Updates On Our Latin American Top Picks

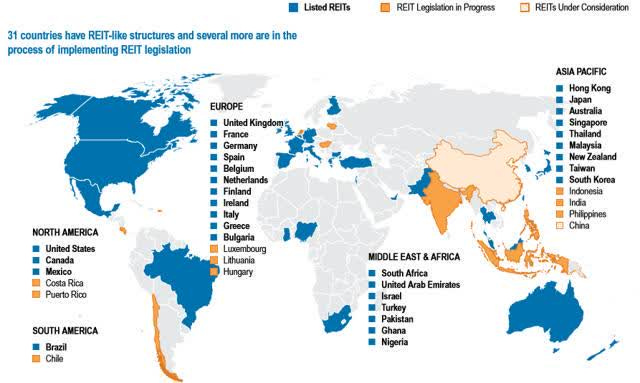

Today, more than 30 countries have adopted REIT-like regimes, creating a broad and diverse opportunity set for investors:

Our International Portfolio is optional and designed for those seeking greater diversification to achieve better risk-adjusted returns.

Personally, I target allocating at least 25% of my REIT exposure to non-U.S. markets. Some members may choose to allocate more, while others may prefer to remain focused on domestic opportunities. Ultimately, it depends on individual preferences, risk tolerance, and return objectives.

The aim is to equip you with the tools and insights needed to go beyond the U.S. market, enabling you to identify and evaluate opportunities across Canada, Europe, South America, Asia, and even Africa, all from the comfort of your home.

The portfolio currently includes 18 positions, with 8 in Europe, 6 in Canada, 3 in Central and Latin America, and 1 in Africa.

In today’s article, we give updates on our Central and Latin American Top Picks

IRSA (IRS):

We first initiated a position in IRSA following Javier Milei’s election victory, expecting that a shift in economic policy and a move away from prior frameworks would attract international capital and drive a rerating of Argentine assets.

This played out as expected, with the stock more than doubling in under a year. We later exited to redeploy our capital, but recently reinitiated a position following a sharp sell-off ahead of the midterm elections, which were driven by fears that the reform agenda would lose momentum and lead to policy gridlock.

Instead, the outcome reduced that risk. The administration strengthened its position in Congress, improving its ability to advance its policy agenda. This was a positive development for markets and removed a key overhang on Argentine equities.

Since then, there has not been much fundamentally new to report, but the outlook remains favorable. Argentina is gradually shifting toward a more market-oriented framework, with efforts to reduce regulation and bureaucracy, improve the business environment, and restore access to capital.

This shift is already having tangible effects. Real estate values are rising, and importantly, mortgage markets are beginning to function again. The lack of financing had long suppressed property values, and as credit availability improves, it should support further upside over time.

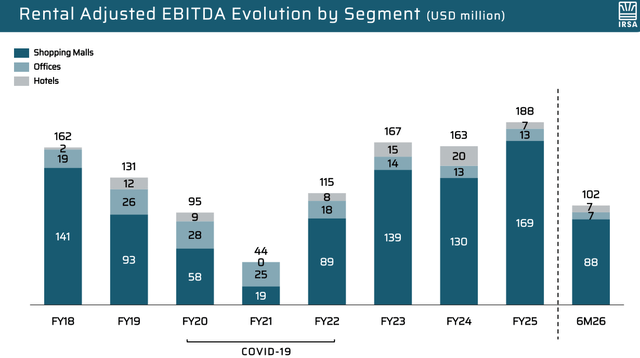

Importantly, IRSA’s underlying business continues to hold up well. Despite political uncertainty and the near-term economic adjustment, including reduced government spending and other austerity measures, the company has delivered resilient cash flow performance in 2025. This reflects the quality of its assets, primarily trophy malls in Buenos Aires with strong locations and high barriers to entry.

The near-term adjustment is meaningful, but it is part of a broader effort to stabilize the economy over the long term.

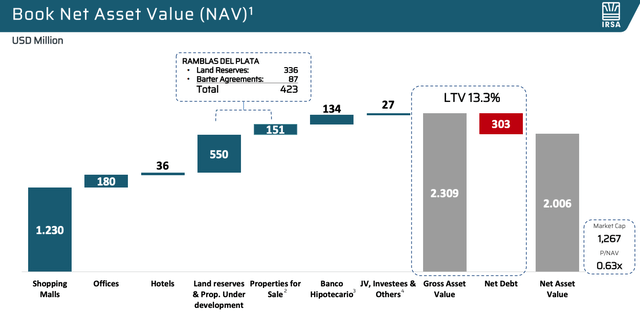

If Argentina continues on its current path and successfully stabilizes its economy, the upside for real estate values could be substantial. IRSA is uniquely positioned to benefit from this, offering exposure to some of the highest-quality real estate in the country while still trading at roughly a 40% discount to net asset value, even though that NAV is conservatively estimated.

In our view, it remains the single best way to gain exposure to Argentine real estate.

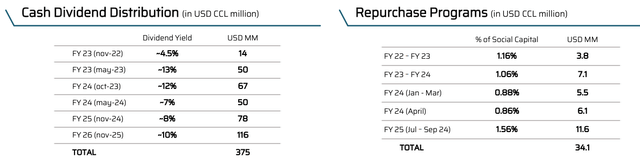

Management also continues to act in a shareholder-friendly manner. They are actively repurchasing shares at a steep discount to NAV, creating significant value for shareholders, and have guided to pay a roughly 10% dividend yield again this year while still retaining capital to buy back shares and fund new investments.

As such, the thesis remains intact. The macro backdrop is improving, the company continues to execute well, and the valuation remains deeply discounted. As Argentina continues to recover and investor confidence returns, we expect IRSA to benefit significantly, both through rising asset values and a narrowing of its discount to NAV.