TRADE ALERT - Retirement Portfolio July 2026

Most REIT sectors are now up significantly in 2026.

The average REIT rose by roughly 11% over the last quarter alone, and this recovery has been broadening as investors begin to recognize that REITs remain heavily discounted, while fundamentals are improving across many property sectors.

But one REIT sector is still hitting 52-week lows today:

Cell towers.

They are all trading near their 52-week lows, even as most REITs have recovered:

We recently bought more shares of SBA Communications (SBAC), which remains our top pick for investors seeking to maximize total returns in the tower space.

Today, we are also buying 63 more shares of Crown Castle (CCI), which is our top pick for income-oriented investors in this sector.

CCI recently traded around $76 per share, well below its 52-week high of $115.76, and at today’s price, CCI offers a roughly 5.5% dividend yield.

We think the market is overly focused on near-term headwinds and underappreciating the long-term opportunity.

Below, we discuss the recent dip, the temporary issues weighing on the stock, and why we believe this is an attractive opportunity to buy a higher-quality, cleaner, pure-play U.S. tower REIT at a depressed valuation.

Why Did Cell Tower REITs Dip?

The market appears to believe that the long-term growth prospects of cell tower REITs have meaningfully deteriorated.

We disagree.

There are two likely reasons why investors have turned more negative on the sector.

The first one is temporary.

The second one is not material.

1. The DISH Issue Is Temporary

The most immediate issue is DISH.

DISH defaulted on its payment obligations earlier this year, and Crown Castle responded by terminating the agreement and pursuing recovery of the payments owed under the contract. The company has amended its pending litigation to include a breach-of-contract claim, and management is seeking to recover the remaining payments owed under the original contract.

As I understand it, DISH is arguing that it should be excused from these obligations under force majeure, essentially claiming that regulatory or government-related actions prevented it from performing as originally expected. Crown Castle disputes this. Its position is that DISH had contractual payment obligations, failed to meet them, and that CCI was therefore within its rights to terminate the agreement and pursue recovery.

To be clear, I am not a legal expert, and I do not know whether Crown Castle will ultimately be successful in court. Therefore, I am not underwriting our investment thesis based on a legal recovery. If CCI recovers some of the money, that would be upside, but we are not relying on it.

The more important point is that the DISH issue is quantifiable and temporary.

For 2026, Crown Castle expects $240 million of total headwinds from DISH terminations and Sprint cancellations. Of this, $220 million is related to DISH and $20 million is related to Sprint.

That sounds like a large number, and it is painful in the short term. But it needs to be put into context.

Crown Castle’s 2026 site rental revenue guidance is roughly $3.85 billion at the midpoint. Therefore, the DISH impact represents about 5.7% of annual site rental revenues, and the Sprint impact represents about 0.5%. Combined, these two headwinds represent roughly 6.2% of annual site rental revenues.

So this is not immaterial, but it is also not thesis-breaking.

It is a one-time tenant-specific reset that is making the headline numbers look much worse than the underlying business.

This was already visible in the first quarter. Crown Castle reported that organic growth, excluding Sprint cancellations and DISH terminations, was strong at 3.1%. However, this was more than offset by a $49 million DISH termination impact, $5 million of Sprint cancellations, and a $26 million decline in straight-line revenues and amortization of prepaid rent.

In other words, the reported numbers look weak because a roughly 6% tenant-specific headwind is being recognized all at once.

But underneath that, the core tower business is still growing, and that is the key point.

DISH is painful, but it does not tell us that demand for towers is disappearing. It does not tell us that carriers no longer need CCI’s infrastructure. It does not tell us that the long-term growth story is broken.

It tells us that one tenant defaulted, CCI is disputing the matter in court, and the company is now moving past it.

Once this headwind is lapped, the underlying organic growth rate should become much clearer. Management already expects roughly 3.3% organic contribution to site rental billings in 2026, when excluding DISH terminations and Sprint cancellations.

That is why we view the current weakness as temporary. It is a one-time revenue reset from a specific tenant issue, which may or may not be recovered in court, layered on top of a tower business that continues to grow organically.

This is masking the quality of the business today, and that is helping create the opportunity.

2. Satellite Fears Are Overstated

The second concern is the reemergence of satellite-related fears, especially with renewed attention around SpaceX (SPCX) following its IPO.

We think this fear is being overstated.

Starlink is a real business and worth monitoring, but it is not a serious replacement threat to tower infrastructure in cities and suburbs.

Satellite connectivity is best suited for rural areas, dead zones, emergency connectivity, and backup coverage. It is not a substitute for terrestrial wireless networks in dense population centers.

The reason is simple physics.

Towers are far closer to users. They can handle far more data density, with lower latency and lower cost per gigabyte. A satellite must serve an enormous geographic area from far away, which sharply limits how much traffic it can handle simultaneously.

This is why satellite connectivity can be useful in places where tower infrastructure does not exist, but it is not well suited to replace towers where most mobile data traffic actually occurs.

This point is especially important as data consumption continues to grow.

The more data people consume, the more important terrestrial networks become.

Satellite may help fill the gaps, but towers remain the core infrastructure for modern wireless networks.

Even on Crown Castle’s own earnings call, management indicated that carrier densification behavior has not materially changed and that the satellite impact is currently “de minimis.”

We agree. The market is treating satellite as a major obsolescence threat, but the actual impact on tower demand appears minimal.

Crown Castle Is Now A Much Cleaner Business

Crown Castle has gone through a major transformation.

The company sold its fiber and small cell businesses, which had long been a source of investor frustration. Those businesses required heavy capital investment, failed to produce the returns originally expected, and contributed to higher leverage and put pressure on the dividend.

The sale was unpopular in the short term because it reduced cash flow and forced the company to reset its dividend.

But we think it was the right long-term decision.

Crown Castle is now a much cleaner business. It has become the only large, publicly traded, U.S.-focused pure-play tower company. American Tower (AMT) and SBA Communications (SBAC) also own high-quality tower portfolios, but both have exposure to international markets, which brings additional currency, political, and regulatory risks. Crown Castle is now focused on the U.S., which remains one of the most attractive wireless infrastructure markets in the world.

The company completed the sale of its fiber and small cell businesses for $8.5 billion, and management expects to use the proceeds to repay approximately $7 billion of debt and repurchase approximately $1 billion of shares.

This transaction simplifies the business, improves the balance sheet, reduces capital intensity, and allows management to focus entirely on making Crown Castle a best-in-class tower REIT.

Management has also executed a restructuring of its tower and corporate organizations, which is expected to reduce annualized run-rate costs by $65 million.

Again, these are near-term disruptions that should improve the long-term quality of the company.

The market is punishing Crown Castle for the messy transition, but we think investors should look beyond it.

Growth Should Reaccelerate

The biggest question is not whether Crown Castle will grow again.

The bigger question is when that growth will show up in the numbers.

Today, growth is being masked by DISH, Sprint churn, rising interest expense, and the transformation of the business. But once these headwinds are absorbed, the underlying tower business should return to growth.

Management believes that the current 3.5% organic growth, which is already strong, should represent the low point.

Carrier activity has paused after the initial 5G buildout, but the long-term demand drivers remain intact:

mobile data consumption continues to grow,

fixed wireless access is gaining adoption,

new spectrum deployments will eventually require more equipment,

AI applications should increase data usage,

and 6G will create another future investment cycle.

The market seems to assume that tower growth is permanently impaired, but we think that is wrong. Wireless data usage has grown for decades, and every major new technology cycle has ultimately required more equipment, more densification, and more tower infrastructure.

AI could make this even more important.

AI applications are likely to require far more data movement, including more uploading of photos, videos, and real-time information. This matters because mobile networks were historically more download-heavy, but many future AI applications may require far more two-way data traffic.

Autonomous vehicles, robotics, smart infrastructure, AI assistants, augmented reality, and real-time video-based AI tools could all increase the need for faster, denser, more reliable wireless networks.

More data consumption ultimately means more demand for infrastructure, and cell towers sit at the center of that infrastructure.

This is why we believe the long-term growth prospects remain compelling, even if the exact timing is difficult to predict.

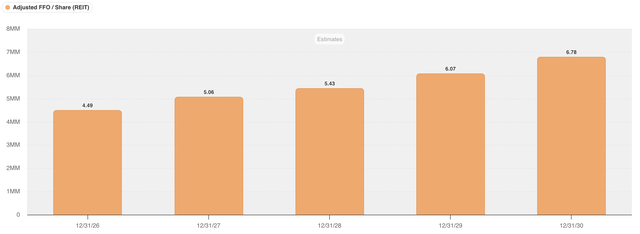

The consensus of analysts also appears to expect a meaningful rebound in growth, which you can see below. They expect 10%+ annual AFFO per share growth through 2030 once we move past the impact of lease cancellations:

I am not so sure about the exact timing of when growth will accelerate, but I don’t think that it is a question of if but when.

Edge Computing Adds Optionality

Longer term, Crown Castle may also benefit from the rise of edge computing.

Edge computing means moving computing power closer to the end user, rather than relying entirely on large centralized cloud data centers that may be located hundreds or thousands of miles away.

This matters because many next-generation applications will require extremely fast response times.

AI inference, autonomous vehicles, robotics, smart factories, augmented reality, virtual reality, and other real-time applications cannot always afford the latency that comes from sending data back and forth to a distant cloud facility.

This is where Crown Castle’s existing tower portfolio could become more valuable.

CCI already owns a large network of tower sites that are often located close to population centers, traffic corridors, and other areas where data is created and consumed. Many of these sites already have key infrastructure in place, including power, fiber backhaul, secure physical locations, and available ground space.

That makes them potentially attractive locations for small edge-computing facilities, where data can be processed locally before being sent back to the broader cloud network.

In other words, Crown Castle may eventually be able to monetize its tower sites in a new way that could create significant new cash flow.

Historically, the value of a tower site has primarily come from leasing vertical space on the tower to wireless carriers. But edge computing could create an opportunity to also monetize the horizontal space at the base of the tower by hosting small data-processing equipment, servers, batteries, cooling systems, or other infrastructure needed to support low-latency applications.

This could be especially valuable because Crown Castle would not need to create an entirely new platform from scratch.

It already owns the physical locations.

It already has relationships with wireless carriers.

And many of its sites already have the basic infrastructure needed to support additional use cases.

To be clear, this opportunity is still early and should not be viewed as a major near-term earnings driver.

It is growing fast, but Crown Castle is still in the trial phase, and it remains uncertain how quickly edge computing will scale and how much economic value tower owners will ultimately capture.

But the optionality is meaningful.

If AI adoption continues to accelerate and more data needs to be processed closer to the end user, tower sites could become increasingly important local infrastructure hubs. In that scenario, Crown Castle would benefit not only from continued demand for wireless connectivity, but also from the growing need for distributed computing infrastructure across the country.