Interview With Agree Realty Corporation (Incl. Trade Alert)

We recently met again with Joey Agree, the CEO of Agree Realty Corporation (ADC), in NYC.

Earlier this year, we met him in Michigan after visiting Agree Realty’s headquarters in person and touring the office. That meeting significantly strengthened our conviction in the company, and we published a detailed investment thesis explaining why we believe that Agree Realty is the highest quality net lease REIT in the market.

This latest meeting gave us another opportunity to discuss the company, the net lease market, and its near-term growth prospects in greater detail.

Our main takeaway is simple:

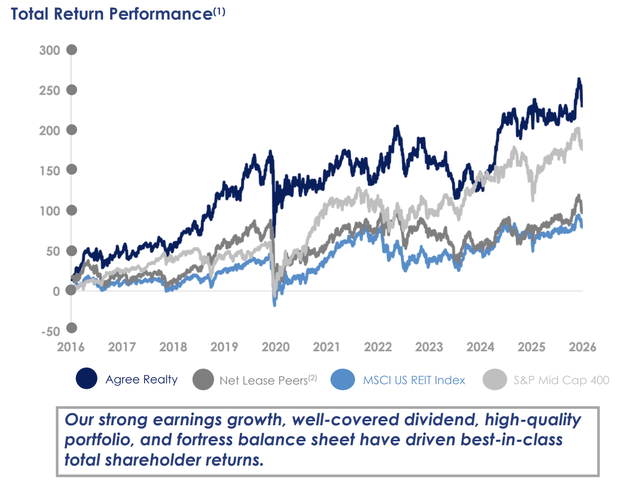

We believe that Agree Realty is now better positioned than ever, and its growth prospects appear to be accelerating and could soon surprise the market to the upside.

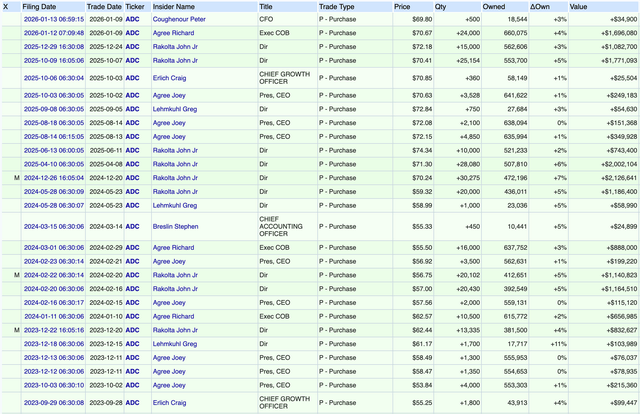

For this reason, we are today increasing the size of our position by buying another 100 shares, increasing our position size by 50%:

To be clear, Agree Realty is not cheap. It rarely is.

But the stock has recently dipped by about 11%, even as we think that its future growth prospects have improved further. We do not expect significant near-term upside from multiple expansion alone, perhaps a little bit, but we believe that the market is underestimating how strong its near-term results could be, potentially already in Q2. This could help it quickly regain those recent losses, and beyond that, we would expect steady double-digit annual total returns from the 4.4% dividend yield and 6% average annual long-term growth.

This is why we are now taking advantage of the dip to bulk up our position.

Here is a recap of our investment thesis, what has changed, and what we learned from our latest one-to-one with the CEO of the company.

Why We Like Agree Realty

Let us first recap why we like Agree Realty so much.

When we visited the company earlier this year, what stood out to us was that this is not just another large public REIT run by professional managers.

This is a family company.

The Agree family name is on the company, on the door, and heavily invested in the stock. Joey Agree and his father have bought millions of dollars’ worth of shares over the years, and they have never sold a share, despite already having most of their net worth tied to the company.

Joey also told us that the family will never sell a share.

That is extremely rare.

I do not know any other REIT that comes close to this level of insider ownership, insider buying, and long-term alignment. Not just in the net lease sector, but across the entire REIT market.

This matters because the net lease REIT business is very easy to mess up if management is too focused on near-term growth.

You can always buy lower-quality assets at higher cap rates, show more immediate accretion, and grow FFO per share faster for a while.

But over time, the quality of the real estate matters more than the lease.

A weak location, a non-fungible building, and a highly leveraged private equity-backed tenant can look fine for years, until competition increases, tenant profitability declines, and the tenant eventually defaults or refuses to renew.

This is why we think that a lot of net lease REITs are taking more risk than the market realizes.

They are buying higher cap rate properties because they want near-term accretion, but they are often accepting weaker locations, less fungible buildings, and lower quality tenants to get there.

Agree Realty is doing the opposite.

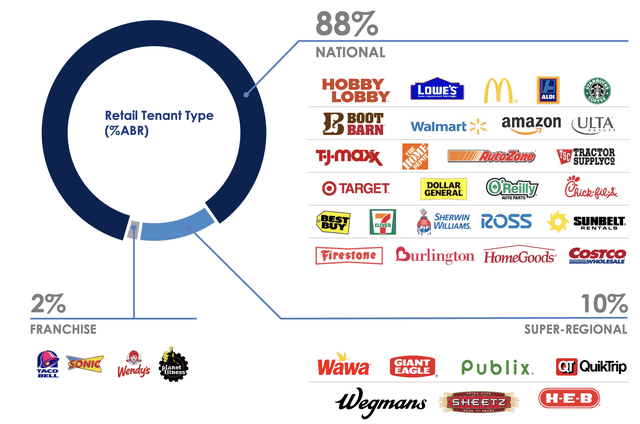

It focuses on the best real estate, leased to some of the strongest national retailers, in defensive categories, with a heavy focus on fungible property types that can be released if needed.

This is the main reason why Agree Realty has the best track record in the net lease sector.

It has not been the most aggressive.

It has been the most disciplined.

That discipline has allowed it to avoid major setbacks, maintain a low cost of capital, and compound at an attractive rate over long periods of time.

Real Estate Quality First

A key point that Joey emphasized to us is that tenant credit quality and real estate quality are closely connected.

Some net lease investors argue that tenant credit quality does not matter much because what really matters is the profitability of the real estate. If the tenant is profitable at a specific location, it is unlikely to vacate, even if it goes through financial stress.

That is true to some extent.

But it misses an important point.

The tenants with the best credit quality will typically end up with the best real estate in most cases.

That is because landlords and developers would almost always rather lease a property to a high-credit tenant if they can. A Walmart, Costco, Home Depot, or McDonald’s lease will typically result in a lower cap rate and, therefore a higher property value.

So if a developer has a great site in a strong market, with good visibility, access, traffic counts, and barriers to entry, it is likely to prioritize the strongest possible tenant.

This is why tenant credit quality cannot simply be ignored.

It is not just a tenant metric. It is often an indicator of real estate quality.

The best tenants have the resources, data, and bargaining power to secure the best locations, and landlords have a strong incentive to lease their best properties to these tenants because doing so increases property value and lowers risk.

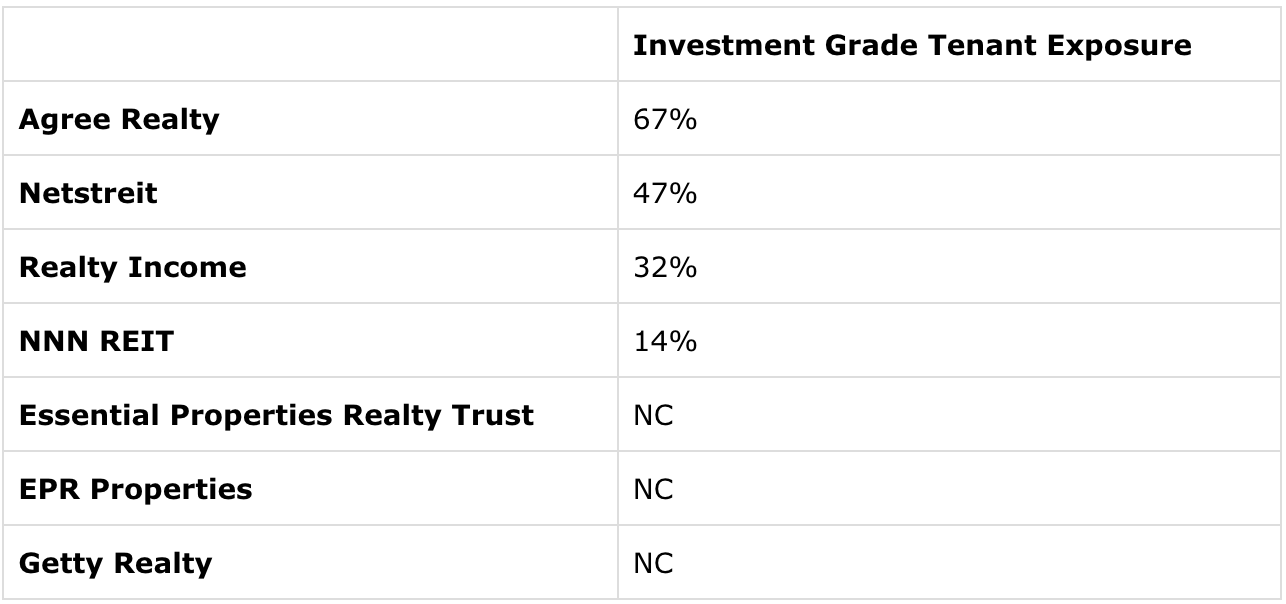

Agree Realty has the highest exposure to these types of tenants in the net lease sector.

That matters a lot as it suggests that Agree Realty is not just collecting rent from stronger tenants. It also owns better real estate.

This is very important because profitability can change over time. If a property is located in a weak market with few barriers to entry, a competitor can build a better location nearby, take market share, and suddenly reduce the profitability of the original location.

This is especially problematic if the building is non-fungible and cannot easily be released to another tenant.

Car washes are a good example.

They can look great when they are new, and the rent coverage is high. But if competition increases and the market becomes oversupplied, that profitability can fall quickly. If the tenant then defaults, the landlord may be left with a highly specialized property that is difficult to release without a major rent cut.

Agree Realty largely avoids this type of risk.

Its portfolio is focused on leading national retailers in defensive categories, and many of its properties are relatively simple, rectangular boxes that could be released to other users if needed.

That gives the company a much better margin of safety.

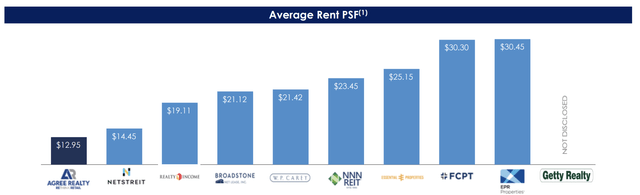

Another important point is that Agree Realty has some of the lowest rents per square foot in the net lease sector, despite owning some of the best real estate.

At first, this may seem contradictory. Why would the best real estate have lower rents?

The reason is that the best tenants often negotiate the best rent terms. Large national retailers like Walmart, Costco, and other leading operators have scale, credit quality, strong bargaining power, and a lot of choices. Developers and landlords want these tenants because they lower the risk of the property and increase its value.

So they often accept lower rents in exchange for better tenant quality, stronger long-term durability, and margin of safety.

This is the type of tradeoff that we like.

Agree Realty may not always maximize rent per square foot, but it maximizes the quality and durability of its cash flow. That is far more important for long-term compounding.