Interview With Agree Realty Corporation (Buy Rating Reaffirmed)

Last week, I was in Ann Arbor to teach a class on REIT investing at the University of Michigan:

I was fortunate to get this opportunity thanks to Joey Agree, the CEO of Agree Realty Corporation (ADC), who connected me with the University after reading my new book on REIT investing.

By the way, if you have not received your copy of the book yet, you can get it for free by clicking here.

On this same trip, I got to visit their headquarters, where Joey Agree gave me a tour of their offices and spent an hour discussing net lease REITs with me.

This was probably the single most valuable learning experience on net lease investing I have ever had, and this is coming from someone who started his career working for a small private equity firm that specialized in net lease properties.

Here are the main takeaways:

Takeaway #1: Tenant Credit Quality Can Change Over Time, But So Does Tenant Profitability

A lot of net lease REITs like Essential Properties Realty Trust (EPRT) argue that the credit quality of tenants is irrelevant because what ultimately matters is the profitability of the real estate.

If a tenant is profitable at a specific location, it is unlikely to want to vacate, and the lease should survive even in bankruptcy.

Moreover, studies show that the credit quality of tenants is likely to change drastically over the lease term, so paying a premium for better credit is likely not worth it.

Therefore, REITs like EPRT will typically focus on properties occupied by smaller non-rated tenants. This allows them to get a much higher cap rate at the time of acquisition, which translates into larger spreads and faster growth, and they will then mitigate risks by making sure that the property is profitable and will structure a strong lease that results in consistent rental income.

At first glance, this seems to make sense.

But there is a significant catch to this approach, and it is that the property’s profitability is also likely to change over time, based on the quality of the real estate.

The largest and best-rated retailers, like Walmart and McDonald’s, will commonly get the best locations in growing markets with barriers-to-entry to protect themselves from future potential competitors.

However, the net lease properties that are occupied by smaller non-rated companies will commonly be in worse locations, often in secondary or even tertiary markets, with ample land available for future development and few barriers to entry, exposing them to significant risk as future competitors enter their markets.

The tenant may have a 3x rent coverage ratio when the lease is initially signed, but there is often little to stop a competitor from building a similar property across the street, potentially cutting the property’s profitability in half overnight.

Worse yet, if your tenant is a smaller, non-rated, private equity-backed company with poor access to capital, they are then much more likely to default on your lease, leaving you with a vacant property that will be very hard to release unless you cut the rent very drastically to make up for its now lower profitability.

Adding to the risk, many of these properties targeted by REITs like EPRT are not fungible. They are things like car washes, which would be impossible to release to any other type of business, further reducing your recovery potential.

That is why the quality of the real estate and tenant matter much more than what a lot of net lease investors seem to understand. The lease can protect you over the short-to-mid term and give you a false sense of safety, especially if the current rent coverage is high.

But over the long run, the quality of the real estate first, and its tenant second, will determine whether the property remains profitable, which will ultimately also determine whether you will be able to sustainably grow the rent.

So yes, the tenant credit quality is not everything, but the fact is that the best net lease properties in the strongest locations are typically occupied by national investment-grade rated tenants, and this is logical when you think of it.

If you are a property developer and you have a great location and high-quality property, you will always favor a high-quality tenant if you can, given that this will result in a lower cap rate and higher property value.

As a result, these large investment-grade rated tenants will commonly end up with the best real estate, especially since they have the best resources to identify those superior sites.

The point here is that higher tenant credit quality typically equals higher real estate quality, and this is ultimately the most important thing, as this superior quality will lead to greater profitability over the long run.

Takeaway #2: No Net Lease REIT Comes Close to Agree Realty in Terms of Real Estate Quality

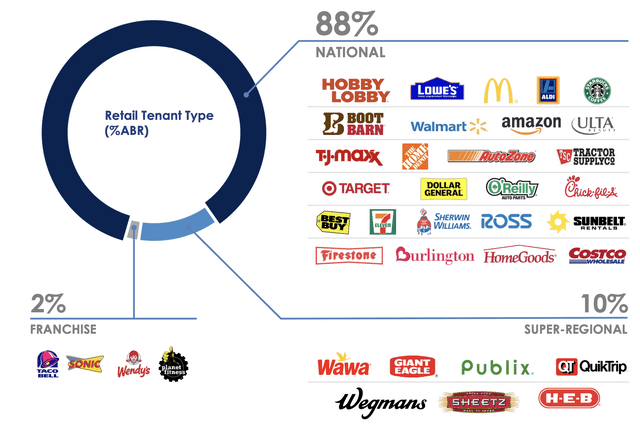

Today, there is really only one net lease REIT left that’s laser-focused on real estate quality, and it is Agree Realty.

Nearly all of its tenants are some of the most successful national retailers, like Costco and Walmart. These retailers are so successful in a big part because they are very picky about the locations of their properties, focusing on growing markets with barriers-to-entry to protect their businesses:

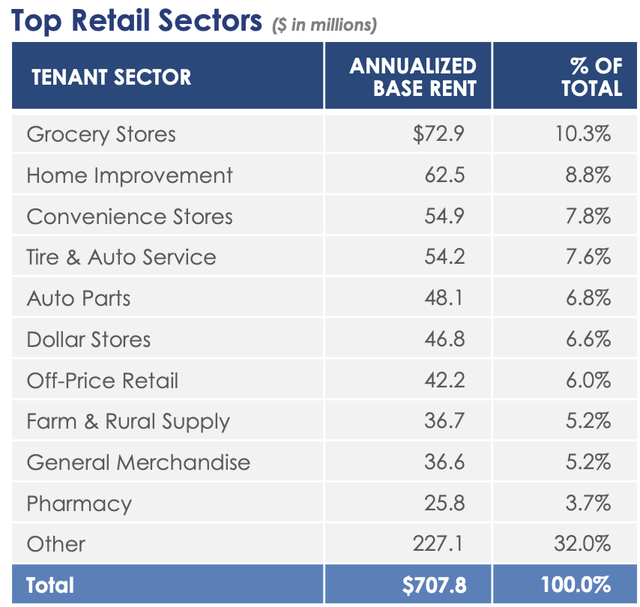

Agree Realty also clearly focuses on more defensive net lease categories that typically have fungible rectangular property types that would be easier to release if needed, and are also recession-resistant:

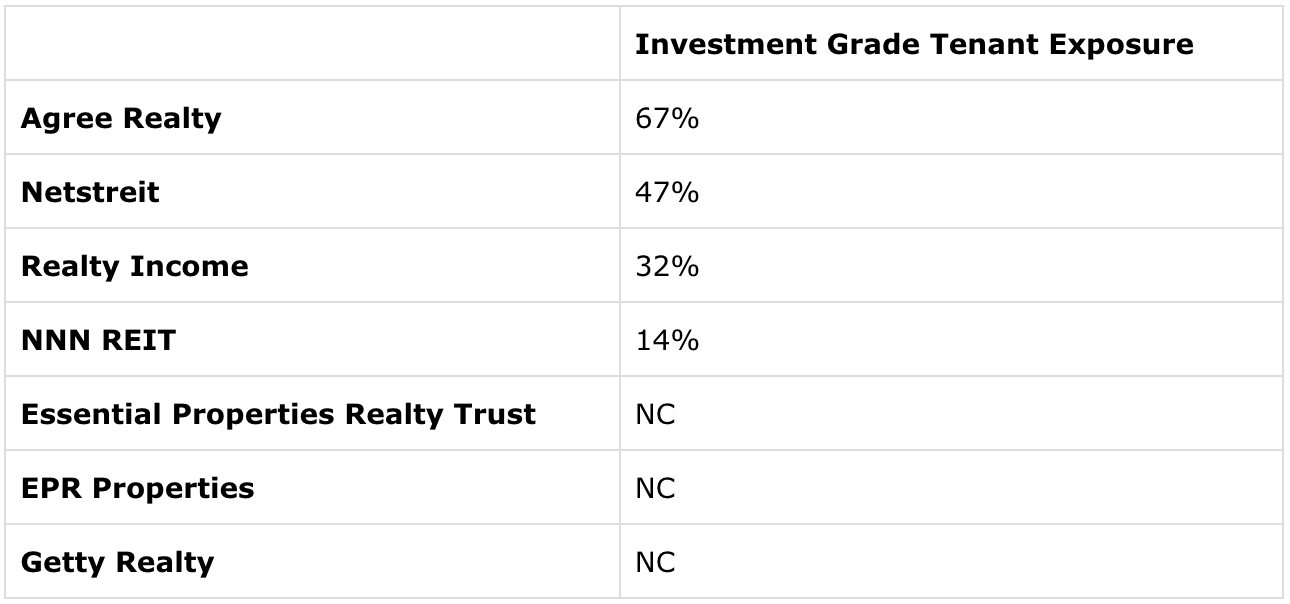

Finally, about 2/3 of its tenants have an investment-grade rating, and the remaining 1/3 are typically highly successful retailers like Aldi and Publix, but they are not rated because they are private.

Here is how it compares to close peers:

Other net lease REITs will often cut corners in order to secure higher cap rates and maximize immediate accretion, which then results in faster short-term FFO per share, at the likely cost of slower long-term FFO per share growth as they eventually hit some setbacks.

Netstreit (NTST) has tried to inflate its investment-grade tenant exposure by heavily investing in dollar stores, which are typically located in secondary and tertiary markets, resulting in poor real estate quality, and in pharmacies, which are today oversupplied and facing poor long-term prospects. Agree Realty has almost entirely sold its pharmacies for this reason.

Realty Income (O) has completely lost its focus on investment-grade rated retailers and is now investing all over the place to make up for its massive size, including vertical farming, industrial properties, casinos, data centers, Europe, etc. Its exposure to investment-grade tenants is now more than 2x lower than that of Agree Realty.

NNN REIT (NNN) made the mistake of stretching its balance sheet for short-term wins, and it is now stuck with quite a bit of exposure to non-fungible assets like car washes and Camping World properties. Reducing this exposure by investing in other categories is now harder due to its higher leverage.

Essential Properties Realty Trust (EPRT) is almost entirely focused on weaker secondary markets with worse barriers-to-entry and lots of non-fungible properties leased to private equity-backed non-rated tenants. In other words, this is some of the worst possible real estate in the net lease category, which will almost inevitably eventually lead to some major setbacks. Car washes, as an example, make up about 15% of its rental income today.

EPR Properties (EPR) may first seem like the worst of the bunch, being almost entirely invested in non-fungible assets with shaky tenants, but the one thing protecting it is that its locations are actually quite decent and enjoy better barriers-to-entry, limiting the risk of future competitors impacting its properties’ profitability. Still, this remains a higher-risk strategy.

Getty Realty (GTY) is also heavily invested in non-fungible properties, such as car washes and gas stations in secondary markets that would be harder to redevelop if and when this property sector becomes oversupplied as a result of electric vehicles gaining market share.

The point here is that no other net lease REIT is even close to Agree Realty in terms of their real estate quality. They will often focus on riskier categories, own less fungible properties in weaker locations, and have much lower exposure to large national investment-grade tenants.

This works fine as long as you have years left on your leases, and the economy is doing fine. But poor real estate quality can only be masked by a lease for so long. Eventually, issues will arise as new competitors enter your market and steal market share, and your tenant defaults and/or your lease expires.

It is also worth remembering that we have not had a proper recession in a long time, and we are long overdue for one to happen. When the tide goes out, you discover who has been swimming naked, and there are lots of net lease tenants that are highly leveraged private equity-backed companies operating in discretionary retail categories like car washes that would likely default on their leases.

Takeaway #3: Focus on Long-Term Sustainable FFO per Share Growth vs. Maximizing Near-term Accretion by Buying Lower Quality Assets

Agree Realty could easily grow faster than it is if it simply went for similar properties selling at higher cap rates.

It would result in greater immediate accretion and faster FFO per share growth in the near term.

However, this would likely come at the cost of slower long-term growth, as it would eventually run into setbacks, which would then likely cause its share price to drop and its cost of equity to rise, limiting its future growth prospects.

So instead of being greedy, Agree Realty continues to focus on the best net lease assets, located in high-barrier-to-entry locations, leased to strong national tenants.

This results in lower immediate accretion as these properties will commonly sell at lower cap rates, but it will result in faster long-term growth as it hopefully avoids painful setbacks and can continue to consistently raise more capital to buy additional properties.

What this means is that a company like Essential Properties Realty Trust may grow faster in the short-to-mid term by acquiring weaker assets and accepting greater risk, but this is likely to eventually lead to setbacks, which is when Agree Realty will then catch up, outperforming its peers over the long-run.

It does not seek to maximize accretion today. It is seeking to maximize growth over the long run. This is achieved by buying the best real estate that’s likely to grow in profitability over time, thanks to their better locations, fungible properties, and stronger tenants.

Takeaway #4: The Denominator Truly Matters for Net Lease REITs

We have often discussed this when referring to Realty Income (O).

The REIT is getting too big for its own good, and this is likely to hurt its growth going forward.

Unlike in other property sectors, there are no economies of scale past a certain point when investing in net lease properties. On the contrary, you start facing clear diseconomies of scale as you must secure a huge volume of acquisitions just to keep the ball rolling.

This forced Realty Income to expand its pipeline and start investing all over the place, at the cost of its portfolio quality.

Agree Realty makes it clear that they will never do that. Instead, if they ever get too big, they will look into breaking the REIT into pieces to remain focused and maintain their growth. There are many options here. They could, as an example, spin off their ground lease assets, representing about 10% of their rental income, into a separate REIT, or they could create a “Walmart REIT”, spinning off all their Walmart net lease properties, representing 6% of their rental income.

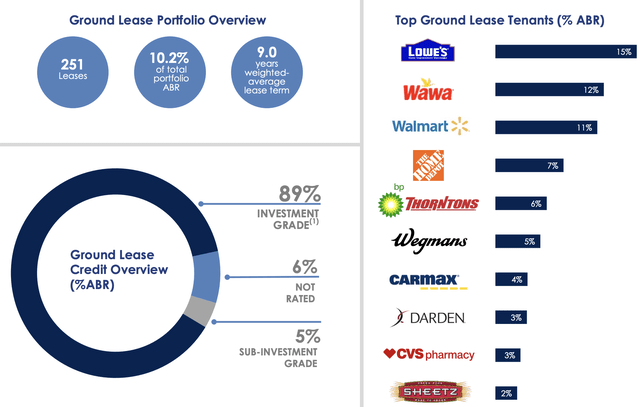

Takeaway #5: Agree Realty’s Ground Leases Are Often Forgotten

Many investors forget that Agree Realty today earns 10.2% of its rental income from ground lease properties with just about 8.8 years left on its leases on average:

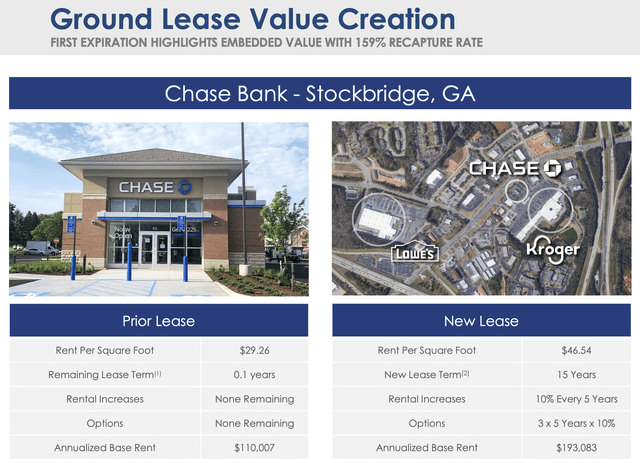

This is a big opportunity for the REIT as these leases gradually expire, and Agree Realty receives ownership of these properties, free of charge.

It will then release the land, plus the building, at materially higher rates, just like it recently did with this Chase Bank, resulting in a 159% recapture rate:

Other net lease REITs have less than 1% exposure to ground leases and won’t enjoy this same long-term tailwind.

Takeaway #6: Agree Realty Has Exceptional Company Culture

They talked a lot about this to me at the University of Michigan: about how Joey Agree has managed to attract the very top talent in net lease space and how they keep them motivated to not just do average, but win in this competitive space.

Their entire office is a reflection of that, from a wall covered with Kobe Bryant to a “war room” where they discuss their next big moves, and Joey Agree’s father, who initially started the company, still being present at the office.

This is also very well reflected in them putting their money where their mouth is. Company insiders have bought $10s of millions worth of stocks in recent years. This includes Joey Agree and his father buying millions, and never selling a share, despite already having the bulk of their net worth invested in the stock, and their compensation plan heavily depending on its performance.

I don’t know any other REIT that comes even close to that. Not just in the net lease sector, but across any REIT category.

Finally, I get the feeling that these are good people, taking good care of their employees, and having a solid moral compass. While this is irrelevant to the investment thesis, I also appreciate that when shortly discussing politics, Joey Agree made it clear that he is very pro-Ukraine and follows the situation closely. This may not matter to you, but it does to me.

Closing Note

Agree Realty has long been Austin’s biggest position by far, representing nearly 10% of its portfolio, and this all now makes a lot more sense to me after getting to meet the team in person and discuss the sector in more detail.

With the stock currently trading at 16.5x FFO and a slight premium to NAV, I don’t think that it has much near-term upside, but it is likely to generate highly consistent double-digit total returns over time from its yield and growth, which is very attractive coming from such a defensive REIT. Its risk-to-reward remains very compelling, and that makes it a great portfolio anchor.

However, being an active investor, I of course would hope to also earn a bit of upside as well, and for this reason, I will wait for a future dip to double down on Agree Realty. I would gladly make it one of my largest holdings, sometimes in the future if the opportunity presents itself.

============================

Access Our Portfolios Via Google Sheets

Our three portfolios are available through Google Sheets. These sheets provide detailed information on position sizes, risk ratings, and key metrics to help you make well-informed investment decisions:

============================

Access Our REIT Market Intelligence Sheet

This exclusive tool includes a list of all equity REITs grouped by property sector, providing all the information you need to make better decisions: FFO multiple, dividend yield, payout ratio, credit rating, and much more.

============================

Access Our Portfolio Tracker

The HYL Portfolio Tracker is a Google Spreadsheet designed specifically for members of High Yield Landlord. It helps you track all your HYL investments in one place with a simple format. It is very easy to use, so don’t miss out on this free feature!

============================

Access Our Live Chat

Our live chat room is where the HYL community comes together to share market news, discuss investment ideas, and help new members get started. Members can post questions and receive prompt answers from other real estate investors and our team.

============================

Finally, feel free to contact us anytime. You can send me a direct message on the chat or email me at jaskola@leonbergcapital.com

Sincerely,

Jussi Askola

Analyst’s Disclosure: I/we have a beneficial long position in the shares of all companies held in the CORE PORTFOLIO, RETIREMENT PORTFOLIO, and INTERNATIONAL PORTFOLIO either through stock ownership, options, or other derivatives. High Yield Landlord® (’HYL’) is managed by Leonberg Research, a subsidiary of Leonberg Capital. All rights are reserved. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The newsletter is impersonal and subscribers/readers should not make any investment decision without conducting their own due diligence, and consulting their financial advisor about their specific situation. The information is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The opinions expressed are those of the publisher and are subject to change without notice. We are a team of five analysts, each contributing distinct perspectives. Nonetheless, Jussi Askola, the leader of the service, is responsible for making the final investment decisions and overseeing the portfolio. We do not always agree with each other and an investment by Jussi should not be taken as an endorsement by other authors. Past performance is no guarantee of future results. Our portfolio performance data is provided by Interactive Brokers and believed to be accurate but its accuracy has not been audited and cannot be guaranteed. Our portfolio may not be perfectly comparable to the relevant index. It is more concentrated and may at times use margin and/or invest in companies that are not typically included in REIT indexes. Finally, High Yield Landlord is not a licensed securities dealer, broker, US investment adviser, or investment bank. We simply share research on the REIT sector.

So Jussi when you talk about adding on a dip. Where do you see the price needing to get to further add to your position. :)

Question: Is Canadian Net REIT following the sale real estate property quality as Agree, or are they more like the others investing a lot in car washes and stuff?