down, interest rates will likely as well. But now, rents will remain at the new higher base, unlocking upside and many investors are betting on that.

Finally, Vonovia is also able to structure JVs with institutional investors, allowing them to benefit from Vonovia's capabilities, and Vonovia can give them a slight discount since it will recoup it from the fees that it will earn for managing these investments.

What are the catalysts?

Today, the share price of the company is around €20, but its net asset value is €50.

This means that even if its net asset value dropped to €40, it would still have 100% upside potential from here.

That's more or less what I expect and I think that there are two main catalysts to get there.

The first catalyst would be the announcement of some property sales or the structuring of new JVs. This would allow the company to pay off some debt maturities and also prove to the market that it is able to unlock value at levels far above what the public market is pricing the company at.

The second and most important catalyst would be a recession. In a weird way, a recession should materially benefit the company because it would kill inflation and likely bring back lower interest rates.

Vonovia's share price would likely rapidly recover to its net asset value because this would essentially remove the one main concern of the market, which is interest rates.

Today, we are already getting strong indications that inflation is headed lower and it wouldn't surprise me if, within a year or two, the European central bank had already cut its interest rates back to materially lower levels.

This should lead to a rapid recovery unlocking ~100% upside and while you wait, you earn a 4% dividend yield. The dividend may not seem high but this is because they retain 2/3 of the cash flow to pay down debt, creating value for shareholders. The real cash flow yield is above 10%, which is exceptional for German apartment communities.

Bottom Line

Vonovia is a blue-chip company and it is only discounted because of the perceived risk of rising interest rates.

I believe that the real risk is smaller than what the market is pricing and as a result, the company has become deeply undervalued.

The management appears to agree as the CEO, CFO, and other insiders have been buying more shares in recent years, and the company also expects to do buybacks - all while paying down debt with retained cash flow and asset dispositions.

To conclude this article, I wanted to share another interesting analysis of Vonovia. It was done by our European analyst, Daviv Ksir, who used to work in private equity and he takes a look at the value of the real estate from the eyes of a real estate developer.

Here's the main highlight of his analysis:

"If you buy Vonovia today, you are essentially buying a 63-square-meter (600 square-foot) apartment in a major German city for EUR56,000 (61,000 USD) or EUR890 per square meter (USD97 per square foot). This is extremely cheap and represents at least 3x-4x the average market level of about EUR3,000 (USD3,300) per square meter.

Let's assume that a newly constructed condo sells for EUR5,000/square meter (USD550/square foot), the developer has a margin of 20%, and construction costs (soft costs plus hard costs) are EUR2,500/square meter (USD270/square foot). So we get an implied land value of about EUR1,500/square meter (see chart below).

This means that for each square meter of residential space that Vonovia holds, the land alone is valued at EUR1,500."

That's why Vonovia is one of our Top 5 Picks...

How to Invest in Vonovia

We invested in Vonovia directly in Germany with the ticker VNA. You can also buy it in the US with tickers VONOY or VNNVF. Note however that the liquidity is much lower in the US and this is why we bought it directly in Germany.

What You Need to Know About Withholding Taxes

There are some tax implications when investing in International companies. Most importantly, a withholding tax may be deducted from the dividends paid by International companies.

This withholding tax is generally 26.375% for German companies, which may seem like a lot, but there are two things to remember here: Firstly, you get a tax credit in your home country to avoid double taxation. And secondly, this is mainly a capital appreciation/growth type investment, and the appreciation is not affected by withholding taxes. Even if there was no dividend, I would invest in Vonovia.

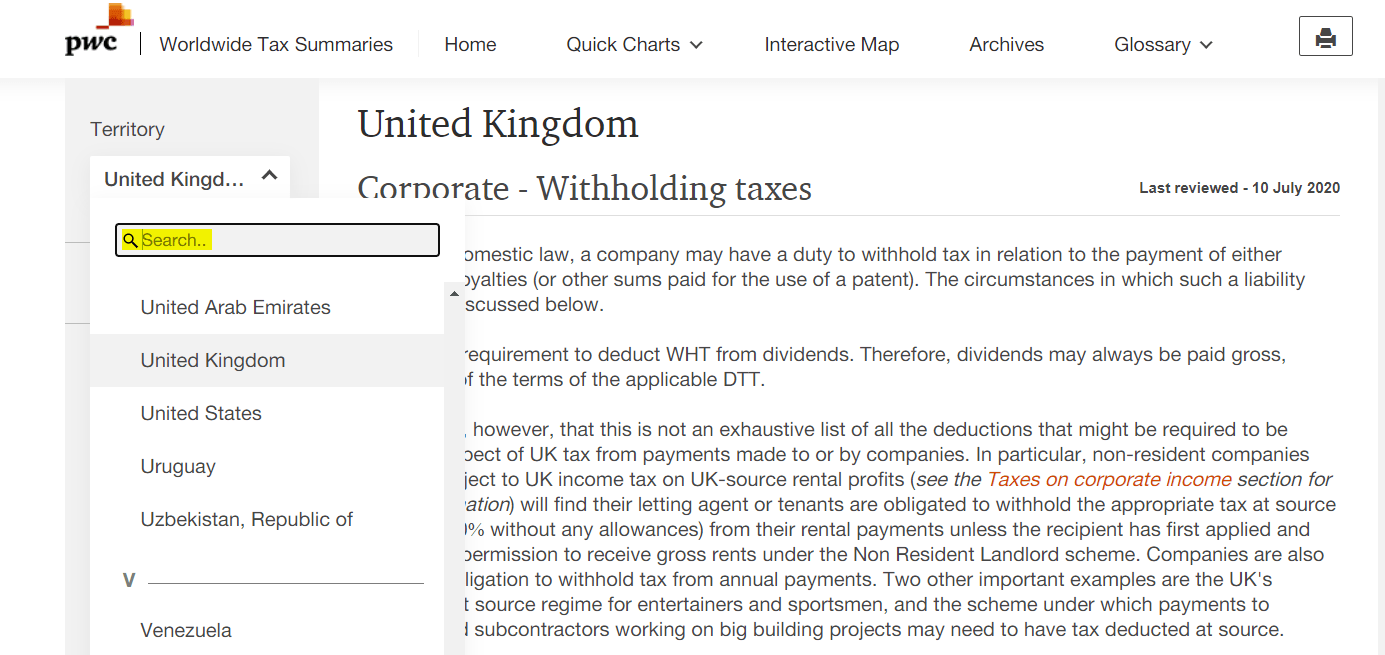

Note that the exact tax rate depends on your country of residency. Investors can find the withholding tax rates for each country on PwC's website. Click the below link to be redirected:

Dividend Withholding Tax Rates

You can use the search bar to change the country and review the different withholding tax rates:

When tax time comes, you will receive in your 1099 from your broker, the amount of foreign taxes withheld, and you use that figure for a credit on your taxes due. In case of doubt, we always recommend contacting your broker and/or a tax advisor. For a detailed overview of Foreign dividend withholding taxes, click here.

Finally, please note that this is a free article from High Yield Landlord. If you found it valuable, consider joining our service for a 2-week free trial. You'll gain immediate access to my entire REIT portfolio, real-time trade alerts, exclusive REIT CEO interviews, and much more. We are the largest and highest-rated REIT investment newsletter online, with over 2,000 paid members and more than 500 five-star reviews.

We spend 1000s of hours and over $100,000 per year researching the market for the most profitable investment opportunities and share the results with you at a tiny fraction of the cost.

Get started today - the first 2 weeks are on us:

Sincerely,

Jussi Askola

Analyst's Disclosure: I/we have a beneficial long position in the shares of all companies held in the CORE PORTFOLIO, RETIREMENT PORTFOLIO, and INTERNATIONAL PORTFOLIO either through stock ownership, options, or other derivatives. High Yield Landlord® ('HYL') is managed by Leonberg Research, a subsidiary of Leonberg Capital. All rights are reserved. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The newsletter is impersonal and subscribers/readers should not make any investment decision without conducting their own due diligence, and consulting their financial advisor about their specific situation. The information is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The opinions expressed are those of the publisher and are subject to change without notice. We are a team of five analysts, each contributing distinct perspectives. Nonetheless, Jussi Askola, the leader of the service, is responsible for making the final investment decisions and overseeing the portfolio. We do not always agree with each other and an investment by Jussi should not be taken as an endorsement by other authors. Past performance is no guarantee of future results. Our portfolio performance data is provided by Interactive Brokers and believed to be accurate but its accuracy has not been audited and cannot be guaranteed. Our portfolio may not be perfectly comparable to the relevant index. It is more concentrated and may at times use margin and/or invest in companies that are not typically included in REIT indexes. Finally, High Yield Landlord is not a licensed securities dealer, broker, US investment adviser, or investment bank. We simply share research on the REIT sector.