TRADE ALERT - Core Portfolio March 2026

Transaction:

We bought the dip in International Workplace Group (IWG /IWGFF), adding another 2,000 shares to our Core Portfolio, increasing our position size by nearly 10%.

----------------------------------------

International Workplace Group (IWG /IWGFF) is our single largest investment, representing 9.6% of our Core Portfolio.

The reason why I invest so heavily in it is that I think it is presenting a generational opportunity to win big over the coming years as the company completes its transformation from a capex-heavy, cyclical, and slow-growing business, into one that’s capital-light, faster-growing, and much more resilient.

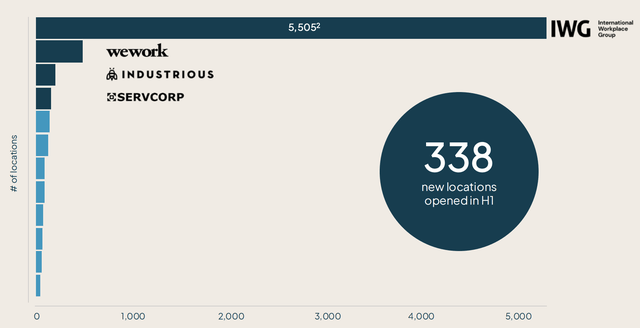

For context, IWG is the world’s leading provider of co-working spaces, operating nearly 6,000 locations under 14 different brands, including Spaces and Regus, in 121 countries. It works with most Fortune 500 companies and has over 8 million users across its entire platform. As such, it is bigger than its next ten biggest rivals combined:

For most of its history, the company used to sign leases for office space and then invest in the space in order to turn it into a co-working location and earn a spread. This was capital-heavy, slow, cyclical, and involved some liability risk as it was committing to those leases.

But then came the pandemic, which flipped the office market upside down.

Office vacancy rates surged to all-time highs of over 20%, even as tenants began to request more flexible office lease terms.

This turned into a massive tailwind for IWG.

Suddenly, office landlords were desperately looking to refill their vacant space, even as tenants were asking for exactly what IWG was providing: office space with flexible terms.

IWG then reinvented its business model into a partnership-based model, partnering with office landlords to simply manage their flexible office space in exchange for a royalty of the revenue. IWG provides the brand, the expertise, the management, the network, the booking system, etc., and the office owner provides the space and the capital.

This transformed IWG into a higher-quality business that’s safer, faster-growing, and worthy of a much higher valuation multiple. It is capital-light, less cyclical (royalty of revenue), has a higher margin, no lease liability risk, and unlocks much faster growth.

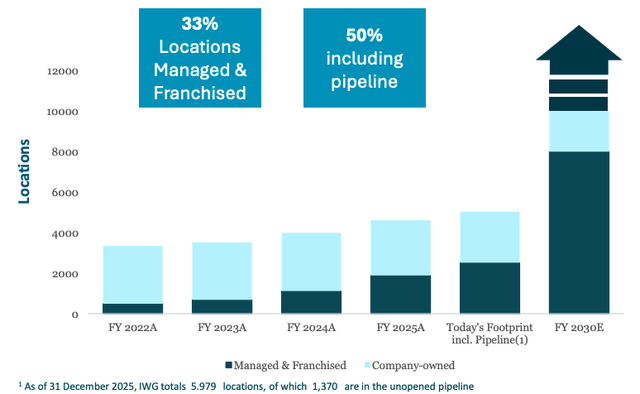

IWG then began to sign 1,000s of new locations annually under this new plan, and this brings us to today.

It took IWG about 30 years to reach 3,000 locations, but only 5 years in the post-pandemic world to double that. Now, the company is already approaching 6,000 (including the signed but not yet opened pipeline), and about 50% of that is under this new capital-light model.

This capital-light business is now scaling really fast, with the management expecting it to reach 80% of its network by 2030.

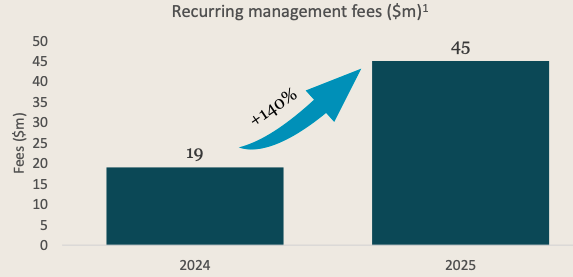

As a result, it is rapidly completing its transformation into a higher-quality business that’s worthy of a higher multiple, even as its cash flow is also exploding to the upside.

Its recurring management fees from this capital-light division surged 140% in 2025, and are expected to nearly double again in 2026, reaching $80 million:

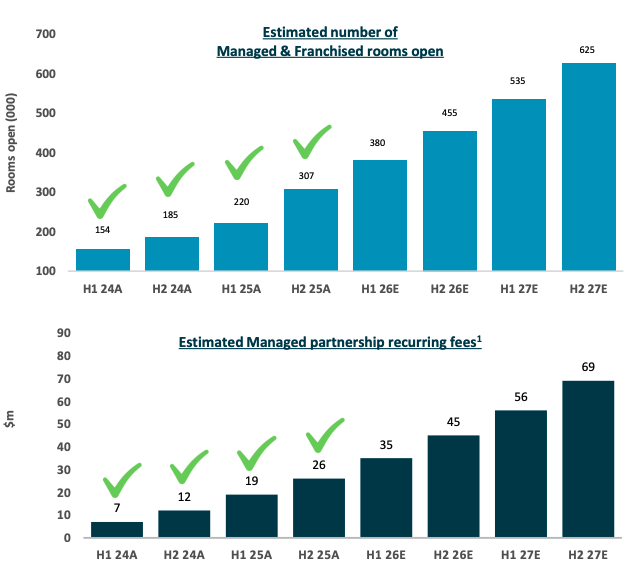

Much of this growth is already contracted, as they have signed about 1,500 locations that are not open yet, and another 1,000 or so that are still in their lease-up phase. Therefore, they feel comfortable sharing guidance even for 2027. The rapid growth is expected to only accelerate:

And here comes the opportunity:

IWG has historically traded at the low valuation multiple of a cyclical, capex-heavy business, operating in the office segment, which has also been out of favor.

However, as its business transforms to that of a rapidly-growing, more resilient, capital-light business, its multiple has the potential to expand very significantly.

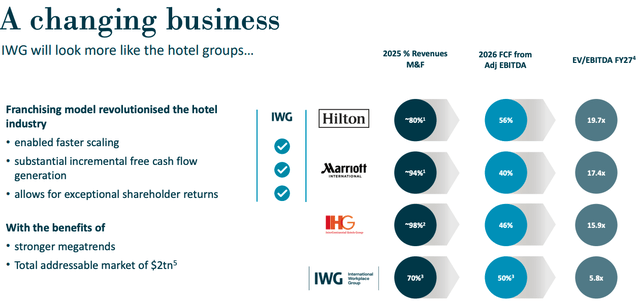

Hotel companies went through a similar transformation over the past decade, and the market rewarded them with huge returns. Here is the case of Marriott (MAR) to give you an example:

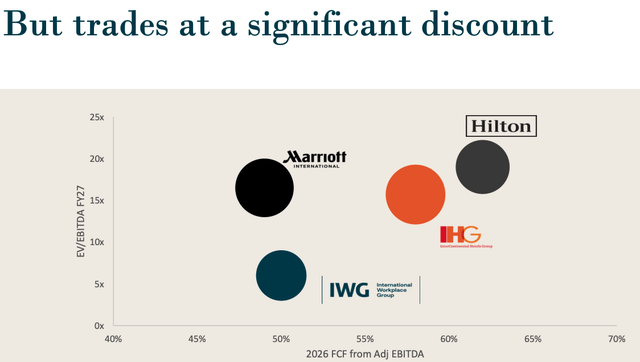

As a result of this transformation, Marriott’s EV/EBITDA based on expected 2027 figures surged to 17.4x. In comparison, IWG is still trading at just about 5x, as it is still in the midst of this transformation:

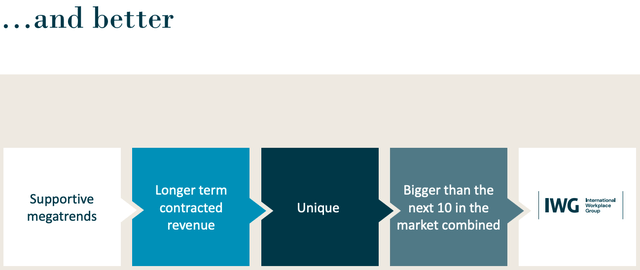

IWG argues that, as it completes a similar transformation, it should eventually reach an even higher multiple than these hotel companies because it enjoys a much clearer leadership positioning, being bigger than its next 10 competitors combined, faces lower competition, and focuses on a market segment with strong megatrends supporting it, longer-term contractual revenues, and lower cyclicality.

Ultimately, it enjoys better long-term growth prospects and faces lower risk and competition:

Yet, it trades at a steep discount:

The market was finally starting to recognize this opportunity in 2025, with its share price nearly doubling in value:

But just recently, lots of stocks sold off due to AI fears, and this brought down most real estate service companies, especially those with office exposure.

CBRE (CBRE) is the world’s biggest company in this space, and its results triggered this sell-off:

But we think that the market is getting it wrong in the case of IWG.

This is not a risk that caught us off-guard. We discussed how AI would impact IWG here at High Yield Landlord already last year.

The market appears to think that it is a headwind for IWG as it could eliminate white-collar jobs.

But that’s far too simplistic and ignores important second-order effects of the AI revolution that will massively benefit IWG’s business.

We think that it will only accelerate the move away from rigid long-term office leases into more flexible office settings, and this could then turn into a huge tailwind for IWG since it is the uncontested leader in this space.

If companies cannot predict how many employees they will need in 1-2 years from now, it becomes too risky to sign a new 10-year-long office lease.

Instead, I expect lots of office tenants to request more flexible office lease terms going forward as a result of this uncertainty. With office vacancy rates already so high, tenants hold the cards, and landlords will need to listen to their demands.

This will push even more office landlords into IWG’s hands, resulting in a lot more signings over the coming years, directly as a result of the AI revolution.

The concept was already growing rapidly in the post-pandemic world as companies moved to hybrid work settings, but it will only accelerate as office landlords face even more vacancies and tenants demand even more flexible terms.

Moreover, as white-collar jobs get eliminated, and lots of ambitious and smart people struggle to find new jobs, I would expect a boom in new small business formations, as AI is also making it easier than ever before to start almost any type of business.

These new small businesses will not sign traditional 10-year leases. Instead, they will use a flexible co-working space for their 1-5 employees. So even the labor force disruption itself could end up resulting in a lot more demand for IWG’s assets over time.

IWG’s team understands this, which is why they recently sacrificed some short-term profitability in order to significantly expand their sales team to accelerate the pace of signing new locations, and this is now starting to pay off. They have noted that they expect new signings to rise closer to 2,000 per year, post-2026. That’s huge given that they currently have only about 4,500 open locations (nearly 6,000 including signed but not yet open).