TRADE ALERT - Core Portfolio April 2026

Q1 is off to a strong start for us overall.

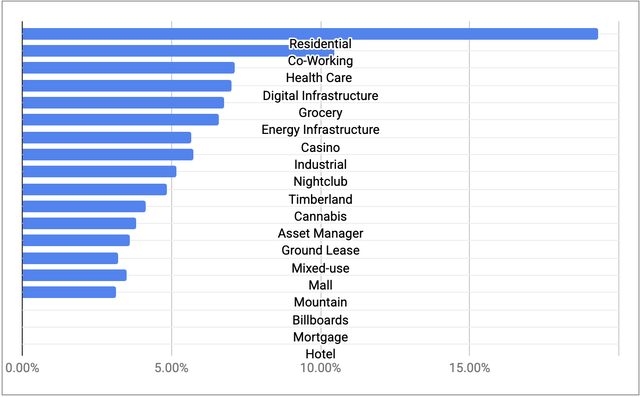

Most notably, residential REITs have surged following stronger-than-expected results, which is especially good news given that residential remains our largest property sector allocation.

We invested heavily in the sector when sentiment was still weak, expecting valuations to recover as fundamentals improved and interest rate fears gradually eased.

However, our biggest loser has remained Alexandria Real Estate (ARE), which continues to disappoint.

It just reported Q1 results, and the stock gave up its recent gains and dropped right back to new 52-week lows.

As a result, we are using this weakness to add another 100 shares to our position, increasing our position size by nearly 10%:

In case you are not familiar with the company, I recommend that you start by reading our latest update by clicking here.

A Short Recap

When we first invested in Alexandria, it was viewed as one of the highest quality REITs in the world, and for good reason.

It owned Class A life science properties, had long leases with steady rent escalations, generated strong same property NOI growth, maintained a BBB+ rated balance sheet with very long debt maturities, and had a long history of dividend growth backed by a conservative payout ratio.

The original thesis was simple.

The company was dealing with temporary oversupply, but its long leases and strong balance sheet were expected to limit the near-term damage. As demand gradually caught up to supply, Alexandria’s cash flow growth would recover, sentiment would improve, and the stock would rerate higher.

That thesis then got hit from two sides.

First, the oversupply issue proved more severe than expected.

Second, and more importantly, the new administration created major disruption across the life science industry through a series of policy actions and threats, including funding cuts, tariff threats, pricing pressure, regulatory chaos, and broader uncertainty.

That caused biotech funding to weaken, the IPO window to shut, and leasing demand for life science space to deteriorate materially.

So what we originally expected to be a 2 to 3 year recovery became more of a 4 to 5 year story.

That was a major negative development. It led to lower cash flow, weaker occupancy, balance sheet pressure, and ultimately a dividend cut.

There is no point pretending otherwise. We got in too early.