Updates On Our Canadian Top Picks

Something unique about High Yield Landlord is that we do not limit our coverage to U.S. REITs, but also actively research opportunities across global markets.

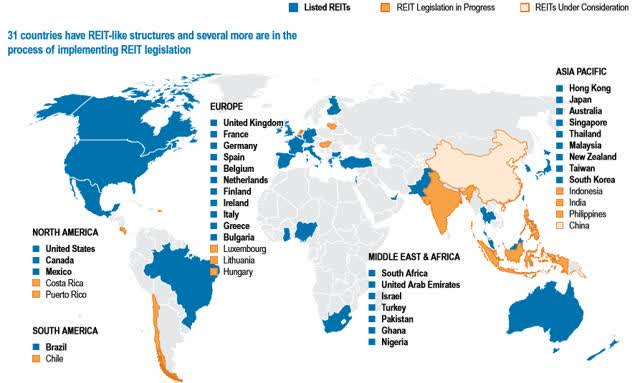

Today, more than 30 countries have adopted REIT-like regimes, creating a broad and diverse opportunity set for investors:

Our International Portfolio is optional and designed for those seeking greater diversification to achieve better risk-adjusted returns.

Personally, I target allocating at least 25% of my REIT exposure to non-U.S. markets. Some members may choose to allocate more, while others may prefer to remain focused on domestic opportunities. Ultimately, it depends on individual preferences, risk tolerance, and return objectives.

The aim is to equip you with the tools and insights needed to go beyond the U.S. market, enabling you to identify and evaluate opportunities across Canada, Europe, South America, Asia, and even Africa, all from the comfort of your home.

The portfolio currently includes 18 positions, with 8 in Europe, 6 in Canada, 3 in Central and Latin America, and 1 in Africa.

In today’s article, we give updates on our 6 Canadian Top Picks:

Northview Residential REIT (NRR.UN:CA)

We invested in Northview Residential REIT (NRR.UN:CA) about two years ago, and it has already become a very successful investment:

And yet, it still remains cheap.

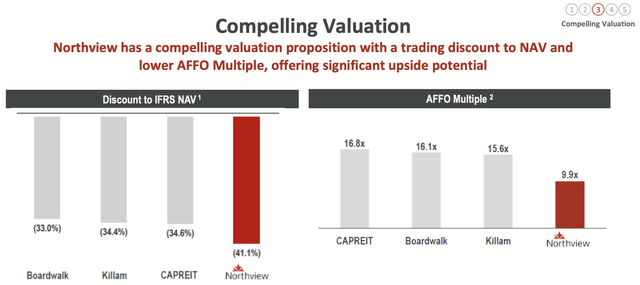

The Canadian apartment REIT continues to trade at a significant discount to its net asset value and at one of the lowest FFO multiples in its peer group, despite delivering some of the strongest growth in the sector.

Recent results once again highlight the strength of the story.

In 2025, FFO per unit grew by 31.7% to $2.37. Even when excluding insurance proceeds, which inflated results, the underlying FFO per unit still grew by 14.9%, which is one of the best growth rates in its peer group.

At the same time, the FFO payout ratio improved materially, dropping by 830 basis points to just 56.6%, providing a much stronger margin of safety for the dividend.

Operational performance also remained solid.

Same-property NOI grew by 4.2%, driven by strong rental growth across the portfolio. Average monthly rents rose by 6.2%, even as occupancy remained stable at a high 95.4%.

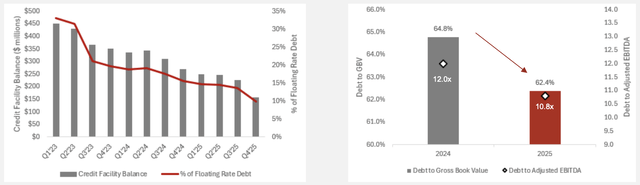

At the same time, management has made significant progress on non-core asset sales and deleveraging.

The company exceeded its non-core asset sale target, completing $164 million of dispositions. The proceeds were largely used to reduce debt, including a $122.7 million reduction in its credit facility, contributing to a 240 basis point improvement in leverage.

Importantly, these asset sales also validate the company’s valuation.

Non-core assets were sold at prices exceeding their IFRS carrying values, despite being among the weaker parts of the portfolio. This suggests that the reported NAV is conservative and likely understates the true value of the underlying real estate.

Interest expense declined by $12.5 million, driven by lower debt balances, improved financing terms, and a more favorable interest rate environment. This was a key driver of the strong FFO growth in 2025.

Putting it all together, the company is executing exactly as planned. It is growing its cash flow, improving its balance sheet, and recycling capital into higher-quality assets, all while maintaining one of the highest dividend yields in the Canadian residential sector.

The key concern remains leverage.

At around 62% loan-to-value, the REIT still carries more debt than most of its peers. However, this figure is somewhat misleading.

Northview values its assets using a relatively high cap rate of around 6.5%, reflecting its focus on smaller, less competitive markets. In contrast, many peers focus on major urban markets where cap rates are closer to 4% to 5%, resulting in higher asset values and lower reported LTVs.

When looking at other metrics, such as debt-to-EBITDA, the difference is far less pronounced, with Northview at around 10x, broadly in line with peers. This is still elevated, but manageable, especially given the REIT’s low payout ratio, well-staggered debt maturities, and strong NOI growth.

Importantly, this market positioning is not a weakness, but a strength in today’s environment.

Northview’s focus on secondary and more rural markets has allowed it to avoid much of the oversupply that has recently impacted primary markets. While major cities have seen a wave of new development, smaller markets have remained more supply-constrained, benefiting from strong housing demand and rising affordability pressures.

This is a key reason why the REIT has been able to deliver such strong rent growth and operating performance.

At the same time, net asset value per share is now rising again, yet the stock remains heavily discounted.

It is currently trading at roughly a 35% discount to NAV and 9.9x AFFO, one of the steepest discounts in its peer group. As the company continues to strengthen its balance sheet and complete the sale of non-core, non-residential assets, which still represent about 15% of rental income, we expect this discount to gradually close.

In the meantime, we are paid well to wait with a 6.6% dividend yield that’s well-covered and paid monthly.