IWG: A Huge Potential Winner Of The AI Revolution

Earlier this year, we built International Workplace Group (IWG / IWGFF) into the single largest holding in our Core Portfolio, representing a sizable 11.3% allocation. So far, it has performed very well, rising by nearly 40% off its recent lows.

Quick side note—it is always funny to see how little attention strong performers get. Our inbox is full of questions about Alexandria Real Estate (ARE), yet no one seems to ask about IWG, despite it being a far larger position for us. That is the nature of newsletters: winners tend to get ignored.

But the key question now is this: has IWG already reached its fair value?

In our view, it has not. In fact, we believe IWG offers more upside potential than ever. The investment case has only strengthened throughout 2025 due to one major catalyst: the rapid acceleration of artificial intelligence and its coming disruption of the office sector.

The way we work is being reshaped faster than anyone expected. Artificial intelligence is already automating millions of tasks, compressing job roles, and reducing the need for large administrative headcounts. In just a few years, the size and structure of office-based workforces may look completely different. And yet, the traditional office lease still expects companies to commit for five to ten years. That disconnect is becoming a serious liability. In a world where businesses can no longer predict how many employees they will need in two to three years, locking into a long-term lease is increasingly seen as reckless. Companies want flexibility. They want cost efficiency. They want optionality.

This is exactly what IWG provides.

In today’s article, we provide a full update on our thesis and explain why IWG could turn into one of the biggest real estate winners of the AI revolution.

Before continuing, we encourage readers to revisit our full investment thesis on IWG by clicking here.

The AI Shockwave Is Just Beginning

The office sector is on the verge of a major disruption.

According to the CEO of Anthropic, AI could push unemployment up to 10–20% in the next five years if current trends persist. That disruption will hit white-collar workers first: lawyers, accountants, consultants, marketers, and administrative staff are all under pressure.

Junior positions, in particular, are being eliminated. The unemployment rate for recent college graduates is already spiking.

A law firm that once needed 10 people to draft contracts may now need only 3 in the future, thanks to AI tools.

In finance, AI can now write 95% of an IPO prospectus in minutes, replacing weeks of work by teams of analysts, according to the CEO of Goldman Sachs.

In marketing, AI can already generate landing pages, advertisements, and visual content better, faster, and cheaper than human teams.

This is deeply negative for traditional office landlords.

But it is a massive tailwind for IWG.

Why?

Because rising workforce uncertainty makes long-term leases unviable.

As one of IWG’s largest shareholders recently told us:

“A steady bleed in white-collar jobs is extremely bullish for short-term lease demand. Who in their right mind would sign a 10-year lease if they have no idea how many employees they will have in 2–3 years?”

Companies will increasingly avoid long leases and instead opt for flexible, on-demand office space. AI is greatly accelerating a structural shift that was already underway.

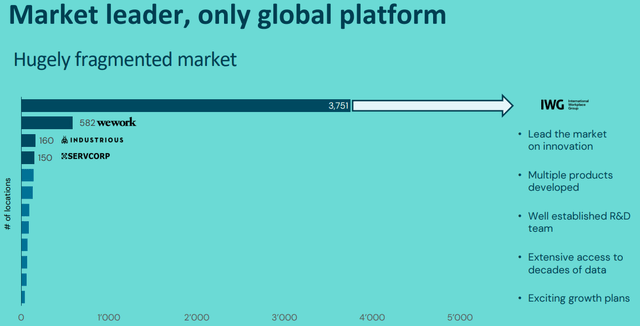

Dominant Market Position

IWG is the global leader in this exact niche.

It is far larger than its closest competitor, WeWork.

IWG has spent decades building out its network, giving it unmatched scale:

This scale serves as a moat, as large corporations prefer to work with a provider like IWG because it gives their workforce access to a vast global footprint. Smaller players cannot offer that.

As companies transition from traditional leasing models to flexible arrangements, we expect the organic growth of IWG’s portfolio to accelerate.

While some worry that AI could reduce overall demand for office space, the more likely outcome is a redistribution of that demand. Traditional office landlords may suffer, but flexible providers like IWG are poised to absorb a growing share of what remains.

Capital-Light Expansion

In late 2022, IWG pivoted to a capital-light growth model focused on signing management deals with landlords, similar to what Marriott (MAR) or Hilton (HLT) do in the hotel sector.

Since then, growth has exploded:

400 new managed partnerships signed in 2022

839 in 2023

899 in 2024

Targeting 1,000 more in 2025

To put this in context, IWG currently operates just around 4,000 locations. This is a massive growth rate, and AI-driven demand may now accelerate it even further.

Landlords are turning to IWG to operate their space under flexible terms because that's what increasingly many tenants are demanding. And IWG is the only large-scale player that has proven it can profitably operate flexible offices. WeWork never figured that out, which is why it went bankrupt.

The Market Potential Is Enormous

In 2010, only about 1% of office space was flexible. Today, that figure has already reached 5%. According to JLL, it could reach up to 30% by 2030.

But that forecast came before the AI disruption. With future headcounts now uncertain for most firms, 30% may prove conservative.

As the dominant operator, IWG is well-positioned to capture this growth.

Moreover, IWG is also a tech company. It owns and operates Worka, a platform that allows users to book desks, offices, and meeting rooms on demand, similar to how Airbnb enables travel bookings.

In fact, the analogy is instructive. The global office market is about 5x larger than the hotel market. Yet Airbnb’s market cap is around $82 billion, while IWG’s sits at just $2.7 billion. It is still just getting started.

Valuation Remains Extremely Attractive

Despite all this, IWG trades at just 8x estimated 2025 free cash flow. That is astonishingly low for a company with rapid growth prospects and significant tailwinds from industry-wide disruption.

Debt is also rapidly coming down, with management targeting a 1x Debt-to-EBITDA ratio later this year. At that point, share buybacks are expected to ramp up. They announced a $50m share buyback programme in March, and they have already completed most of it.

Further validation of the sector came from CBRE’s recent acquisition of Industrious, one of IWG’s smaller competitors, for $800 million. That deal valued each location at a multiple roughly 6x higher than where the market currently values IWG. Yet IWG has nearly 20x more coverage and better margins.

Final Thoughts

The flexible office sector is no longer a fringe segment. It is going mainstream. And with AI reshaping the future of work, the trend is only accelerating.

IWG is:

• The only global player of scale

• Growing fast with minimal capital investment

• Operating a proprietary booking platform (Worka)

• Trading at a deep discount to intrinsic value

In a world where agility is king, IWG might become one of the biggest real estate winners of the AI revolution.

We believe IWG could be a multi-bagger over the next five years as flexible offices go from niche to dominant.

And yet, hardly anyone is paying attention.

We are.

That is why IWG remains our single largest holding. And that is why we are more bullish than ever.

Finally, please note that we have exceptionally posted this article without a paywall. If you found it valuable, consider joining High Yield Landlord for a 2-week free trial.

You will also gain immediate access to my entire REIT portfolio, real-time trade alerts, exclusive REIT CEO interviews, and much more. We are the largest and highest-rated REIT investment newsletter online, with over 2,000 paid members and more than 500 five-star reviews.

We spend thousands of hours and over $100,000 per year researching the market for the most profitable investment opportunities, and we share the results with you at a tiny fraction of the cost.

Get started today - the first 2 weeks are on us:

Analyst's Disclosure: I/we have a beneficial long position in the shares of all companies held in the CORE PORTFOLIO, RETIREMENT PORTFOLIO, and INTERNATIONAL PORTFOLIO either through stock ownership, options, or other derivatives. High Yield Landlord® ('HYL') is managed by Leonberg Research, a subsidiary of Leonberg Capital. All rights are reserved. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The newsletter is impersonal and subscribers/readers should not make any investment decision without conducting their own due diligence, and consulting their financial advisor about their specific situation. The information is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The opinions expressed are those of the publisher and are subject to change without notice. We are a team of five analysts, each contributing distinct perspectives. Nonetheless, Jussi Askola, the leader of the service, is responsible for making the final investment decisions and overseeing the portfolio. We do not always agree with each other and an investment by Jussi should not be taken as an endorsement by other authors. Past performance is no guarantee of future results. Our portfolio performance data is provided by Interactive Brokers and believed to be accurate but its accuracy has not been audited and cannot be guaranteed. Our portfolio may not be perfectly comparable to the relevant index. It is more concentrated and may at times use margin and/or invest in companies that are not typically included in REIT indexes. Finally, High Yield Landlord is not a licensed securities dealer, broker, US investment adviser, or investment bank. We simply share research on the REIT sector.

I must rise in objection to part of your very rosy analysis of IWG. Your technical and financial considerations of its value may well be on point. However, many of the users of this office space provider have expressed a great deal of unhappiness on Internet review sites regarding the service provided by a IWG. To my point trust pilot.com “consumers express widespread dissatisfaction across multiple facets of the business. Many people report issues with contracting the company, siting unhelpful staff, and a lack of focus on providing solutions. The main points appear to revolve around payment discrepancies and unresolved issues.” Complaints board.com sites “deceptive tactics and dishonest dealing.” There are extensive articles about many people having contract issues, can’t terminate contracts and having terrible experiences with IWG. I was very excited to learn of IWG in your initial writings on it some months ago, so I did just a little research and all these articles came up about unhappy customers. Is there anyway that you can address this issue to assure or comfort those who may be using the service or thinking of investing in this company?

I've discounted IWG the first time because it has very low dividend yield and Switzerland HQ - which has a horrible dividend withholding tax that is a hassle to reclaim.

As a (growing) dividend investor with a buy-and-hold whenever-possible mentality, are the reasons to buy this stock overruling my reasons not to buy this stock?