TRADE ALERT - Retirement Portfolio January 2026 (Capital Recycling)

Dear Landlords,

I want to extend a warm welcome to all our new members!

As a reminder, our most recent “Portfolio Review“ was shared with the members of High Yield Landlord on January 5th, 2026. You can read it by clicking here.

You can also access our three portfolios on Google Sheets:

New members can start researching positions marked as Strong Buy and Buy while considering the corresponding risk ratings.

============================

TRADE ALERT - Retirement Portfolio January 2026

Alexandria Real Estate (ARE) was our biggest loser of 2025.

When we invested in it, the life science property sector was already oversupplied, and this was well-known to us, but the demand was gradually catching up to the supply.

This has now turned into a longer story as the demand side has collapsed as a result of the policy chaos of the current administration.

This has led us to review all our holdings to verify if any others could be exposed to this particular sector, and there is one.

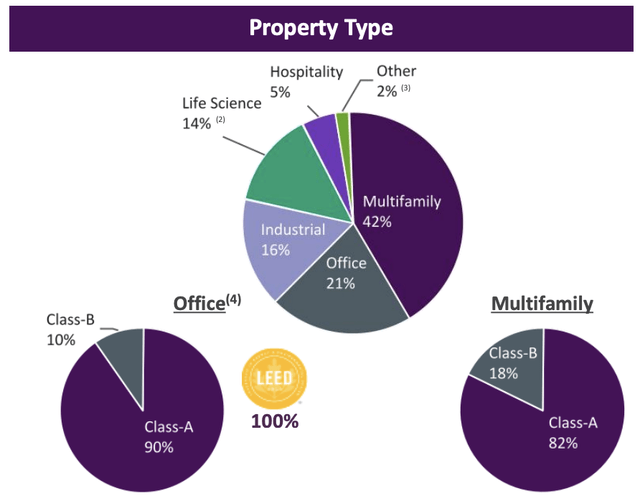

KKR Real Estate Finance (KREF) has 14% of its loan portfolio backed by life science properties, some of which are still under construction.

This would be fine if the REIT had a strong balance sheet with enough wiggle room to absorb potential losses.

But KREF is one of the more heavily leveraged mortgage REITs with a 4x debt-to-equity ratio, leaving little room for error.

Just in the last quarter, they again downgraded the risk profile of one of their life science loans. If they face more losses in the coming years, this could land them in serious trouble.

For this reason, we are today selling our position in the Series A preferred equity of KREF (KREF.PR.A). Our cost basis was $17.21, and we are today getting out at $18.20, pocketing a small gain on top of the 9% yield that we have earned over the last couple of years.

I consider this a good outcome, considering that the risks have surged.

It is also a good example of how we can apply lessons from past losers to future investment decisions, to hopefully avoid suffering the same losses again. The market appears to have overlooked KREF’s relatively high exposure to life science properties and failed to price this risk accordingly.

What are we buying with these proceeds?