Time To Buy Hotel REITs?

Dear Landlords,

I want to extend a warm welcome to all our new members!

As a reminder, our most recent “Portfolio Review“ was shared with the members of High Yield Landlord on April 2nd, 2026. You can read it by clicking here.

You can also access our three portfolios on Google Sheets:

New members can start researching positions marked as Strong Buy and Buy while considering the corresponding risk ratings.

============================

Time To Buy Hotel REITs?

Most REITs have been strongly recovering so far this year. They are up about 10% on average, and many property sectors are up closer to 20% as rent growth improves, interest rate fears slowly subside, and capital rotates toward hard assets that are less exposed to AI disruption.

Even after that rebound, REITs still remain undervalued in many cases and offer meaningful upside potential.

However, as prices recover, it is of course getting harder to find the steep discounts that we got used to seeing over the past couple of years.

That has led a few of you to ask me whether now could be a good time to invest in hotel REITs.

I understand the appeal.

Hotel REITs typically trade at some of the lowest multiples in the REIT sector. Even the highest quality blue chip in the space, Host Hotels (HST), trades at just around 10x FFO, which is far below the typical multiple of a large, high quality REIT. Many of the smaller and lesser-known hotel REITs also trade at steep discounts to NAV and offer high dividend yields. Pebblebrook Hotel Trust (PEB) is one example, trading at a 40% discount.

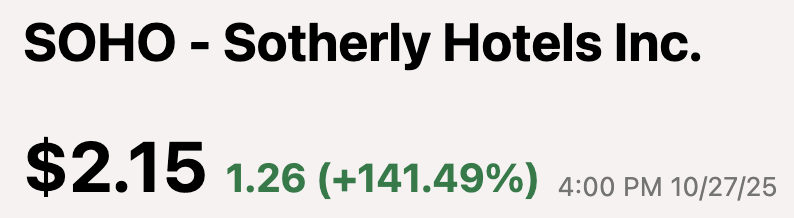

We have also seen hotel REIT buyouts in the recent past. That is another reason why the sector draws interest. When a hotel REIT gets taken private, the premium can be very large, which reinforces the perception that public market pricing may be too pessimistic. Sotherly Hotels (SOHO) was bought out at a huge 140% premium!

All of this seems to indicate that hotels could now offer a compelling opportunity.

So why not invest in them?

Cheap Does Not Always Mean Attractive

In short, hotels are among my least favorite property types.

Yes, they are cheap, but in my opinion, they are cheap for very good reasons.

Hotels are management-intensive, require substantial capital expenditures, are highly cyclical, and face increasing pressure from disruptive technologies and the current political climate. This makes them very different from the types of real estate that I generally want to own for the long run.

A low multiple is not enough to make an investment attractive.

Cyclical assets deserve to trade at lower multiples, especially if we are potentially approaching the peak of the cycle, and a good portion of current earnings may not be sustainable through the next downturn.

Moreover, that multiple should be especially low if there are also long-term concerns about the supply and demand outlook for the property type.

That is exactly the situation that I see with hotels.

Hotels Are Operating Businesses, Not Passive Real Estate

The first issue is that hotels are not really passive real estate investments.

They are operating businesses wrapped in real estate.

When you own an apartment building, a net lease property, or a shopping center, you sign leases and then collect rent. There is still work involved, but the revenue stream is relatively contractual and predictable.

Hotels are very different.

Rooms must be priced daily. Staff must be managed daily. Customer satisfaction must be maintained daily. Occupancy can change overnight. Margins can swing quickly. Performance depends not just on the quality of the real estate, but also on operations, brand positioning, labor management, and constant execution.

That makes hotels much more management-intensive than most property sectors. This is one reason why I do not view them as especially attractive real estate investments. The more operational complexity there is, the less durable the investment tends to be.

Hotels Require Heavy Ongoing Capital Spending

The second issue is capital intensity.

Hotels wear out quickly. Guests expect updated rooms, attractive common areas, modern technology, good food and beverage offerings, and a high service standard. To remain competitive, hotel owners must constantly reinvest into renovations, upgrades, and maintenance.

This is not optional. It is a permanent feature of the business model. As a result, headline cash flow numbers can overstate the true long-term earning power of hotel assets because a significant portion of that cash flow needs to be reinvested just to maintain competitiveness.

That is very different from many other forms of real estate, where maintenance capital is lower, and the cash flow is more durable.

So while a hotel REIT may look cheap on FFO, I do not think investors should take that at face value. The real free cash flow is often much less impressive than it first appears.

Hotel Earnings Are Highly Cyclical

The third issue is cyclicality. Hotels do not benefit from long lease agreements.

That is a major weakness.

If the economy weakens, consumers pull back on discretionary spending, corporate travel budgets get cut, or tourism softens, hotel earnings can fall very quickly. There is no long-term lease protecting the landlord. Pricing resets every night.

This is why hotel REITs deserve to trade at lower multiples than apartment REITs, industrial REITs, net lease REITs, and others.

A meaningful portion of hotel earnings at the top of the cycle is often not sustainable. Investors who buy based on current earnings alone can easily end up overpaying for what looked like a low multiple.

This is particularly important today because we may already be relatively late in the cycle. If that is the case, then hotel cash flows may be closer to peak earnings than normalized earnings.

That makes the apparent cheapness less compelling.

The Supply Side Is a Major Concern

If I am going to invest in a risky cyclical property sector, I at least want it to be supply-constrained.

Hotels generally are not. In many markets, it is not particularly difficult to build new hotels if the economics justify it. The barriers to entry are simply not very high compared to other property types that benefit from greater zoning restrictions, irreplaceable locations, licensing limitations, or other structural constraints.

But even more importantly, hotels no longer just compete with other hotels. They compete with Airbnb-like alternatives and other short-term rental platforms that have created a huge new source of room supply. Anyone with an extra room, apartment, or house can increasingly compete with traditional hotels.

I think AI will make this even worse over time. AI is great at breaking barriers to entry. It makes operations easier, cheaper, and more scalable. In the case of alternative accommodations, AI can help with pricing, customer service, check-in, check-out, guest communication, screening, cleaning coordination, and marketing.

In other words, AI may make hosting easier than ever before. That could bring even more supply into the market and intensify competition for traditional hotels.

This is the exact opposite of what I want from a long-term real estate investment. I want assets where scarcity protects value. Hotels do not offer that.

Demand Is Also Becoming Less Attractive

The demand side worries me as well.

Near-term international travel to the United States has weakened as many foreign travelers choose to spend their tourism money elsewhere. I do not say this in a political way. It is simply a reality that rhetoric, policy uncertainty, and broader sentiment can affect travel demand. Hotels are highly exposed to those shifts, and it is negatively impacting the American hotel market right now.

Beyond that, business travel also faces long-term pressure.

Zoom and other virtual meeting platforms have reduced the need for many business trips. In fact, with AI now helping with translation, notes, analysis, etc., it is often easier and more effective to hold a meeting digitally than in person.

Business travel is not disappearing, but it does not need to disappear to hurt hotels. It only needs to be structurally lower at the margin. That matters because hotels used to benefit significantly from business demand that was relatively recurring and less seasonal.

Booking Platforms Are Taking More of the Economics

Another concern is that booking websites are taking an ever bigger cut of hotel revenue.

Hotel flags and brands are losing some of their value because consumers are less loyal and more focused on comparing options across platforms. With AI tools improving search and recommendation engines, this trend could intensify further.

Instead of going directly to a hotel brand, many consumers now start with a booking platform, compare properties side by side, and choose whichever one looks best for the price. That weakens pricing power and shifts power away from the hotel owner.

It also means more of the economics are being captured by intermediaries.

Again, this is not what I want in a long-term real estate investment. I want the owner of the hard asset to retain pricing power and customer value. In the hotel business, too much of that is leaking away.