Interview With FrontView REIT (Watchlist Addition)

I recently had the chance to visit the headquarters of Agree Realty Corporation (ADC), where I met their management team for an exclusive interview.

You can read it by clicking here.

This meeting with ADC left me wanting to own more of it. The REIT truly stands out in the net lease peer group in that it owns the best real estate, has arguably the best management team, and enjoys very attractive long-term prospects.

But there’s one issue. The REIT’s share price has strongly recovered, and it now trades at near fair value, limiting its near-term upside potential.

I think that it still should be able to earn near double-digit total returns to its investors from its yield and growth.

However, being an active investor, I would also want to earn some additional upside on top of that.

This led me to look for a similar but cheaper alternative, and that’s how I landed on FrontView REIT (FVR). It is a net lease REIT that IPOed just one and a half years ago and has mostly flown under the radar because of its small size and lack of analyst coverage.

- by Real Assets Value")

But it shares important similarities with Agree Realty:

Both focus on real estate quality first, lease second. They target fungible buildings in strong locations, typically occupied by service or necessity-oriented businesses. FVR is so confident in its real estate that it provides the best disclosures in its peer group, including even the addresses of every property it owns.

Both invest heavily in ground leases, generating 10%+ of their rental income from them. They are the only two net lease REITs to do that. It may provide opportunities to materially increase rents as leases expire and improvements revert back to them.

Both have shareholder-friendly management teams that focus intensely on growth on a per-share basis and own 10%+ of the equity themselves. Both management teams also come from a shopping center development background, which is unique for net lease REITs, and likely explains why they follow similar investment approaches.

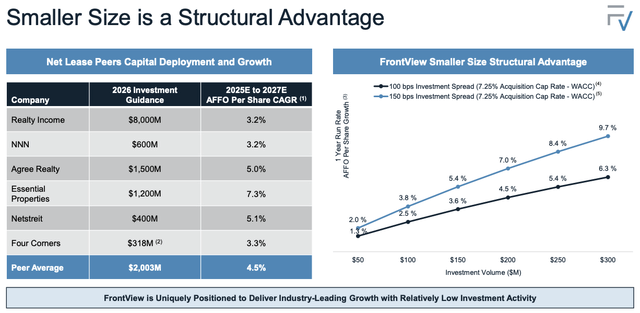

Both appreciate how much of an advantage it is to be smaller in size, and openly point out how a large denominator can hurt growth in net lease investing. FVR is, however, still 20x smaller than ADC, which may potentially allow it to grow even faster over the long run.

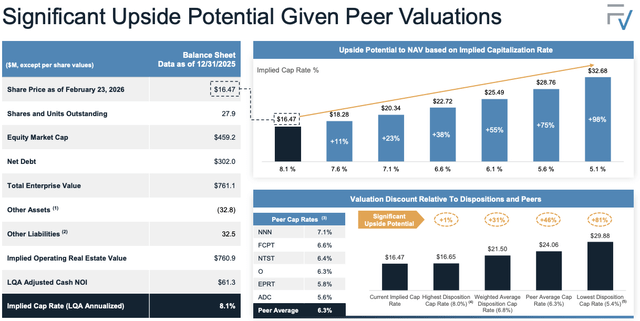

Even then, its valuation is quite a bit lower than that of ADC. Its Price-to-AFFO multiple is lower at 12.5x vs. 17.7x for ADC, but this does not fully capture the discount because FVR is still subscale and its management cost is much higher as a percentage of total assets.

A useful valuation measure here is the implied cap rate, which is 8.1% for FVR, but just 5.6% for ADC. That’s a huge spread:

What this means is that its share price would need to rise by 75% to trade in line with ADC.

That’s unlikely, of course, as ADC is a bigger REIT, it has a better balance sheet, a longer track record, and it also generates a greater share of its revenue from investment-grade rated tenants.

But on the flip side, FVR also has its own advantages:

It enjoys bigger average rent escalators at 1.7%, compared to closer to 1% for ADC.

It has a lower payout ratio at 65% of its AFFO, compared to 70% for ADC.

Its average remaining lease term is just 7.4 years, compared to 9 years for ADC. I view this as an advantage in the case of FVR, as it owns properties with below-market rents and has a history of enjoying strong recapture rates at lease expiration.

It has a bit more ground lease exposure at 11.5% vs. 10.2% for ADC.

It owns fewer big box stores, which could be harder to release in case of vacancy.

It is a lot smaller in size with a $450 million market cap, meaning that it can afford to be a lot more selective than ADC, and each new investment will have a much bigger impact on its bottom line.

The smaller size also means that the management should be able to more easily create value via portfolio recycling. FVR has sold a large portion of its portfolio in recent years to reinvest at a positive spread.

Over time, we think that it will likely reprice at closer to a 7% implied cap rate, which would still be near the bottom of the net lease peer group, but price the stock at $22.50, implying 40% upside.

This, of course, won’t happen overnight, but the stock pays a 5.4% dividend yield in the meantime, and the REIT has guided to grow its AFFO per share by 4% in 2026. The REIT has a decent balance sheet, with a 5.6x Debt-to-EBITDA, a 34% LTV, and enough liquidity for its planned acquisitions in 2026.

In some ways, this also reminds me of when Essential Properties Realty Trust (EPRT) went public. Their investment approaches are very different, but the situation is similar in that EPRT had to earn its respect before the market eventually rewarded it with the multiple that it deserved.

To earn this respect, EPRT went on a media tour, reaching out to investors, pitching their REIT, and eventually, this paid off as investors bid up the share price, unlocking access to cheaper equity to raise capital and accelerate growth.

This growth, coupled with multiple expansions, has resulted in 20% average annual total returns for shareholders since its IPO:

We think that FVR could be the next success story.

To learn more about it, we reached out to their company for an exclusive interview and had the chance to talk with their CFO, Pierre Revol: