TRADE ALERT - International Portfolio May 2026 (Trimming A Winner)

Dear Landlords,

I want to extend a warm welcome to all our new members!

As a reminder, our most recent “Portfolio Review“ was shared with the members of High Yield Landlord on April 2nd, 2026. You can read it by clicking here.

You can also access our three portfolios on Google Sheets:

New members can start researching positions marked as Strong Buy and Buy while considering the corresponding risk ratings.

============================

TRADE ALERT - Trimming Helios Towers And Reinvesting Into Shurgard Self Storage

We invested heavily in Helios Towers (HTWS / HTWSF) in 2022 and 2023 when it was trading right around 100 British pence per share.

Our average cost basis is actually slightly below that, at 93 pence per share.

Today, just a few years later, Helios is trading at roughly 242 pence per share, and as a result of this huge surge, it has become our largest position by far, representing about 16% of our International Portfolio.

This has been one of our best investments of the past few years.

The share price has increased because the company’s cash flow has surged, its balance sheet has improved, and its valuation multiple has rerated higher, exactly as we had expected.

Even then, we still think that Helios remains very attractive for long-term investors.

At today’s share price, Helios has a market cap of roughly £2.5 billion, or about $3.4 billion. Management is guiding for $215 million to $230 million of RFCF in 2026, which is the closest equivalent to AFFO in their reporting. That puts the company at roughly 15x 2026 RFCF.

But this guidance includes a roughly $20 million working capital outflow. If that normalizes in 2027, then normalized RFCF would already be closer to $235 million to $250 million.

On top of that, management expects its tenancy pipeline to add more than $15 million of annualized RFCF from 2027 onward. This implies potential normalized RFCF of roughly $250 million to $265 million, putting the valuation closer to just 13x forward normalized RFCF.

That is not expensive for a company that could potentially enjoy double-digit annual AFFO per share growth for a long time to come.

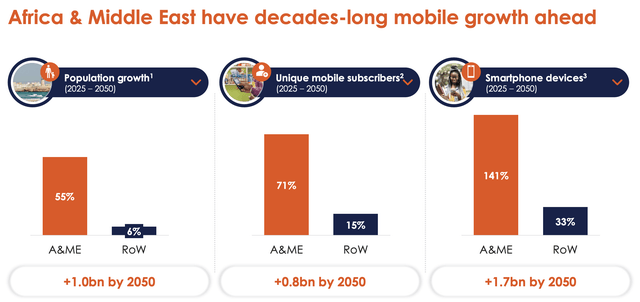

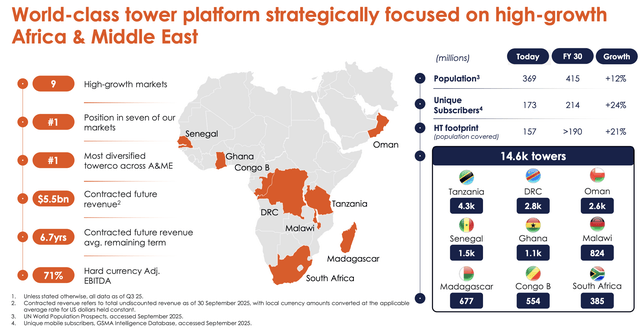

The consumption of data is exploding across the African continent. Its mobile phone market remains far behind the developed world, and the continent is also enjoying rapid population and economic growth. Helios is directly benefiting from this as one of the leading owners of telecom infrastructure across Africa and the Middle East.

Therefore, we remain very optimistic about the long run, and we have no intention of selling our position entirely.

You can read our full investment thesis by clicking here.

However, at 16% of our International Portfolio, the concentration risk has become a bit too high, especially for an African REIT.

For this reason, we are only slightly trimming our position, bringing it back down to about 13% of the portfolio.

This sale unlocked about $14,000, most of which we are today directly reinvesting into: