TRADE ALERT - Core Portfolio March 2026

When we first invested in RCI Hospitality (RICK), the thesis was fairly simple. The company owned a portfolio of highly cash-generative nightclubs and valuable real estate, yet traded at a deeply discounted valuation.

Importantly, its management also had a long track record of creating shareholder value through acquisitions.

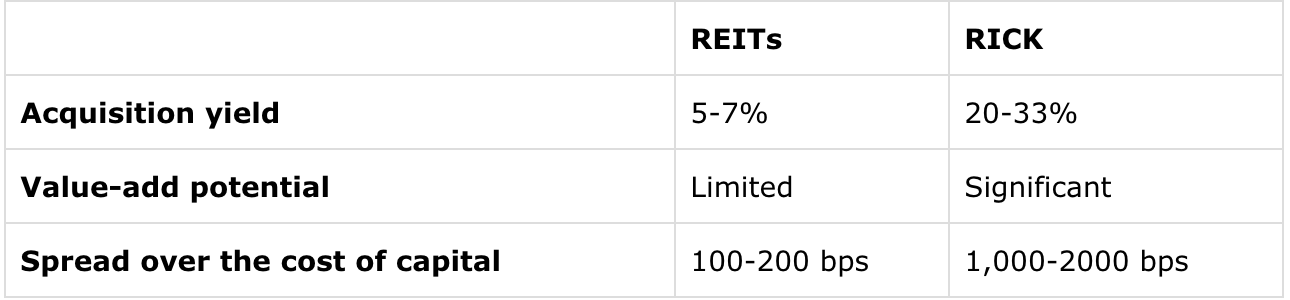

I described it as a “REIT on steroids” because of its economics. RICK was acquiring clubs at 20–33% cash flow yields, generating massive spreads over its cost of capital. By comparison, most REITs are happy acquiring assets at 5–7% cap rates, earning far smaller spreads.

What makes this possible is a unique competitive advantage. RICK is essentially the only acquirer of scale in a highly fragmented industry, with access to public capital. At the same time, many club owners are approaching retirement, creating a steady pipeline of willing sellers. Yet, few buyers exist due to the stigma and operational complexity of these assets, which further strengthens RICK’s position.

This allows the company to deploy capital at exceptionally high returns. On top of that, most acquisitions come with significant value-add potential. RICK is often able to increase cash flow by 15–20% post-acquisition through better pricing, improved operations, and cost efficiencies from scale.

The result is a consolidation business model with exceptional economics:

This model has historically allowed the company to grow FCF per share at roughly 15% annually. Combined with multiple expansion, it generated exceptional returns for shareholders until its recent crash.

But then interest rates surged, and real estate-heavy companies fell out of favor. RICK dropped even more than the rest as its businesses also suffered from post-COVID normalization.

As a result, its stock was already cheap, and that’s when the legal indictment hit, pushing its sentiment even lower.

That legal issue is serious and should not be minimized. New York state alleged that RICK underpaid certain sales taxes tied to its voucher system at three clubs and also brought bribery-related allegations involving a state tax auditor. This was clearly bad news, and it created a lot of uncertainty around management, legal costs, the company’s filings, and even its NASDAQ compliance. As a result, the stock sold off sharply, and investors were left in the dark for months as the company delayed its 10K.

You can read our thoughts on this entire saga by clicking here.

But now we finally have much more clarity, and in my view, the latest update was very good news.

RICK has finally filed its 10K and even held a conference call to answer investor questions. RICK’s founder, Eric Langan, was also present. For months, investors had been left in the dark, and that is never good, especially when a company is dealing with serious legal issues. The delayed filing was primarily due to additional audit procedures tied to the New York state indictment, which the company itself identified as the main reason for the delay. The fact that the auditors ultimately signed off is reassuring. There was always a risk that the auditors could uncover something new and refuse to sign off, but the financial statements now received an unqualified audit opinion. Just as importantly, these filings are required to maintain the company’s NASDAQ listing, so this meaningfully reduces the risk of a delisting. Management also said that the 10Q should follow relatively soon, likely in April, which makes sense since the 10K was the main bottleneck and the quarterly filing is shorter and only reviewed rather than fully audited.

On top of that, the actual operating results were quite good.

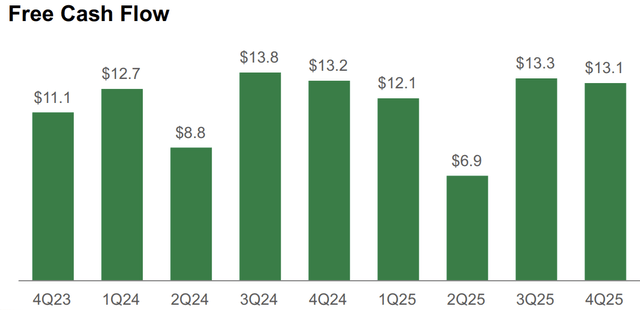

The biggest takeaway from the call is that business continues largely as usual. The company generated another $45 million of free cash flow in fiscal 2025, including $13 million in Q4 alone. It is a good reminder that the legal case has no material impact on the actual business.

Most importantly, they are buying back shares very aggressively and reaffirming their five-year capital allocation plan. The company still targets $400 million in revenue, $75 million in free cash flow, and 7.5 million shares outstanding by fiscal 2029, with the goal of doubling free cash flow per share to about $10 relative to fiscal 2024. At the current pace of buybacks, they may get there even sooner. The share count is already down to roughly 7.7 million, about 14% lower than at September 30, 2024.

In that sense, this crisis may turn out to be a blessing in disguise. The stock is trading at an extremely depressed valuation, roughly 3.5x current free cash flow and about 2x management’s 2029 free cash flow target. That gives the company an opportunity to retire shares at an extraordinary pace with internally generated cash flow. Eric Langan made this very clear on the call. He said that as long as the stock trades below $36.50 per share, they intend to use 100% of free cash flow for buybacks rather than acquisitions.

I love that. It is exactly the right move. Why buy outside assets at higher valuations when you can buy your own business at a fraction of its intrinsic value?

This is what makes the setup so compelling.